Chris Lewis investigates how European road providers are surviving in the face of another potential recession and an investment shortage. Additional reporting by Christopher Ludwig on the latest EU transport policy issues.

This past year may go down as the annus horribilis for some in the finished vehicle road transport industry, but there are fears 2012 could be even worse. With the eurozone crisis draining what little consumer confidence remains, volumes of car sales continue to stagnate or, in some markets, plummet. Unsurprisingly, spending by the road transport sector in new trucks and trailers has been at a standstill, which some in the sector fear could precipitate a capacity shortage. Sooner or later, the old trucks will have to be replaced–but nobody is in the mood to go shopping.

Until recently at least, the general European road freight sector had been growing, albeit weakly, but a report by consultancy Transport Intelligence estimates that the market is more than 10% lower than at its peak in 2008 and it could be 2014 before all the lost ground is recovered. While recovery has been held back by troubled southern economies, Germany has seen demand grow for road transport, fuelled in part by domestic vehicle sales–up more than 10% this year–along with continued growth for exports. Other major economies, such as the UK and France, have seen demand flat or decline several percentage points, while Italy and Spain are down double digits. Some Central and Eastern European countries, in particular the Baltic States, also saw healthy growth as supply chains continued to develop on a European region-wide basis; vehicle sales in the Baltics recovered as much as 80% in 2011 from depressed levels. Russia has seen growth of more than 30-40% for much of the year.

Advertisement

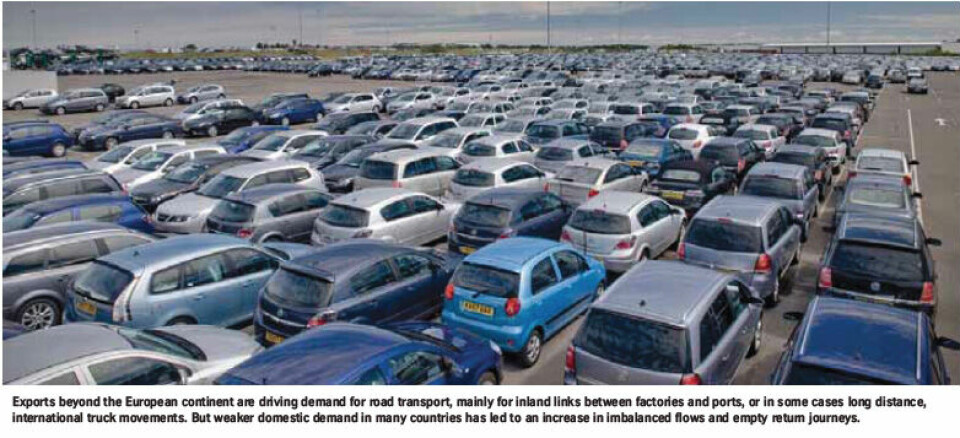

Mike Sturgeon, executive director at the Association of European Vehicle Logistics (ECG), says there is more concern now among ECG members than earlier in 2011. However, LSPs continue to survive. “I think it’s a very resilient industry,” says Sturgeon. “No one is making much money and margins are very thin, but companies are surviving.” Exports beyond the European continent are also driving demand for road transport, mainly for inland links between factories and ports, or in some cases long distance, international truck movements, such as to Russia and Central Asia. Exports are also driving certain niche markets, such as enclosed distribution for high-end vehicles. David Brinklow, director of UK-based specialist prestige provider Ontime Automotive, says that such distribution for China has never been stronger.

Exports and assets help Spanish carriers survive Eduardo Estévez, general manager of sales and customer service for Spain’s Bergé Automotive Logistics, says that despite the country’s dire market conditions, “no major players have exited yet in the Spanish market.”

Estévez believes this survival is partly because operators own a large number of assets, which they can borrow against or sell to get cash to re-invest in their businesses. But as real estate values plummet further, many are reluctant to sell. Many small companies and subcontractors across Europe, including the self-employed, are indeed pulling out of the market, which has become even more competitive now that major companies like Groupe CAT and Gefco have been building up their own fleets of car transporters. In Spain, the domestic distribution market has declined 55% from 2007 levels, while vehicle stocks are 70% lower than at that time. “Car buyers are waiting four months to receive cars, totally the opposite of the market up to 2008 in which the immediate availability was a commercial competitive advantage,” Estévez points out.

Furthermore, manufacturers have shifted workshop services that were traditionally provided by logistic operators–including pre-delivery inspection, customisation, repairs, refurbishment of fleet and used cars–to dealer networks to make fuller use of their workshop capacity. With the market so reduced, capacity is more than sufficient at the moment. However, warns Estévez, “Carriers are not investing. If sales do increase, no capacity would be available in the short term.”

A deep imbalance Konrad Zwirner, senior vice president of international sales and business development at the Austrianheadquartered, pan-European logistics operator Hödlmayr International, points to varying fortunes across the continent, from falling volumes in the Ukraine to high export volumes from Germany and Romania. The problem for the logistics industry, he says, is although exports increase traffic from plants to ports, the flows are imbalanced, with little coming back. In Eastern Europe, where Hödlmayr is the market leader, there has been recovery in the Baltics and parts of Central Europe, but sales have declined in Hungary, Romania and the Ukraine. Exports from Romania are high thanks to Renault’s Dacia and the opening of new assembly lines, but again

the problem is the lack of a balancing stream in the return direction. In Spain it’s a similar picture with growth in exports– not least with Seat now producing the Audi Q3–but a depressed local market causing imbalanced traffic flows. Perhaps the best-performing market has been Turkey, where not only have exports increased but a strong domestic market has created further demand for vehicle logistics, according to Zwirner, who is also commissioner for land transport at the ECG.

As in Spain the larger companies have survived but many sub-contractors have thrown in the towel or been taken over. Hödlmayr recently purchased the assets of Tatschl, a carrier for Ford, BMW, Mercedes, Opel and Toyota. This 89-strong addition to Hödlmayr’s fleet–along with 100 drivers–has made the LSP one of the leading investors in the sector and with 590 trucks, one of the largest fleet owners for vehicle logistics in Europe. Tatschl, says Zwirner, was a good company and particularly well established in the east-west trades. “Its problem, though, was that it only had road transport, whereas we are established in a lot of areas like rail, PDI and logistics.” Pure hauliers appear to have suffered the recession’s most brutal blows, while the better-spread logistics firms have faired somewhat better. “We’ve been able to cope by cost cutting and obtaining business from those leaving the market,” admits Zwirner.

Fleet investment has also become a thorny issue. The major operators have to some extent been able to replace older trucks, however fleet replacement is different from expansion, Zwirner stresses. “If we are to actually increase the numbers, we can only do that with the backing of our customers.” Meanwhile, the average age of the European car transporter fleet is increasing. “After the crisis, companies waited before they renewed many of their vehicles and as a result the fleets got older. But we need long-term contracts with our customers,” he says. While the general consensus is that capacity levels in most of Europe are adequate, there are some predictions that the age of current fleets will lead to increased transporter demand, creating a potential bottleneck among trailer manufacturers, some of whom saw drops of 80-90% during the recession. “Maybe this won’t be the case if there is a new recession, though there will still be the need to replace old trucks,” says Zwirner. There are some examples of investment, either from large providers or niche carriers. Ontime’s Brinklow says his company has undertaken a “significant investment programme” to modernise its fleet of enclosed transporters and its communications systems. But in general, fleets across Europe are aging, confirms ECG’s Sturgeon, who points to low rates and shortterm contracts. However, he believes there are signs of improvements among some OEMs.

“They may not be reflected in actual contracts yet, but I think the message is being taken on board,” he says. Capacity concerns would be more worrisome for carmakers likely to increase volumes in 2012–and one of the possible few could include Hyundai-Kia, which has defied the poor economy the last three years. Frank Schnelle, general manager for development and planning at Glovis Europe, the group’s logistics arm, says Hyundai and Kia will increase European production next year and, with new models from overseas coming to the European market, Glovis expects an increase for transport demand. However, “since carriers are quite sceptical about investing in new capacity due to the uncertainty of the markets, Glovis is preparing some countermeasures to minimise the risk of missing capacity to support the ongoing growth of Hyundai and Kia in Europe,” he added. Schnelle expects consolidation of the transport sector to continue, though this might not necessarily translate into capacity shortages. “Some players might disappear or be taken over,” he says. “But this might not necessarily mean that transport capacity will decrease but [that it] would be concentrated at the market leader.”

Advertisement

A resilient CAT One such possible leader to emerge could be Groupe CAT. To speak with Antoine Namand, head of vehicle logistics at the French international operator, you would scarcely know there was a crisis in Europe. CAT’s previous owners faced a financial crisis of their own back in 2006 and some important lessons were learned which have prepared the company well for the current situation, he says. Cost analysis is key to CAT’s strategy.

“Quite simply, if you reduce prices without reducing your costs, then you go bankrupt,” says Namand. It also helps to have a global business spread across a large number of varied markets to flex with the ups and downs of the global economy. Russia, for example, has gone from boom to bust and back again. Namand believes providers must be able to meet customer’s demands with considerable flexibility. “Many people in the industry are used to working in a certain way and seem to be hoping that things will go back to the way they were,” continues Namand. “But things are moving fast. We have electric vehicles, cars are moving much longer distances; the world is changing.” Namand says that while it’s difficult, you can still earn money in car haulage. CAT has worked specifically to fine-tune its operation and squeeze out empty mileage to the point where it is no higher than about 20-22% and in some regions as low as 4-5%. CAT is also sweating its assets, running trucks up to 24 hours a day, seven days a week in some markets.

An example of its flexibility and drive for efficiency can be seen where it switched vessel calls for its shipping joint venture with Suardiaz, SCSC, to the Brittany port of Montoir, to give an import flow to counterbalance deliveries into the region and help soak up empty truck capacity. It helps to have assets under your own control when making these sorts of decisions, of course. A new compound opened at Batilly in Eastern France is also at a strategic convergence point for several different flows and helps keep transporters filled. CAT has also been on an investment push, including most recently the 50% acquisition of a British carrier. The aim, says Namand, is to add around 700 vehicles to CAT’s current 300-strong owned fleet, while retaining the services of around 1,000 exclusively subcontracted vehicles.

Getting Europe in harmony On the policy front, the ECG continues to lobby intensively in favour of a European-wide standardisation of allowableloaded- truck lengths, which are currently a patchwork of different standards across the EU. The ECG wants a harmonised, minimum-loaded length of at least 20.75 metres through the use of front and rear overhangs, which some countries currently allow and others do not. According to Sturgeon: “Although most European countries allow an overall loaded length of around 20.75-21.00 metres–and some allow longer–there are many, especially in the Baltics and southeastern Europe [that] do not allow overhangs at all and thus restrict the loaded length to the same as the unloaded length, which is just 18.75 metres as regulated by EU Directive 96/53 on weights and dimensions.”

Allowing a 20.75-metre-loaded-minimum length would make it possible to go across multiple countries on the continent without changing equipment or reducing load sizes. There would also be no changes applied to equipment or infrastructure. “The important thing is that the trucks themselves would be the same length as today–it is just a question of how they are loaded,” says Sturgeon. Sturgeon says that the ECG has stepped up its lobbying efforts in Brussels on truck dimensions and cabotage. “We have a new EU affairs manager, Tom Antonissen, and we’ve developed an action plan based on short- and medium-term expectations,” explains Sturgeon.

The issue has considerable impact for some carmakers, particularly Renault, the major manufacturer in Romania, which faces disadvantages in distribution because of truck regulation. In common with many other Eastern European and Baltic countries, Romania only allows rear overhangs from the standard 18.75-metre length on payment of a special licence fee. “We are missing some opportunities to optimise our load factor and to reduce costs, trucks and emissions,” says Thomas Vernier, general manager of outbound operations in Europe for Renault Nissan. “We wish that Europe could reach a compromise on the same rules, which is something that would also benefit LSPs.” According to Sturgeon, whether or not they allow overhangs is a matter for individual member states to decide under the subsidiarity principle. But the EU might get involved if it can be persuaded that it is an internal market issue and if it can be seen as directly related to the political wish to make road transport more efficient while further promoting intermodal transport.

Not easy to be longer or higher A separate, somewhat more complex issue is that of the European Modular System (EMS), or so-called ‘gigaliner’ trucks of 25.25-metre length. Sturgeon says that ECG is also broadly supportive of the EMS, however the system would be untenable in its current form for the vehicle logistics sector. For starters, such a truck would require not only new trailers but also modified, more expensive trucks– and with LSPs struggling, such investment is hardly feasible. The EMS would also be problematic for deliveries to urban areas in many European cities.

“The EMS would only have a niche use for LSPs, primarily for point-to-point flows such as plants to ports, since such trucks could not deliver cars to urban dealerships,” he says. “Such limitations could also lead to increases in empty backhauls.” But the EMS also raises several problems for both countryspecific and EU transport policy. The general haulage regulation in the European Union is currently 18.75 metres with a 40-tonne weight limit, unless the truckload has been in combined transport with rail, in which case it can be 44 tonnes. The EMS concept is for a truck of 25.25 metres weighing up to 44 tonnes. Sweden and Finland currently allow a version of this but with an even higher weight limit inherited from their timber industries. The Netherlands, Denmark and certain states in Germany either accept trucks at 25.25 metres or will be running trials. However, both Denmark and Germany have categorically limited the weight of such trucks to 40 tonnes. According to Sturgeon, while vehicle logistics providers do not need a 44-tonne limit for an 18.75-metre truck, at 25.25 they would. This effectively means that if the EMS were rolled out further in Germany or adapted at a European level on Danish terms, it would not be legally useable by vehicle logistics providers.

Advertisement

A further complication is that the EU limit of 18.75 would technically still apply for crossing borders, which would mean that even if Germany and Denmark both allowed longer trucks, it would still be illegal to cross the border with a truck longer than 18.75 metres. Modifying these regulations would likely require a change to the commission directives, which is a long, complicated process. It’s partly for these reasons that the ECG supports the EMS but does not lobby for it, focusing its efforts instead on the more practical issues of loaded lengths. On the other hand ACEA, the association of European carmakers, is lobbying strongly for EMS, despite the weight issue. This support is perhaps unsurprising in part, at least, because ACEA represents several truck manufacturers that would likely benefit from providers investing in new trucks. The issue of truck heights is another contentious issue.

Truck heights are covered in directive 2007/46/EC, of which there have been recent proposals to amend its annexes for a height limit of 4 metres for those newly-built trucks that have a mass lower than 3.5 tonnes, along with all trailers. The proposed exception would be for double-deck- and semitrailers, which could have a height up to 4.9 metres. For car carriers, a 4-metre-height limit would cause difficulties in some markets, says Sturgeon, notably the UK, France, Ireland, Spain and Portugal that haven’t had formal height limits. However, the current legislation does not clearly define car carriers as either a trailer or double-deck trailer. “If all car carriers are classified as double-deck trailers, then we’re in the clear,” he says. Member states and the European Parliament are due to vote on the issue soon.

A peculiarly British problem New cabotage rules have also proved problematic in the UK, where there are still strong, twice-yearly peaks owing to the year-letter registration plate changes in March and September. In the past, the UK industry coped by bringing in trucks from across Europe, but the new rules restrict cabotage movements to three movements in seven days and then only after a loaded arrival from across a border. Such rules make these operations unattractive financially to European providers, says Sturgeon. ECG, together with the Society of Motor Manufacturers and Traders and industry representatives, addressed these issues earlier in 2011 to Mike Penning, under secretary of state for transport in the UK. The department has since looked at whether it could use a relaxation of the rules–as had happened in Ireland, which has a similar registration-related peak–but decided that a change in the legislation would be needed. Such a change requires an impact assessment, which has now begun with ECG members closely involved.

The issue could be resolved at a European level since the current EU Transport Commissioner, Siim Kallas, has publicly stated that he is determined to see all cabotage restrictions abolished by the time his term of office ends in 2014. However, Sturgeon believes a more immediate change in UK legislation would be necessary as the abolishment of cabotage in the EU in 2-3 years time is unlikely. As ever in Brussels it seems, the complex workings and interpretations of the law are unlikely to result in any quick changes.