Brexit: Who’s in the driving seat... and where are we going?

With the dust far from settled after a shock UK referendum result in favour of leaving the European Union, we assess the country’s future trade possibilities and their implications for the automotive logistics industry

With the dust far from settled after a shock UK referendum result in favour of leaving the European Union, we assess the country’s future trade possibilities and their implications for the automotive logistics industry

In this story...

- Shock to the system

- Gauntlet to government

- Cuts on the cards?

- Future trade scenarios

- Speculation and uncertainty

At 17 minutes past midnight on June 24th, the returning officer for the city of Sunderland, in north-east England, announced on live television that 61% of the city’s voters had elected to leave the European Union.

On news of the city’s massive 22-point margin in favour of ‘Brexit’, the pound promptly fell, dropping vertically on Asian exchanges. The significance of the Sunderland vote was clear: if that town could vote to leave, anything was possible.

Few tourists travel to Sunderland. Historically, just three industries served as the bedrock for its economy – coal mining, shipbuilding and brewing – and as these declined, jobs disappeared and decades of economic malaise set in.

To the rescue (to some extent) came EU economic regeneration funding, and the arrival of Nissan in 1986. Today, Sunderland’s Nissan car plant is the UK’s single biggest for vehicle assembly, producing nearly one in three UK-built cars, with more than 476,000 units last year. The plant exports around four-fifths of its output, with more than 70% of those exports bound for the EU.

Sunderland directly employs some 6,700 workers, with an estimated further 20,000 in its immediate supply chain. The nearby port of Tyne, through which most of the plant’s output is exported, is one of the UK’s largest vehicle ports for exports, shipping nearly 370,000 in 2015.

How the UK's car plant areas voted – click to enlarge

And yet Sunderland, along with most of north-east England, voted for Brexit. Nor was Sunderland unique in towns with automotive plants in doing so (see map, left). In Swindon, where Honda is based, the vote for Brexit was 55%. In Ellesmere Port and Luton, where GM has operations, the votes for Brexit were 51% and 56%, respectively. Jaguar Land Rover’s plant towns of Castle Bromwich, Solihull and Halewood all voted to leave. The same went for Toyota operations in Burnaston, in the Midlands, and Deeside, in Wales. Only in leafy Oxford, where BMW produces the Mini, did ‘Remain’ campaigners triumph, with a ‘Leave’ vote of just 30%.

[sta_anchor id="1"]To say that the automotive industry was shocked would be an understatement. Before the vote, senior industry executives had made their opinions very clear: Brexit would be bad news.

Rory Harvey, managing director and chairman of GM’s Vauxhall brand in the UK, had been quoted as saying:“We believe that not to be part of the EU would be undesirable for our business and the sector.” Renault Nissan’s chairman Carlos Ghosn was equally blunt: “Our preference as a business is, of course, that the UK stays within Europe, as it makes the most sense for jobs, trade and costs.” His sentiments were echoed by Tony Walker, deputy managing director of Toyota Motor Manufacturing UK, who said: “We believe that continued membership of the European Union is best for our business and for our competitiveness in the longer term.”

And yet – by a margin of 51.9% to 48.1% – the British people had indeed voted to leave the EU. Not consistently, certainly: London, and much of the UK’s prosperous south-east, voted to remain, as did isolated pockets around the country – mostly cities and their immediate surroundings. Scotland, together with Northern Ireland, also voted to stay in, but overall, by a majority of 1.3m votes, Brexit prevailed.

At 8:23am on the morning that the result became clear, the trade body for the UK automotive sector, the Society of Motor Manufacturers and Traders (SMMT), put out a brief, terse statement, attributed to its chief executive Mike Hawes: “The British public has chosen a new future out of Europe. Government must now maintain economic stability and secure a deal with the European Union which safeguards UK automotive interests. This includes securing tariff-free access to European and other global markets, ensuring we can recruit talent from the European Union and the rest of the world and making the UK the most competitive place in Europe for automotive investment.”

[sta_anchor id="2"]It is a statement that both throws down the gauntlet to the British government’s negotiators, while signalling the magnitude of their task. Hawes, in the latter months of the referendum campaign, had made much of a survey that found that 77% of the SMMT’s members were in favour of remaining within the European Union. “The message from UK automotive is clear,” he said. “Being in Europe is vital for the future of this industry to secure jobs, investment and growth.”

So, if being in the EU is ‘vital’ for the UK’s automotive industry, what will happen once it actually leaves?

What’s at stake and who is holding the cards? The answer is that no one knows. After the referendum outcome, both outgoing prime minister David Cameron and his successor, Theresa May, declined to trigger Article 50, the mechanism for formally notifying the rest of the EU of the intention to leave. The government is now targeting the first quarter of 2017 at the earliest for invoking the article.

Perhaps naively, many observers had initially expected that in the event of a Brexit vote, Article 50, and the subsequent two-year timetable that it imposes, would be triggered almost immediately after the referendum. Instead, May’s view was that a government sorely lacking in experienced trade negotiators and a negotiating platform needed as much time as possible.

That is important in part because the UK’s post-Brexit future looks set to be secured by two new government departments, working with the Foreign Office: one set up to negotiate the terms of Brexit with the EU and another to negotiate trade deals with the rest of the world. Each has been formed with a prominent Brexiteer as the government minister in charge. David Davis, a popular Conservative politician, became secretary of state for Leaving the European Union; Liam Fox, secretary of state for International Trade.

Perhaps the most surprising appointment was former mayor of London Boris Johnson as secretary of state for Foreign Affairs. Together, these three politicians are to be responsible for steering Britain into a post-Brexit future.

Nissan’s Sunderland plant, the UK’s largest assembly facility, exports most of its output to the EU and Nissan’s chief executive, Carlos Ghosn, has suggested future investment at the plant will depend on what kind of trading arrangements the UK has with the EU after Brexit

Nissan’s Sunderland plant, the UK’s largest assembly facility, exports most of its output to the EU and Nissan’s chief executive, Carlos Ghosn, has suggested future investment at the plant will depend on what kind of trading arrangements the UK has with the EU after BrexitThe stakes are high for the country and its automotive industry. Underpinned by volume producers such as Jaguar Land Rover, Nissan, Mini, Toyota, Vauxhall and Honda and supplemented by niche marques like Aston Martin, Bentley and Rolls Royce, automotive is Britain’s third-largest industry. The country is also the third-largest passenger car producer in Europe, building more than 1.6m units last year.

What is more, relatively little of that output is for domestic buyers. According to the latest SMMT statistics, 77.8% of cars built in the UK during 2015 were exported, mostly to mainland Europe. Engines, including those made at Ford’s two huge plants in Dagenham and Bridgend, are also exported globally. The UK’s automotive sector, the SMMT emphasises, is part of a complex, highly integrated European and global supply chain, and depends on significant cross-border trade in components.

That’s also because, while the local content of UK-built cars is growing, 50-60% of the components making up UK vehicle production are imported, predominantly from Europe.

The Brexit vote has also come at a time when the UK sector is at record levels, including the country’s best half-year performance for 16 years, with 897,157 cars produced by the end of June – up 13% on 2015, as billions of pounds of earlier investment in new models came to fruition.

[sta_anchor id="3"]The prospects for that performance now appear mixed. While industry observers don’t expect carmakers to suddenly shut plants and decamp wholesale to Europe, it is clear that as each manufacturer’s new models come up for consideration, tough choices are likely to be made.

A report by industrial consultants PA Consulting, for instance, reckons that plants run by Honda and Toyota are most at risk, as they are highly reliant on exports to mainland Europe and have relatively low margins and profitability.

“Uprooting plants is costly, but ongoing investment in capacity and new models is likely to be called into question,” agrees Mark Ellis, market line director for automotive logistics at logistics service provider Geodis.

“The UK’s automotive sector is likely to be hit harder than most industries,” adds Richard Gane, automotive industry expert and director at procurement consultants Vendigital. “The probability is that investment is likely to be cut back, but until more is understood about just what a post-Brexit future looks like, we won’t know by how much.”

The ‘disaster scenario’ What might this post-Brexit future look like for the UK’s automotive industry? What stance should the two government departments in charge of that future take? How will Europe respond to Britain’s negotiators?

The early signs have not been inspiring. Britain’s vaunted civil service appears to have done little by way of planning for Brexit. Nor had the various politicians campaigning for Brexit done much to put flesh on their widely criticised bluster.

Brexit minister David Davis, for instance, had spoken of negotiating trade deals with individual EU countries, seemingly unaware that membership of the Union imposes an obligation on member countries to negotiate as a single bloc.

Likewise, EU trade commissioner Cecilia Malmström apparently caught the UK government unawares by insisting that EU rules called for trade negotiations to take place only after a country had formally left the Union, rather than in the run-up to that exit. Her suggestion implied that, post-Brexit, the UK and EU would have to trade without a free-trade deal until a new one was struck – something that could take ten years to complete.

For now, at least, there is limited information on what either side really wants or expects, although the mood music from both Whitehall and Brussels suggests both sides are far apart. British politicians call for access to the European single market and free trade area, while European politicians insist that any such access will be on condition of the free movement of people – the restriction of which was arguably the single biggest issue for pro-Brexit campaigners.

"Government must now maintain economic stability and secure a deal with the European Union which safeguards UK automotive interests. This includes securing tariff-free access to European and other global markets, ensuring we can recruit talent from the European Union and the rest of the world." - Mike Hawes, SMMT

The UK’s automotive and logistics industries would appear to lose out from anything short of that untrammelled access to Europe, including tariff-less trade and the ‘single market’, in which goods that meet the requirements for sale in one EU member state automatically qualify for sale across the EU.

“In our direct discussions with automotive manufacturers, they have been clear that they don’t want Brexit at all, because of its potential impact in terms of tariffs and disruptions to trade,” says George Marinos, managing consultant in the advanced manufacturing practice at PA Consulting. “What they are looking for is a zero-tariff scenario, with smooth and cost-free customs procedures.”

However, in the absence of any sort of trade deal with the EU, that won’t happen. That would mean a reversion to World Trade Organisation (WTO) rules, with tariffs no less than 9.8% for imported vehicles and 3.8% in respect of components. Nor would the UK have access to the existing free-trade agreements in place with 53 non-EU countries. Just as painfully, from a purely logistics point of view, the imposition of the WTO’s ‘hard borders’ would mean border controls and customs clearances at ports and airports where UK-EU trade currently flows freely.

Many in the industry view such a prospect as unappealing, even on a temporary basis.

John Leech, head of automotive at business advisory group KPMG, calls any period of WTO rules the “disaster scenario” for the automotive sector. “Given the importance of the automotive industry, there’s going to be growing pressure for a ‘fast-track’ specific automotive trade deal, and quickly,” he says.

John Leech, head of automotive at business advisory group KPMG, calls any period of WTO rules the “disaster scenario” for the automotive sector. “Given the importance of the automotive industry, there’s going to be growing pressure for a ‘fast-track’ specific automotive trade deal, and quickly,” he says.

Nor would conventional approaches to circumventing tariff walls be useful in such a situation, adds Stephan Freichel, professor of distribution logistics at Köln University of Applied Sciences, who has also worked in automotive logistics.

“Longer term, when the eventual post-Brexit reality is known, then there will probably be government-backed workarounds such as free-trade zones to help smooth things. But in the short-to-medium term, these won’t be in place, and the environment for UK automotive plants when bidding for new models is going to be tough,” he predicts.

Consequently, whatever shape Brexit takes, experts are already watching for factory-and-model allocation decisions for 2020 launches – some of which OEMs will be taking over the next year – as the first opportunity to judge the industry’s response to Brexit.

Analysts at IHS Automotive, for instance, reckon that Jaguar Land Rover will accelerate its plans to build a further overseas plant, along with the one set to start up in Slovakia in 2018. Likewise, analysts at LMC Automotive have fuelled speculation already circulating that GM will move production of its Vauxhall-badged Astra model to Opel’s Gliwice, Poland factory, which assembles the left-hand drive equivalents of the vehicles built at GM’s Ellesmere Port facility on the outskirts of Liverpool, employing over 2,000 people.

At GM, which has already cut European production following the referendum, chief financial officer, Chuck Stevens, predicted as much as a $400m hit in the second half of this year because of the fall in sterling, and he admitted that mitigating such costs “may or may not involve footprint and other actions we will take” – and that is before any semblance of future trade relations between the UK and EU has been confirmed.

Similarly, Nissan’s Carlos Ghosn has signalled that while he was “reasonably optimistic” that common sense would prevail when Brexit negotiations eventually began, a lot depends on the outcome of those negotiations.

“The question is what will happen to customs, trade and circulation of products,” he told the BBC, describing Nissan’s Sunderland factory as a European plant that happens to be based in the UK. “That will determine how – and how much – we will invest in the UK.”

Ghosn’s statements pre-empted a stark warning from Japan, whose companies are highly represented in the British automotive supply chain, of the UK’s need to maintain close relations with Europe. In September, Japan’s ministry of foreign affairs issued a detailed statement and list of requests from Japanese business leaders in the UK, stressing the importance of a free trade system. It effectively argued for the UK to remain in the single market, including retaining access to European markets, capital and skilled labour. The plea was made because Japanese businesses operating in Europe are concentrated in the UK, from which they sell extensively into the EU.

[sta_anchor id="4"]The options on offer So what, broadly, are the post-Brexit options? In practice, experts reckon, the scenarios boil down to just a handful of alternatives. For automotive logistics, at least, each would bring some obvious downsides compared to existing membership.

For those keen to retain access to the single market, for instance, securing membership of the European Economic Area (EEA) has clear merits. This is the approach taken by Norway, in preference to full EU membership.

So might the so-called ‘Norway option’ work for the UK? Brexiteers are unlikely to like the fact that EEA member states still have to adopt EU rules on issues such as state aid and competition, without having a say in formulating those rules; still have to accept the free movement of people; and pay a fairly significant contribution to the EU budget.

Meanwhile, as EEA countries are technically outside the EU customs union, there are extra customs and security procedures required for shipments to and from the EU – although EEA members have mostly come to bilateral agreements with the EU to simplify such requirements.

Another touted option is membership of the European Free Trade Association (EFTA), which again provides some – but not complete – access to the single market. The UK was a founder member of EFTA in 1960, and eventually opted to join what became the full European Union in preference to EFTA, as did Denmark. Currently, only Norway, Iceland, tiny Liechtenstein and Switzerland are members of EFTA (although Switzerland is not a member of the EEA).

Plants such as Toyota’s in Burnaston, which is highly reliant on exports to Europe and has an integrated inbound supply chain with the EU, could be hard hit without single market access

Plants such as Toyota’s in Burnaston, which is highly reliant on exports to Europe and has an integrated inbound supply chain with the EU, could be hard hit without single market accessThe merits or drawbacks of EFTA memberships depend on what each country has negotiated with the EU for each sector – a process that has taken those countries years to complete. However, members must again contribute to the EU budget, and – at least in the case of Switzerland – accept the free movement of people. Though perhaps less directly relevant for automotive, current EFTA agreements, including those for Switzerland, do not cover key areas of the economy, such as services, for which the UK has large financial and consulting industries.

Then there’s the notion of a customs union – the form of trading relationship with the EU that is currently enjoyed by Turkey for industrial goods. This has more obvious merits for the automotive industry, in that it allows the free movement of manufactured goods with no tariffs, thereby eliminating not only the ‘nightmare scenario’ of significant barriers, but also border delays resulting from customs bureaucracy.

Hardline Brexiteers may jib at handing over external trade negotiation to the EU, meaning that the UK could not sign separate trade deals with countries like India or China. There’s also a requirement to apply EU rules, and while a customs union imposes no requirement to contribute to the EU budget, it also permits no say or vote on those rules. The customs union is furthermore incomprehensive in other economic areas, including services, agriculture and finance, all of which are very important to the UK’s current trade and ties to European Union member states.

Finally, there’s the fourth option: the UK in effect ‘going it alone’, and agreeing trade deals on a country-by-country basis. For example, outside the EU customs union the UK could, in theory, set up trade deals relatively quickly with countries with whom it has close relations, such as Canada and Australia. While notionally attractive – and much-hyped by Brexiteers – the difficulty here lies in the practicalities.

The much-vaunted proposed trade deal between the EU and Canada, for instance, has taken seven years to reach its present status, with the timetable for implementation still unclear. Has the UK enough trade negotiators to handle multiple trade negotiations with multiple countries? Most observers reckon not, and given that EU members are forbidden from negotiating individual trade deals, some accommodation would still have to be reached with the EU as a whole.

“In our view, the notion that the UK will be able to have free trade with the European Union at the same time as negotiating bilateral deals with countries such as China is incredibly naïve,” says Neal Williams, group managing director of expedited freight specialist Priority Freight, which handles significant volumes of automotive freight. “For the industry, the referendum is a dreadful development, and I struggle to see the positives.”

So what to make of these various scenarios? It looks like these alternative trade arrangements have less to offer the UK’s automotive industry in comparison with full EU membership.

Yet, given that so little of the political debate during the referendum revolved around issues such as trade and access to the single market, this is perhaps inevitable. Among both voters and politicians, hotter topics turned out to be ‘independence’, the size of the UK’s contributions to the EU budget, and immigration.

Questions still remain about which scenario the UK government will pursue, and what influence industry – including automotive – will have on its deliberations and negotiating strategy.

"When the eventual post-Brexit reality is known, then there will probably be government-backed workarounds such as free-trade zones to help smooth things. But in the short-to-medium term, these won’t be in place, and the environment for UK automotive plants when bidding for new models is going to be tough." - Stephan Freichel, Köln University of Applied Sciences

Brexit minister David Davis gave his first statement to parliament on the subject on September 5th, in which he acknowledged that it would take time to get the “right priorities, the right aims and the right outcomes”. That said, he assured MPs that the government was listening, including studying 50 different sectors of industry to see what the effects of Brexit might be on them. The key objective of negotiations, he added, would be to form a free-trade agreement with the EU that did not require it to unconditionally accept EU migrants and pay into the EU budget.

Critically, though, he observed that he thought retaining access to the single market was “improbable”, if that meant accepting free movement of people.

Fascinatingly, the prime minister’s official spokesperson promptly slapped down Davis in a press briefing, stressing that he was expressing his own views, rather than official government policy. That said, one piece of information that Davis let slip in response to direct questioning from MPs does appear to be government policy: that the UK will decide its stance on the desirability of a customs union before triggering Article 50. This matters, because membership of a customs union with the EU precludes separate bilateral trade deal with non-EU countries – the very raison d’être of trade minister Liam Fox’s new government department.

[sta_anchor id="5"]Visions of the UK’s post-Brexit future are murky at best, with even the government divided on it. For the automotive industry, and its logistics partners, perhaps the best hope for now lies in communicating to government their own post-Brexit aspirations. As the UK’s third-largest industry, together with the important logistics sector, such voices should figure prominently among the 50 industries that Brexit minister Davis is consulting and taking into consideration.

What does the industry want?Perhaps surprisingly, many voices are muted, especially in logistics. Gefco, for instance, declines to comment on Brexit, referring to a terse three-sentence statement acknowledging the uncertainties it brings. DHL is similarly tight-lipped.

Even more surprisingly, a logistics industry representative body, the British International Freight Association (BIFA), issued a blunt statement saying that it will not be adding to “the highly speculative debate” on what might happen to trade between the EU and the UK post-Brexit.

“Is there any worth in speculating on the consequences of Brexit before anything tangible has happened and there is little sign of any clear information emerging from government on the timetable for exit?” asked Robert Keen, BIFA’s director general. “We will avoid adding the trade association’s voice to what is currently a worthless game of ‘ifs’ and ‘buts’ about the potential impact of Brexit on trade. [But] when government is ready to fire the starting pistol on Brexit, BIFA will be ready to make the necessary representations on behalf of our members.”

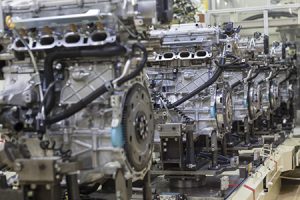

Many of the engines produced at plants in the UK are destined for export, leaving such operations as vulnerable to changing trading conditions as those producing finished vehicles.

Many of the engines produced at plants in the UK are destined for export, leaving such operations as vulnerable to changing trading conditions as those producing finished vehicles.The logistics departments at the likes of JLR, GM and others are also unwilling to comment beyond official company policy. Officials at JLR say the OEM is committed to current UK and EU investments, and that it will work to make sure the government understands its needs.

Some organisations in the UK, however, are being more proactive, perhaps sensing an opportunity to punch above their weight in the present policy vacuum.

For example, the Freight Transport Association’s (FTA) chief executive David Wells has urged the prime minister to prioritise the logistics industry during negotiations, to ensure that goods can move freely between the UK and the rest of the world. Access to the single market and the ability to hire non-UK drivers were top of the association’s list of concerns, he added.

That said, points out Chris Yarsley, the FTA’s Brussels-based EU affairs manager, the range of potential Brexit outcomes that are of concern to FTA members is extensive, taking in everything from the detail of customs arrangements to the unpicking of UK transport legislation that is based on EU directives and regulations.

“Our preference is clearly for free trade, with as few restrictions as possible, and we aim to give the UK government as clear a picture as possible of what a post-Brexit future looks like to our 15,000-plus membership. We will be looking very closely at whatever emerges as a negotiating position in order to see how ‘trade-friendly’ it is, and what the impact might be on our membership.”

A similar, watchful eye is being kept by the UK Warehousing Association, explains its chief executive Peter Ward. “The outcome of the referendum wasn’t what we expected, either as an association or as an industry, and our priorities are the free movement of goods, and the free movement of people,” he explains. “In an industry that relies extensively at the moment on European labour, the free movement of people is vital: there are logistics parks in the UK’s Midlands, serving the automotive industry, where the proportion of east European workers is over 75%. Take them away, and the industry could be on its knees.”

Yet even so, some are sanguine, arguing that it is too early to predict the consequences of Brexit, and that in any case, some pain would be worth the price of exiting the EU.

Ardent pro-Brexit champion Andrew Baxter, for instance, managing director of international freight firm Europa Worldwide, which sees 75% of its revenues come from UK-European Union trade, is unrepentant about the referendum outcome.

“There will be pluses and minuses, and lengthy customs clearances might be one of those minuses, so it’s important that the government works towards making customs clearance as smooth as possible,” he argues. “But even so, it’s my firm belief that the UK is better off outside the European Union – so it would be crazy to base our entire relationship with Europe solely on customs clearances and customer charges. What’s bad for our industry isn’t necessarily bad for the country.”

Is he right? Only time will tell. Until then, uncertainty rules the waves for Britain.

Freight flows with Europe, infrastructure investment and Brexit will be among the topics that will be discussed at the inaugural Automotive Logistics UK conference that will be held October 5-6th in London. Click here for more details.

EEA membership – Norwegian routePros: Tariff-free, near-complete access to European single market; harmonised standards and regulations; can negotiate bilateral FTAs with other countriesCons: Customs rules apply for shipping; politically unpalatable requirements, including freedom of movement and payment into EU budget; no decisive role in deciding EU regulations

EFTA membership – Swiss routePros: High access to single market, with more potential opt-outs; reduced EU budget payments; can negotiate bilateral FTAs with other countriesCons: Could take years to negotiate; might not include services; likely to require free movement and some payment to EU budget; no role in deciding EU regulations

Customs union – Turkish routePros: Tariff-free trade of industrial goods; seamless customs processes; no demand to pay into EU budget or accept free movementCons: Might not cover services or agriculture; no control over separate global trade agreements and external trade

Customs union – Turkish routePros: Tariff-free trade of industrial goods; seamless customs processes; no demand to pay into EU budget or accept free movementCons: Might not cover services or agriculture; no control over separate global trade agreements and external trade

WTO rules – Hard BrexitPros: Flexibility in making global trade agreements; no requirements to follow EU rulesCons: WTO tariffs of 9.7% for vehicles, 3.8% for parts; costly non-tariff trade barriers with EU; lengthy negotiations for trade agreements; no access to EU global agreements