Have the tides turned for car shipping?

No one is pretending there has been a return to pre-recession highs, but the car shipping market has come back to high speed and nearly full capacity. But with worries over a ‘double dip’, a rising Yen and increasing fuel prices, the competition is tougher than ever, writes Chris Lewis.

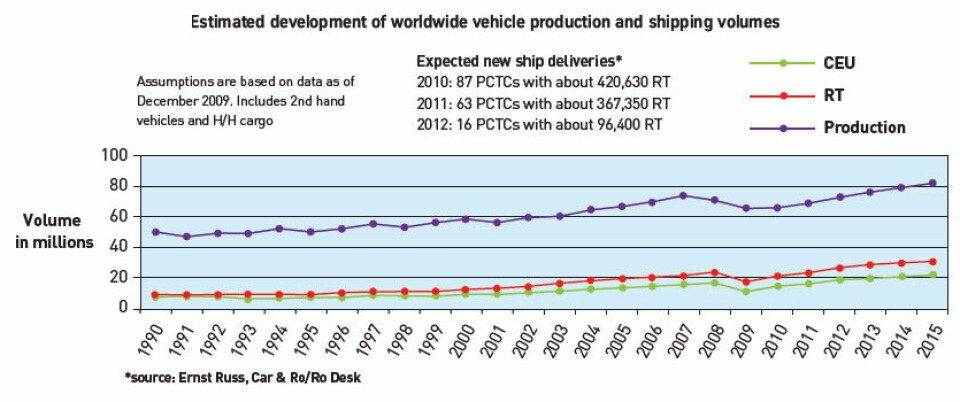

The global car shipping industry has been in a pretty sick state these last two years. The downturn led many shipping lines to scrap and layup ships, while reducing speed to save costs. The good news is that much of those measures have now been reversed, with new builds coming online and many ships coming out of storage. However uncertainty over the recovery in some markets, as well as rising fuel and operational costs, mean that shipping lines remain cautious–costs and load factors are now the biggest causes of concern. According to Hamburg-based shipbroker and analyst Ernst Russ (ER), the world’s car carrying fleet capacity is still growing, with 36 vessels already delivered in 2010 and a further 47 due in the remainder of the year. This will be followed by a further 63 in 2011 (previous ER estimates put the figure at 52), followed by 18 in 2012. (The sharp falling away in 2012 is to be expected, as ship operators normally wouldn’t commit themselves to new purchases more than 1-2 years in advance.)

However, shipowners are discussing cancelling or delaying deliveries from shipyards, so a small number of vessels still listed as being ‘on order’ may not materialise. But this is unlikely to be a big factor, ER believes.

Ship scrappage rates soared in 2009. At 390,000 RT (RT is a common unit of measurement used in the car shipping industry based on the length of a 1966 model Toyota), they were around ten times the level of 2008. The scrapping rate is one source of flexibility for the industry because, as further ships are delivered in the second half of 2010, owners would have the option of keeping or retiring their existing older tonnage. ER suggests the existing fleet is probably sufficient to ship all cargo and with the number of vessels due for delivery for the second half of 2010, it is likely that a similar capacity will be deleted from the fleet. On the other hand, if the cargo volume increases further, withdrawals could be reduced to below the capacity of the newly delivered tonnage. Overall, ER is fairly optimistic that car volumes will increase quicker than shipowners can build vessels, with most scenarios suggesting available tonnage to fall short of demand over the coming years.

While slow steaming has largely abated, ship operators are coming under pressure from carmakers to speed up ships to minimise inventories, but at the same time fuel costs have risen while load factors have not yet fully recovered. ER is therefore expecting fairly poor financial results from shipping lines.

A new market entrant

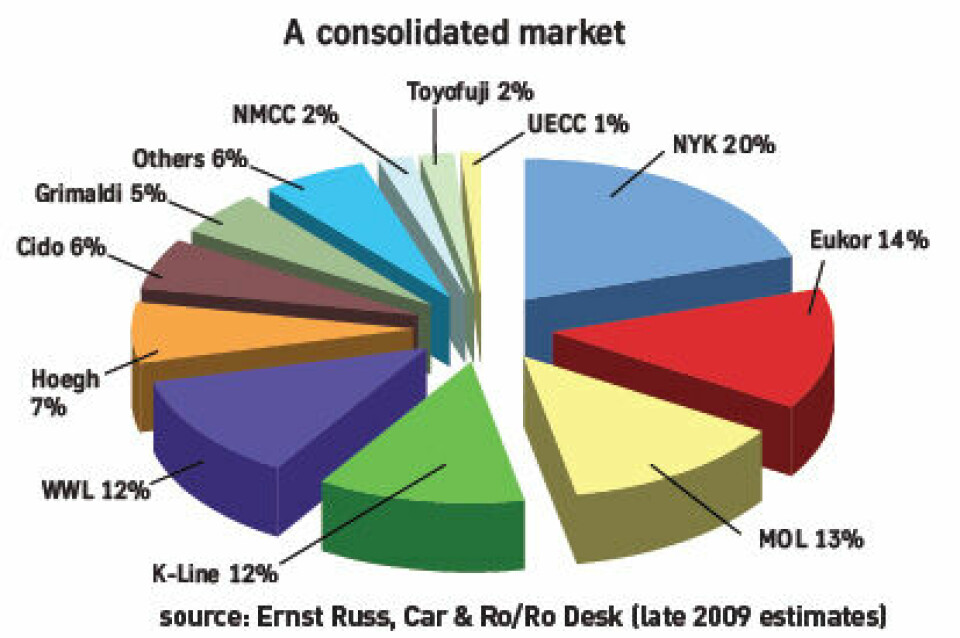

According to ER, the world car carrying fleet is dominated by NYK, MOL, K Line, Eukor and WWL, which together still control around 70% of fleet capacity–compared with 75% a year before–with the three medium-sized players, Höegh, Grimaldi and Cido accounting for a further 20% of the market (although ER says that Cido has deleted all new-building contracts for 2010 and thereafter, except for two smaller vessels. All larger vessels were either cancelled or, where this was not possible, taken over by NYK). A newcomer as a carrier is the logistics provider Glovis, majority-owned by Korean manufacturer Hyundai/KIA.

Glovis, which has either bought or taken on a number of vessels on time-charter, seems to be having much more success and moving quicker than anticipated, ER continues. It is said to have ordered two big PCTCs from Hyundai shipyard–one of the few operators currently ordering large new ships–and would appear to be taking over volumes that had traditionally been Eukor’s.

However, the newcomer’s effect on the overall market has been muted, ER says, as it was able to charter in tonnage that was not needed by other operators and neither the freight nor the time charter rates have moved significantly because of the new entrant.

Espen Hofland, head of the president’s office at Eukor said that the shipping line is making no major changes despite some of its Hyundai/Kia business going to Glovis, but it will be diversifying. “It will be business as usual, although our share of export volumes is down. We will continue to serve Hyundai/Kia but we will also diversify our cargo base–both into car manufacturers and other types of business.”

Svein Steimler, executive VP and COO at NYK Group Europe, points out that carmakers with their own shipping companies are nothing new–VW has run its own ships for many years. But unless a manufacturer’s own trade flow is reasonably balanced, or it can persuade a rival manufacturer or a non-automotive return cargo to use its ships, the potential for OEMs to run their own ships must be limited, Steimler argues. “These ships cost a lot to build and run. Though if a few manufacturers were to start running their own ships, it might actually be good thing because they would perhaps experience the true cost of running them.”

Eukor has maintained its deliveries of new ships–mainly in the 6-8,000 RT range–which will continue to be delivered over the next 2-3 years. The ships will mainly replace chartered tonnage. “Our tonnage is pretty much balanced now,” adds Hofland.

Jin-Og Kim, the director of Glovis’ PCTC operating group, says there has been a rather gradual or at least steady sign of improvement in the car shipping market for the first half of the year thanks mainly to a continuous increase in exports from Korea and Japan. “Compared to the tragic 2009 performances, Japan export volumes have presented steady upward figures during the first half this year.” But there are also concerns that optimism over an early recovery in the major US and European markets may have been slightly overdone. There is also concern over the strengthening yen. Nevertheless, the number of long-term laid up vessels have reduced to almost nil during the first half of the year thanks to scrapping as well as the rebound in cargo volumes. There is however still a large amount of new tonnage entering the market in the second half of this year and up to 2012. And with the global economic situation still uncertain, it is hard to be sure about future capacity issues, says Jin-Og Kim. “When Glovis commenced transporting automobiles ex-Korea from January this year, the number of operating vessels could be counted with the fingers in both hands,” he says. “Now after seven months, the number doubled to about 20 vessels.”

With Glovis’ main customers, Hyundai and Kia, forecast to maintain their strong export volumes, Glovis will expand its third-party sales activities on a long-term basis and fleet capacity is expected to grow gradually.

With the mature markets of the US and Europe likely to remain stagnant, other economies in the Middle East, Oceania, Africa and South America will play a greater role, at least for the time being.

In the long term, there will be a requirement to service the group’s foreign factories so services can in time become more diversified.

Trade from Japan must pick up

Though the Russian import market remains considerably lower than before the recession, increases in the Chinese, Indian and Brazilian market have led to increased flows in and out of those countries. NYK, for example, currently serves four ports in China–Guangzhou, Shanghai, Dalian and Tianjin. Between Europe and India it serves Mumbai and, from South East Asia, Chennai. The volumes of cars actually moving in and out of these countries by ship are relatively modest compared with the local market and local production, but it has the potential to grow, says Steimler.

But what the shipping world really wants is a pick-up in the large-volume trades–Far East (Japan and South Korea) to Europe and Far East to North America. As long as these volumes remain relatively low, fewer ships come to Europe, which gives European manufacturers a headache as there is less capacity available to ship their own exports overseas. Trade from the Far East to the US has picked up, but there is not enough backhaul cargo from North America to make this a very good business for carriers.

Dennis Manns, VP sales and logistics planning at American Honda, says: “Our import business from Japan has increased over the past several months. Obviously we are nowhere close to business levels of two years ago but we are in much better shape than a year ago. I believe that many of the ship operators are balancing their fleet with market conditions and a rise in imports has put a squeeze on capacity levels and taken up the slack.”

But it would be a mistake to sit back and wait for the market to return to ‘normality’, Dennis Mann continues. “The norms have changed for everyone and forecasting has become an even greater challenge... these market conditions make you aware–if you weren’t already–of the impact your supply chain has on the growth or decline of other key markets.”

NYK’s Steimler is confident that strong growth will return on the back of emerging regions. When that does happen, given that the market for ship capacity is tightening, NYK and other carriers may be more selective in which traffic they choose, concentrating on the more lucrative markets. NYK has enough new capacity on order to meet its immediate needs, although when the recession hit it quickly took older tonnage out of service–much of which had been life-extended to cope with the earlier boom–and laid up some ships, almost all of which have now been returned to service. A new-building programme will add significant new tonnage between now and 2012.

Paul Kyprianou, external relations manager of the Grimaldi Group says that the new vessels being built or on order by 2012 should create a bit of slack in the market, although a lot does depend on whether ship operators decided to keep vessels older than 20 years in operation. “One issue is that stricter emissions limits mean that operators are having to use more low-sulphur fuel, and low-sulphur fuel is more expensive. That means that ships that use more fuel will become increasingly uneconomic and they may be compelled to leave the market.” However, the new regulations are not being introduced everywhere, so the older tonnage might find useful employment in parts of the world where environmental rules are less strict.

Quite a bit of cargo around

K Line’s director of the car carrier division for Europe, Peter Menzel says that with trade on many routes recovering strongly, shortages are now emerging in some sectors of the market. Overall, K Line’s volumes were up 168% in the first five months of 2010 compared with the same period in 2009, with Japan to Asia up 223% and Japan to Europe up 145%. Moreover, he adds, as the industry moved into the peak August to October shipping season, the shortages could become more acute as 2010 progresses. Potential growth spots include Europe and North America to China, Europe to the US, and North to South America. East Europe is also recovering slowly, says Menzel.

“Overall, there is quite a bit of cargo around now,” he continues. “People say that there is a lot of tonnage due to be delivered, but most of the surplus will be in medium sized new-buildings of around 5,000 car capacity mainly in the short term charter or spot market.” Non-specialist operators ordered most of these ships during the boom years. What is emerging, says Menzel, is a shortage of operatorowned larger ships of 6,000 cars and above. Some of the medium-sized ships in the charter market could theoretically be used to plug gaps elsewhere in the market, but he predicts that ship operators will be reluctant to take on long-term charters.

K Line’s own car carrying fleet, roughly 75 vessels strong worldwide, is nearly at full capacity right now. Five new owned vessels, four of 6,000 car capacity and one at 4,000, are being taken into the fleet this year to replaced chartered tonnage, with a similar number to follow in 2011.

K Line will also look to streamline its operations in ports, the aim being to combine ‘economic steaming’ at 16-18 knots with reasonably slick port operations.

But K Line is hampered in these efforts by many of the ports it uses–mostly in Europe–where terminal operators have laid off workers to such an extent that they often hire more untrained workers. Not only has this led to delays in port of up to five days, but also there has been an upsurge in accidents. Paul Kyprianou adds that some Mediterranean ports are also struggling to cope, which has had a negative effect on some carriers. There are few specialised car-handling ports in this region, and many lack dedicate berths and storage or stevedoring. Costs in some Mediterranean ports can also be very high. “Pilotage, towage–they can all have a very big impact on the cost of maritime transport,” he explains. Höegh Autoliners, which currently operates about 70 pure car and truck carriers, will add five 4,900-car capacity vessels by 2012. Although new builds will decrease after this, spokesman Gary Shoesmith said he did not anticipate that this would lead to any significant capacity shortages.

“We still have some flexibility in our fleet and we are looking for new port calls,” explains Shoesmith. He added that Höegh is pleasantly surprised in the recovery in the market so far for 2010 and is predicting a steady increase in trade into 2011.

Like other carriers, Höegh is operating its ships at around 16.5 knots–not so slow as to seriously add to voyage times but with less fuel burn and leaving some capacity in hand in case of port or weather delays.

Shoesmith says that the main concerns over terminal operations are port delays in West and South Africa, where capacity has not kept up with an increase in trade. The new operations in India are, in contrast, working very well, he says. At United European Car Carriers (UECC), the intra- European carrier jointly owned by Wallenius Lines and NYK, head of car sales Bjorn Gran Svenningsen says that there is currently some oversupply in the market, despite some scrapping of vessels. “We think that 2011 is going to be a tough year, but we estimate that in 2012 or 2013 markets will begin to pick up again.”

Many of the car scrappage programmes in European countries have now finished and, despite efforts by some manufacturers to stimulate the market, the picture is not very upbeat. Russia used to be a big market for UECC, which at one stage deployed eight vessels there compared with the current three, though there are signs that car imports are picking up again following government efforts to boost the market. Kai Kraass, chief operating officer at Wallenius Wilhelmsen Logistics, sees “pretty positive development” on almost all trades over the last couple of months. Growth has been mainly on the Asia to North America and the Asia to Europe markets, along with intra-Asia. As far as Asia-Europe is concerned, what he would really like to see is a full recovery in the Russian market, which realistically won’t be until about 2012. Kraass says that operators have reacted in a measured way, taking capacity out but not over-reacting. “Now we see good vessel utilisation, and also the right mix of cars and other traffic, such as high and heavy and break-bulk.” Like other operators, WWL is moving towards much more flexible ships that can take a wide range of different-sized cargoes. The pure car carrying ship could soon be a thing of the past.

For the future, Kai Kraass sees more manufacturing in local markets, such as Russia or India, as well as more outsourcing of outbound logistics. “What we also see is more manufacturers outsourcing logistics services and we’re having a lot more conversations about that.” He adds that specialised makers of electric cars are emerging in North America and Europe and these companies, which lack a logistics ‘history’, tend to be more open to this concept.

Like other operators, WWL sees the higher cost of lowsulphur fuel having an impact, along with tighter environmental regulations generally, particularly as new EU emission regulations start to bite in 2012-2015. “It’s an expensive future if we don’t change our way of working,” says Kraass. Besides adjusting its equipment and ship speeds, WWL is aiming to reduce emissions by developing the concept of ‘super ports’ fed by a hub and spoke network. Radical new technology such as ships partly powered by solar panels could make a real contribution to cutting vessel operating costs.

The one concern above all others

NYK’s Svein Steimler has one concern above all others. “Our running costs have been hugely affected by fuel costs, which have quadrupled over the past ten years. These huge increases in our costs are largely outside our control and at the end of the day, it is a cost increase in our view that should be covered by the consumer as it is with most other commodities. But many car manufacturers believe that, for some reason, these huge increases should somehow be paid for by the shipping carrier.”

NYK is looking for the basis of an understanding among its customers that would streamline the myriad bunker adjustment factors (BAFs) that have mushroomed and made shipping costs extremely opaque. What Steimler envisages is a single, standard clause. Meanwhile, NYK is reviewing its BAFs every two months and in the medium term wants to review surcharges with some of its OEM customers.

He is not talking small numbers. A large car-carrying vessel burns typically 45 tonnes of fuel every 24 hours and standard fuel now costs around $500 a tonne. The gas oil fuel, which many countries now insist on being used in or near their port areas, costs closer to $1,000 a tonne, and low sulphur fuel is also expensive.

Burning less fuel is an answer ultimately, but the new technology that might one day make that possible is also eyewateringly expensive. NYK has set aside Y70bn ($830m) for new technology, such as the project to fit the Auriga Leader car carrier with solar panels. NYK reckons that it is no slouch in the green technology department, but even the panels on the Auriga Leader only generate enough juice to run lighting and other auxiliary functions, rather than power the ship. Ultimately, though, NYK’s goal is to cut its total emissions 50% by 2050 and has a target of a minimum 10% reduction on a per tonne or mile basis from fiscal 2006 levels by 2013. It has worked up a design for a Super Eco Ship, which it hopes to have in service by 2030 as part of that process.

Dennis Manns adds that pressure to green shipping is also coming from the car industry: “We have for some time been working with all of our logistic partners to measure, monitor and reduce their carbon footprint.”

The company has found that the recent opening of its Richmond, California port not only allowed it to reduce car hauling miles to West Coast dealers by more than 1.4m annual miles but service levels as well as operating cost improved. But there is more to increasing capacity than building new ships, adds Kai Kraass; a tighter and more responsive supply chain will play an equal part. “At the moment, at any port you see thousands of cars waiting and waiting. We need to move away from the ‘rush and stop’ approach to logistics, we need more systems and management competence.”

Better communications will allow operators to take early action if there are disruptions such as bad weather or strikes. “We need more investment in systems, which we are doing as an industry, but perhaps it’s got to happen more.” Dennis Manns agrees. “If there was good to come from the economic downturn of last year, I believe it was the enhanced focus of the value of a solid supply chain. At American Honda we have experienced a heightened focus on making sure all of the key components of our supply chain are connecting to make all of us are more successful.”

He adds: “The inconsistency of sales and production from last year really challenged all aspects of our supply chain. However, the actions to improve our business, budget adjustments and just paying attention to details has carried over into this year and I believe makes us more successful.”