Central and Eastern Europe has developed a strong automotive supply base over the past few decades and is now gearing up to support major trends such as electrification

In the decades since the end of the Cold War, Central and Eastern Europe (CEE) has been attracting automotive components suppliers by virtue of its cheap labour, low taxes and convenient geographical location. Now, the region is aiming to maintain or even build on its gains in the face of vehicle electrification, rising global competition and other challenges.

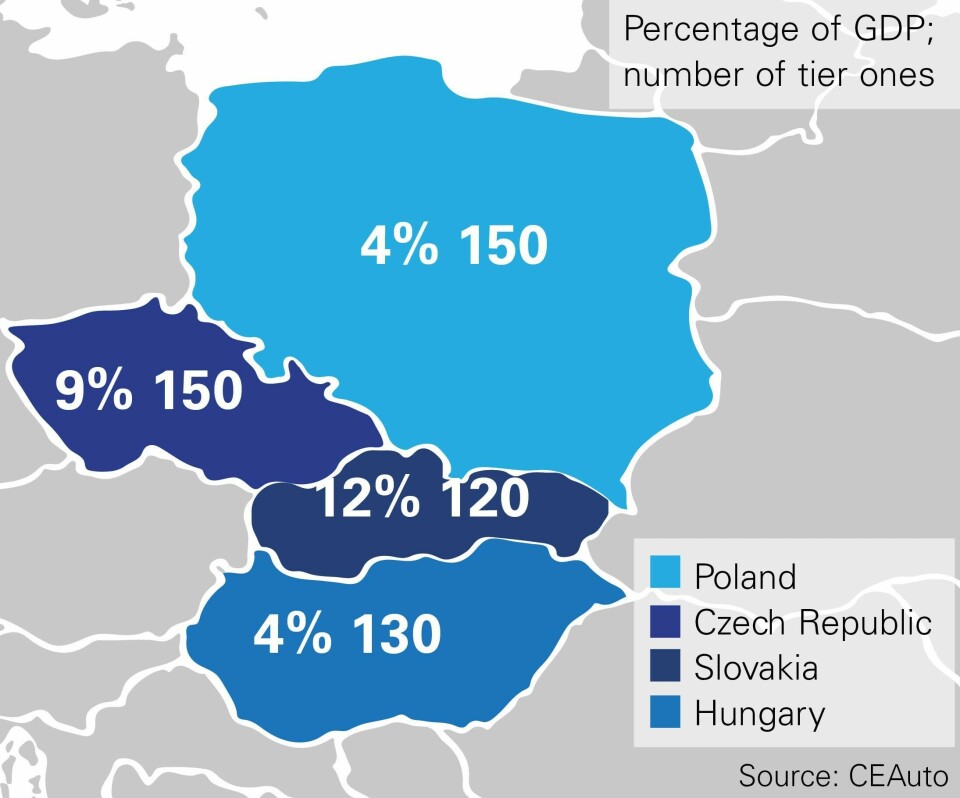

The automotive components industry of four key CEE countries, Poland, Slovakia, Hungary and the Czech Republic, comprises around 550 tier one suppliers, according to consulting agency CEAuto, which is based in the region. There are also between 100 and 150 tier one suppliers in Austria, according to government statistics.

CEAuto estimates that the number of tier one parts suppliers, both major international corporations and local companies, amounts to approximately 130 in Hungary, 120 in Slovakia and 150 in both the Czech Republic and Poland. “It is the largest industry in the Czech Republic and Slovakia, accounting for about 9% and 12% of GDP, respectively, while in both Hungary and Poland it accounts for 4% of GDP,” says Pál Négyesi, managing director of CEAuto.

Advertisement

”Over the past two decades, the supply base in Poland, including the environment around the Gliwice plant, has grown significantly and we are confident it will grow further”

Wojciech Osoś, Opel

In general, the industry in the CEE region is optimistic about the near future. For example, a study by PWC showed that 80% of automotive companies in Austria anticipated sales growth in the coming years. This was the verdict in spite of some serious threats, which these suppliers also acknowledged in their survey responses.

In particular, 38% of companies admitted that their business had started to suffer in the shift toward electrification. One in six participants highlighted a shortage of skilled staff as one of the main threats; nearly 15% of companies raised concerns about rising pricing pressure from OEMs; 12% expressed worries about slow growth in the main sales market; and 25% pointed to regulatory changes in the EU, including those related to Brexit.

Automotive components contribute significantly to the GDP of CEE nations like Slovakia, Czech Republic, Poland and Hungary

“The majority of tier one suppliers’ local operations are situated in the central and western parts of the V4 [Visegrád] countries, relatively close to Germany and other western markets,” Négyesi observes. The Visegrád Group includes the Czech Republic, Poland and Slovakia.

One reason for optimism is that the automotive components industry remains attractive for investors from different countries for a variety of reasons. Négyesi lists the following influential factors: relatively low wages; availability of both blue- and white-collar workers; well-developed infrastructure; close proximity to OEMs; the presence of reliable sub-suppliers and logistics companies; higher education hubs; investment incentives; and a stable political and economic environment. He describes low wages as “still a decisive factor” for suppliers.

Automotive components in CEE are not only serving the needs of localised OEMs, however; significant volumes of components are being exported. For example, according to Alexander Matusek, president of the Automotive Industry Association of Slovakia, 60% of parts made in the country are exported.

“It should be a concern of all governments to establish on their territories a major supply base, as is the case in Slovakia,” Matusek states. He argues that this is “one of the basic pillars of competitiveness and sustainability of the industry”.

EVs put pressure on supply base The global shift towards electric vehicles (EVs) is set to transform the components business worldwide, and CEE is no exception. This is because an EV contains, on average, around 30-35% fewer moving parts than a traditional vehicle.

A source in the region’s automotive industry, who wishes not to be named, says: “We see when it comes to electrification and new ecological standards [that] Europe is ahead of the curve, and this scares some tier one suppliers a lot, because they need to invest a significant amount of money into new technologies to stay in business.”

“The shift in focus to electric vehicles is starting to impact Poland, with existing suppliers modifying their plants and processes to accommodate this change, and new suppliers entering the market”

Andries Retief, DHL Supply Chain

Karolina Konicarova, spokesperson for the Czech Invest Agency, adds: “There are governmental action plans for both e-mobility and AV [autonomous vehicles], and all the OEMs in the Czech Republic are reflecting it; all of them are now offering various types of electric vehicles, including popular SUVs.”

According to Grzegorz Galczynski, strategic industries manager at the Polish Investment and Trade Agency, electrification is now transforming the country’s automotive industry. This will have a big impact on the parts business, because 59% of the country’s automotive production consists of components, with Poland being the leading manufacturer in the region (as well as fourth in Europe as a whole and ninth in the world).

Advertisement

“Poland is actively creating an ecosystem for electromobility as an answer to rising global megatrends. We are currently running 17 electromobility-related projects,” he comments.

Andries Retief, CEO of the CEE division at DHL Supply Chain, agrees that the transformation is underway: “The shift in focus to electric vehicles is starting to impact Poland, with existing suppliers modifying their plants and processes to accommodate this change, and new suppliers entering the market. The increased focus on e-mobility is also driving a higher spend in research and development investment in the automotive sector.”

Electrification is changing the supply base in the CEE region, requiring modifications to plants and processes. Credit: Bosch

Something similar is happening in Slovakia, according to Tomas Meravy, senior analyst at local think tank, Mesa10. “The possible risk from electrification is a hot topic in Slovakia, because of the dependence of Slovakia on automotive [and] the disruption this would cause to the level of employment and the supply chain,” he states.

“My hope is that Slovakia will become a production site for EV batteries. All the producers in Slovakia are heavy on EV plans, including Kia, VW, JLR and PSA, so the ability or inability of Slovakia to become a battery producer will be key in retaining the automotive industry.”

Andries Retief, CEO of the CEE division at DHL Supply Chain, agrees that a transformation is underway. “The shift in focus to electric vehicles is starting to impact Poland, with existing suppliers modifying their plants and processes to accommodate this change, and new suppliers entering the market. The increased focus on e-mobility is also driving a higher spend in research and development investment in the automotive sector,” he states.

Components manufacturers agree that the effect of electrification is so far not being felt in every segment equally. “There is currently no impact of the EV offering on aftermarket parts sales. But one has to notice the new Korean production plant in Poland [which is] fully focused on modern battery production,” comments Andrzej Senkowski, spokesperson for Polish tier supplier Polcar.

“The possible risk from electrification is a hot topic in Slovakia, because of the dependence of Slovakia on automotive, the disruption this would cause to the level of employment and the supply chain”

Tomas Meravy, Mesa10

Paweł Hanczewski, aftermarket country sales manager in Poland for Bosch Automotive, further notes that the growth in the Polish automotive industry has mostly come from imported used cars in recent years, at around 1m units per year. New car registrations have also grown.

“As a leading IAM [independent aftermarket] supplier we benefit from this growth of the market in the sale of spare parts and workshop test equipment as well. Consequently, we have increased our market share in recent years,” he states. Hanczewski says that ICE vehicles still represent the biggest share of the imported and new car growth, with EVs taking just a small percentage.

Global competition heats up Some other world regions, like the Balkans and North Africa, are increasingly regarded as the new hotspots for low-cost automotive manufacturing, being located relatively close to the key sales markets and offering good investment terms to components suppliers. In the coming years, CEE will have to prove that it has not lost its competitive edge.

“Some suppliers are shifting their production out of western Europe and even China to CEE countries, while some low added-value production is being transferred from CEE to the Balkans, with [its] significantly cheaper labour force,” says CEAuto’s Négyesi.

Paweł Hańczewski of Bosch says that ICE vehicles still represent most imported and new car growth in Poland. Credit: Bosch

“Supportive measures in taxation and incentive systems have been initiated by [CEE] governments to ensure the transition from low added-value production to products and services with high added value and to get more involved in R&D activities, as well as to create competitive investment conditions as the sector is preparing for extensive electrification.”

Pascal Trummer, vice-president of sales and marketing, Europe, at Magna (see box below), agrees: “We see key players building up a new footprint in North Africa in order to be able to leverage this rising competition in terms of resources and wages.”

Advertisement

Nevertheless, local analysts and OEMs believe that the automotive components industry in the CEE region will be able to compete.

“Nowadays, Poland is offering a competitive supply base in the automotive sector and its dispersion ensures the optimal delivery cost. The deliveries from Poland represent a large percentage of our overall turnover,” says Wojciech Oso, spokesperson for the Polish arm of Opel.

“CEE remains attractive for the supplier base because of its skilled people. However… key players [are] building up a new footprint in North Africa in order to be able to leverage rising competition in terms of resources and wages”

Pascal Trummer, Magna

“The quality of the components is very important to us, just as much as its production cost; that, in turn, is equally as important as the delivery cost. Over the past two decades, the supply base in Poland, including the environment around the Gliwice plant, has grown significantly and we are confident it will grow further,” he continues.

Marlena Szmajda, spokesperson for the Polish Automotive Industry Association says: “The sheer size of the country, its regional diversity and access to human resources are special advantages of Poland in the Central Europe region at a time when the struggle for talent translates directly into the possibility of further development for automotive companies.”

She notes that Poland has rapidly developed its parts exports since 2013, seeing growth of 67% over five years. In 2017, the country was responsible for 3.2% of global automotive parts exports by value, amounting to $3.6 billion.

CEE offers skilled labour and low costs, but is now facing competition from regions such as North Africa. Credit: Bosch

Holger Wilhelm, executive vice-president, automotive, at Imperial Logistics International, notes the potential for investment from foreign manufacturers that have not yet made in-roads in CEE. “China has a track record of success in penetrating all manufacturing sectors globally, so there is good reason to suppose that they will try to repeat this in the automotive field – both as OEMs and tier suppliers.”

“So far, this process is in its relative infancy, and the consumer will be the final arbiter of their success or otherwise. Europe is home to many quality manufacturers and has traditionally proven tough to penetrate from outside. But some, particularly from Japan and Korea, have already succeeded, so perhaps China can, too,” he adds.

Wilhelm believes these companies will need to make a show of commitment, such as opening local production facilities, focusing on low-emissions vehicles, and building their environmental credentials to match those of the European manufacturers.

Opportunities for logistics providers Just like the automotive components suppliers, logistics providers, such as Imperial, seem optimistic about the prospects in CEE. “Overall, business has been strong for our automotive operations, and we continue to win new contracts and expand existing ones despite an obvious cooling in the global market,” says Wilhelm.

Imperial is seeking geographic expansion and aims to grow alongside its major customers, for whom CEE is “a major focus”, he explains, though he foresees some challenges alongside the opportunities.

“Current market headwinds are coinciding with our sector, confronting crucial decisions on when, where and how to adapt to emissions-free powertrains – as well as looking at greater use of digitalisation and big data to make businesses more efficient and market-responsive. These are challenges that will require heavy investment by vehicle manufacturers, but they are also opportunities for us to add further value for those customers,” Wilhelm explains.

“The market in Eastern Europe is competitive and under constant price pressure with carriers coming from the Ukraine, Romania and Bulgaria offering low-cost options which drive down price and margin”

Stuart Stobie, Priority Freight

For DHL’s Retief, the automotive industry continues to make progress in terms of driving higher value, efficiency, optimisation and quality. “There is a definite trend to deploy newer technology in the automotive factories as well as in the logistics industry. With low unemployment levels in Central Europe and Poland, an over-reliance on manual labour would be prohibitive and, as such, deploying technologies and innovation is a critical investment,” he states.

“These investments enable employees to provide value-adding services rather than repetitive tasks, thus further developing their skillset and improving productivity for the automotive and logistics sectors,” he continues.

There are also some changes in product flows through CEE as well as to destinations outside the region. “We see an increase in the number of car and part manufacturers that are exploring long-distance sequencing of parts for production. While this could potentially reduce a manufacturer’s flexibility, the reduction in storage and handling cost is attractive in a very competitive industry,” explains Retief. “For the same reason, there is an increase in manufacturers investing in automated guided vehicles to increase accuracy and overcome potential labour shortages in the region.”

Priority Freight has opened an office in Bratislava, Slovakia. It serves three OEMs and several suppliers. Credit: Priority Freight

Meanwhile, Priority Freight opened an office at Bratislava Airport late last year, from which it now offers expertise in time-critical services, road freight, airfreight, onboard couriers and aircraft charters. “The office has been successful and we now deal with three OEMs and a number of tier one customers. We hope to treble in size again in the next year, and I believe it is important to operate a local office in order to develop relationships, trust and understanding of the local market,” says Stuart Stobie, director of Priority Freight.

Low unemployment causes some issues for employers in the west of Slovakia, Stobie explains, but Priority Freight has had the same team since the launch and has continued to add more resources; he says good logistics skills are available in the area.

“The market in eastern Europe is competitive and under constant price pressure, with carriers coming from the Ukraine, Romania and Bulgaria offering low-cost options which drive down price and margin,” Stobie states.

“There are more tier one and two suppliers moving into the market almost daily, but supply chains have been relatively well organised this year, [coping] with Brexit uncertainty, less diesel cars and more focus on electric over new model combustion engines. I expect next year to be busier, particularly with further market consolidation and more new models likely to be manufactured,” Stobie states.

Ultima Media’s Business Intelligence Unit has produced a detailed report on the top 20 tier suppliers worldwide, and the challenges they face. Download it here.

1.0.0.20

Q&A: Pascal Trummer, vice-president sales and marketing Europe, Magna

Pascal Trummer, Magna

How has business been for Magna in the CEE region over the past few years? Magna has been successful in developing our business in the CEE region. Our plants in Poland as well as in Slovakia have been extended and a new paintshop in Slovenia has been launched recently. Actually, we have 34 plants in this region.

What are the main trends in the automotive components industry? The automotive business is facing big challenges, starting from the move from internal combustion engine to electrification up to the business model itself shifting from ownership to more mobility services. At the top, tariff discussions [between the US and EU] are sharpening the overall market situation. All these factors lead the OEMs to improve their costs and a few OEMs are shifting production to CEE in order to leverage their costs. On the one hand, this gives new opportunities for the supplier base, however on the other hand this could bring more tension over the availability of resources as well the situation on wages.

Is competition in this part of Europe on the rise? CEE remains attractive for the supplier base because of its skilled people. However, the limit on additional resources will be challenging for keeping a competitive footprint in the long term. These resources are skilled people as well as programme management with knowledge of automotive industry. We see key players building up a new footprint in North Africa in order to be able to leverage this rising competition in terms of resources and wages.

How are Magna’s logistics organised in CEE? Our logistics network is optimised in the best way possible at a plant and corporate level. Depending on the size of the shipment, Magna uses grouped transport, milk runs or full-truck loads. In a certain region, smaller shipments are picked up by a selected service provider using its own network. For mid-size consignments, Magna plans milk-runs; a truck picks up shipments at two or three suppliers on a route. And finally, Magna runs full truck loads for high-volume suppliers.

Which transport modes are used? Due to transport volume, the main mode of transport is truck. In general, we [face] the huge challenge of sustainable transport. E-trucks are not yet available (just electrified diesel trucks) and LNG [liquified natural gas] refilling station availability is very poor. LNG trucks are more expensive than diesel trucks (over €40k), e-trucks are very expensive and FC [fuel-cell] trucks cost a fortune.

The target must be to improve sustainability at the same cost level. Any improvements in rail infrastructure and multi-modal rail service products will help. In general, rail service providers have to provide additional services so that smaller shippers can participate in rail transport. There aren’t so many shippers that are able to fill an entire block train.