The UK automotive industry faces its toughest year yet, with production down, high energy costs impacting competitiveness, and confusion over EV government incentives.

The UK automotive industry is under severe pressure, with

production down 11.9% year-on-year and the worst first-half performance, excluding

covid, since 1953. The industry is facing challenges including the shrinking of

export volumes, high energy costs, low domestic supply of EV components, and an

imbalance in supply and demand for EVs. On top of this, there is confusion

spanning from customers to OEMs and logistics planers about which vehicles

qualify for EV mandates. However, recent government funding could provide hope

for recovery.

Declining vehicle production in an export-heavy UK market

In the first half of this year, new vehicle manufacturing declined

by 11.9% to 417,232 units, according to the latest figures from the Society of

Motor Manufacturers and Traders (SMMT).

Advertisement

It has been one of the toughest periods in the history of the UK automotive industry.

Mike Hawes, chief executive of SMMT

The UK’s output of cars this year to date declined by 7.3%

to 385,810, while production of commercial vehicles almost halved, declining by

45.4% to 31,422 units, due in part to restructuring at commercial vehicle

production plants.

The overall year-on-year decline was softened slightly by a

6.6% increase in car production in June compared to the same month last year. In

June 2024, model changeovers and supply chain issues held back output,

accounting for the YoY increase.

EV production not only saw a rise

of 1.8% in the first six months of the year, but it also took on a record share

of overall production, with EVs and hybrids accounting for more than two in

five cars produced in the UK, at 160,107 units.

However, there is a mismatch

between EV production intent and logistics capability. The domestic EV supply

chain is running short on components including e-axles, wiring and battery casings.

Local production of EV batteries is still scaling, with assurances made for AESC’s

second gigafactory in Sunderland, but is not yet widely operational. On top of

this, reverse logistics for defective battery modules, or for end-of-life

batteries to be recycled, is still an afterthought.

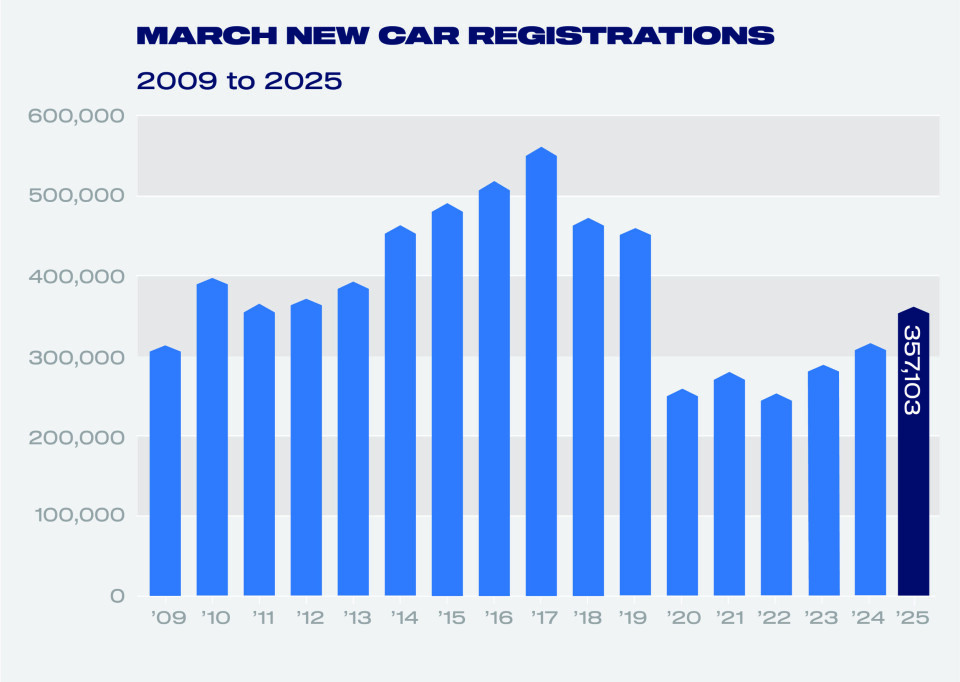

New car registrations in the UK in March year-on-yearSMMT

While the forecast for the full year

has been revised from 818,000 units to 755,000, the SMMT does expect a recovery,

albeit a slow one, over the next few years. In a press briefing, Mike Hawes,

chief executive of SMMT, said: “We do not expect to get back to a million

[units produced annually] before the end of the decade under current conditions

and current participants.”

For this to happen, there would need to be new

entrants in the market, he said. However, the SMMT does expect to see

production rise to more than 800,000 units produced next year, and 850,000 by

2030.

As a result, those involved in the

FVL sector, including vehicle holding yards and ro-ro terminals, must prepare

for volatile flows.

Export growth shrinks, despite

being dominant over domestic sales

When it comes to passenger vehicle

flows, the UK leans heavily towards exports rather than domestic sales, with

76.9% of output headed overseas. Of this, the UK moves vehicles mostly to the

EU (54.4%) and the US (15.9%), with the latter being the UK’s biggest single

export market. In light of this, the UK’s recent trade deal with the US is

vital for the region’s automotive industry.

“Global economic uncertainty and

trade protectionism have taken their toll on automotive production across the globe,

with the UK no exception,” said Hawes. He added that while the UK’s production

figures are not unexpected, they remain “very disappointing”.

Export volumes for vehicles are

shrinking, down 4.3% in the first six months of 2024 YoY, which Hawes said “you

would expect, given the disruption, especially in exports to the US”. This led

to manufacturers having to reprioritise market destinations and forecast routes

dynamically, which affected lead times, mode choice and inventory planning.

Now the disruption has “largely

resolved” following the UK-US deal, according to Hawes, which “keeps the wolf

from the door” and provides some relief to the UK industry. But the possibility

of new, more competitive Chinese entrants to the market means that FVL flows

need to be redesigned to support flows likely destined for the EU or the Middle

East, rather than the US.

EV government grant sparks

industry confusion

While the UK government has injected

cash to boost incentives for domestic EV production, it has caused confusion

among OEMs and logistics providers as to which models can qualify for the

government funding – particularly since it was devised, developed and announced

without consultation to the industry.

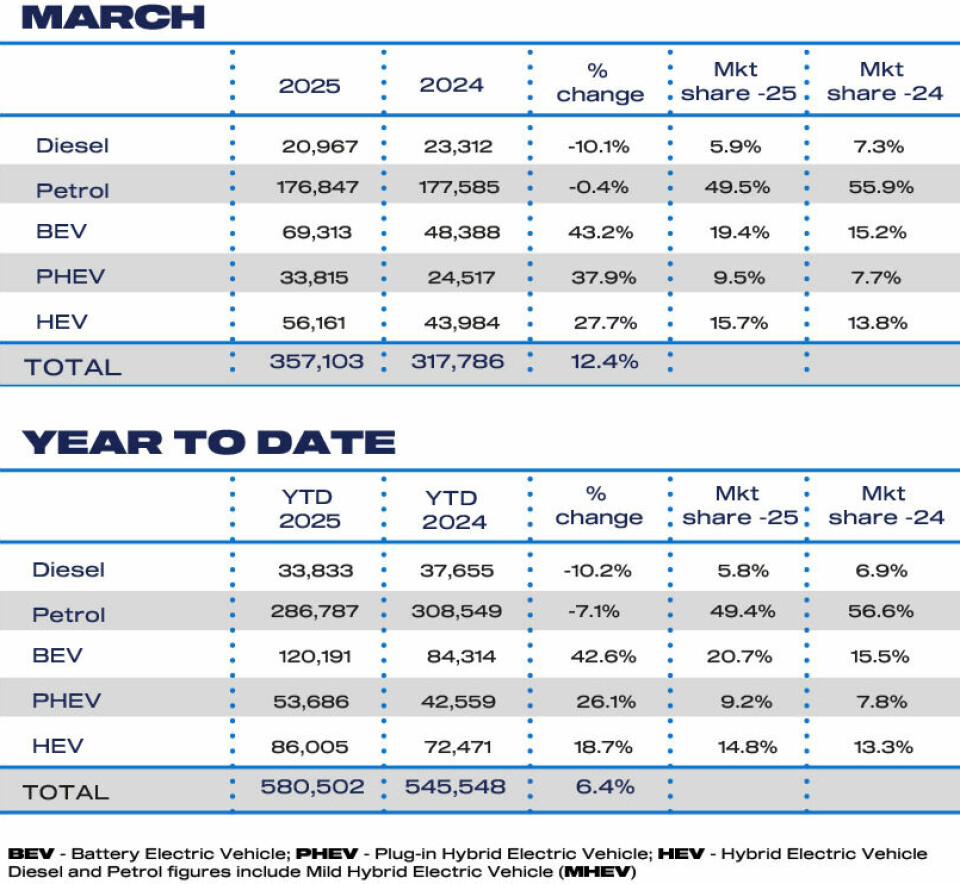

Units of model types produced in the UK year to date 2025SMMT

The grant, which is a £650m ($880m) consumer subsidy, separate from

the government’s recent £2.5bn DRIVE35 industrial initative, offers a

reduction of up to £3,750 off a new EV priced under £37,000, or a second band

reduction of £1,500 for models with slightly lower environmental performance.

Chinese-made vehicles will not be eligible for the discount as they do not pass

the government’s rules on environmentally sustainable manufacturing. Tesla will

also not be eligible, as its prices are above the first band cap.

Advertisement

While the SMMT welcomed support in

the EV market, Hawes said it is a “complex” grant. He said: “I think the

industry is still trying to get clarity behind its application. It is eligible for

all, including fleets, businesses, private grants, but what we were clearly

asking for, for a number of months, is support focused on the private consumer

because that’s where the big shortfall is in demand."

The government has not disclosed

which brands or models will be eligible, but the department for transport (DfT)

said 33 EV models will be available for less than £30,000.

It has committed to

publish the list of vehicles that qualify for the grant by 11 August, just one

month out from the second biggest registration month in the year. This makes it

difficult for OEMs to plan ahead, as many will have their volume forecast in

place already, without knowing if they, or their competitors, will qualify for

a price reduction.

It undermines your ability to forecast for the biggest month and beyond for the rest of the year.

Mike Hawes, chief executive, SMMT

Hawes added: “Right now, your

local car dealer can’t tell you for sure whether the car you’re looking at

thinking of buying will qualify.”

The uncertainty adds another

visibility gap in forecasting ability, putting the sector in “pre-positioning

limbo” and making order assumptions made months ago potentially invalid. It

also means that the FVL sector cannot adequately forecast demand and capacity,

risking storage bottlenecks, or, on the flip side, underused pre-delivery

inspection (PDI) centres.

“It undermines your ability to

forecast for the biggest month and beyond for the rest of the year,” Hawes

said. “So, for some manufacturers, the impact of that is their route to mandate

compliance now looks worse.”

Reducing energy costs remains key to unlocking UK competitiveness

For the UK market to see a return

to growth and competitiveness, reducing energy costs must be the number one

priority, according to the SMMT.

UK-based OEMs and parts

manufacturers are paying up to double what their EU peers do for energy. Because

of this, the SMMT said, Chinese manufacturers are investing instead in the

likes of Hungary, Turkey and Spain, where energy costs less. It also means that

domestic plants that could potentially expand are instead looking to reshore in

less cost-intensive countries and divert product allocation there. This is

forcing the supply chain to reshape flows, consolidating inbound logistics hubs

closer to UK hubs for buffers and cost controls.

“That is something that remains a

focus to improve our competitiveness,” Hawes said.

With rapid delivery and the right conditions, UK automotive can reverse the current decline

Mike Hawes, chief executive, SMMT

However, the foundations for

growth are strong. “The industry is moving to the technologies that will be the

future of mobility, our engineering excellence, highly-skilled workforce and

global reputation are strengths, and we have an industrial strategy with

advanced manufacturing and automotive at its core,” Hawes said. “With rapid

delivery and the right conditions, UK automotive can reverse the current decline

and deliver the jobs, economic growth and decarbonisation that Britain needs.”