Executives we spoke to…

BMW Group

BMW Group

Wolfgang Baumann, vice-president of parts logistics management, has been with the company since 1985 and spent most of his career in sales planning and commercial operations in Germany, before moving into his current role in service parts logistics in 2010. While he claims not to be a logistics guy, he has been instrumental in leading a restructuring of BMW’s global service parts management. (See our recent extended interview with Baumann.)

Carlisle & Co

Carlisle & Co

David Carlisle, chairman, is a consultant specialised in dealer services and runs benchmark studies that measures service parts logistics performance and delivery in the US and global regions. In 1997, the company shifted its data collection methods to involve vehicle manufacturers via benchmarking steering committees. The ensuing transparency was a “shock to the system” for many carmakers at the time, he says.

Opel/Vauxhall

Opel/Vauxhall

Kai Rabe, European aftersales logistics manager, has worked for the carmaker in various functions for the last 25 years, most of this in aftersales but also in dealer network development and customer care centre development. Twenty years ago, Rabe had just completed a move from the aftersales supply chain to vehicle sales, looking after dealers. He moved back into aftersales logistics about a decade ago.

Toyota North America

Toyota North America

Neil Swartz, vice-president and general manager of service parts and accessories operations, joined the company in 1985 as service marketing manager. He has since held numerous service and parts positions including national dealer development manager, and national sales and field operations manager. Prior to his current position, Swartz was corporate manager for Toyota’s North American Parts Operations unit.

Volkswagen Group of America

Volkswagen Group of America

Anu Goel, executive-vice president, group after sales and service, is a veteran in the service parts industry. Goel worked in 17 different aftermarket roles in 23 years with Ford, later also working in service parts logistics for CNH. Twenty years ago, he was just moving from being general manager at a Ford depot in Atlanta to leading a parts centre in San Francisco. He joined Volkswagen in 2012, and has been in his current role for two years.

Service parts part 1: Moving fast towards the customer

What have been some of the most important changes for service parts logistics compared to 20 years ago?

What have been some of the most important changes for service parts logistics compared to 20 years ago?

Executives and experts agree that the shift towards more customer-focused logistics, including more frequent order and delivery, has transformed many aspects of aftermarket logistics, leading to a significant decrease in lead times in both inbound supply and, especially, to dealers.

Volkswagen Group’s Anu Goel describes a fundamental switch in both dealer and supply order approaches. In the early 1990s, carmakers encouraged dealers to order parts once a week in bulk, with next-day, emergency orders available from express providers. In the 1990s and early 2000s, on both sides of the Atlantic, OEMs switched to dealers ordering parts daily with them arriving overnight by the following morning. In the US, 11 out of the 16 major carmakers now offer next-morning delivery as standard, according to data from Carlisle & Co, a consultancy and research group that compiles service benchmarks.

With most OEMs committed to next-day delivery, carmakers continue to target later order cut-off times for dealers, with some now able to order in the early evening and still receive parts the next day. Same-day services to major markets are also increasingly common for a number of major carmakers in Europe, the US and China.

The root of these changes has been a switch to prioritising customer lead times. Consumer expectations for faster, more reliable delivery, particularly from the likes of e-commerce giants Amazon or eBay, have influenced carmakers’ operations. Neil Swartz at Toyota also cites the financial crisis and subsequent recession as a “call to action” to strengthen the focus on customers, and subsequently move to a point where some deliveries could be made within hours.

The shift to daily deliveries has come with other structural changes over the past two decades in the way that carmakers approached their service parts supply chain. David Carlisle, who has long collected data on delivery and service, points to a more rigorous and strategic approach to storage and warehousing, including adopting TPS processes.

Carlisle also cites dramatic improvements in inventory management thanks to ‘segmented warehousing’, pioneered in the US around the turn of the century by Ford under the leadership of Don Johnson, then head of global parts logistics. This approach means allocating parts to different warehouses depending on whether they are fast or slow movers, which helps carmakers to reduce overall inventory. Anu Goel, who worked for Ford at the time, recalls how the company added new buildings to the handle “the big uglies” – parts such as sheet metal and powertrain that took up a lot of space but were

Carlisle also cites dramatic improvements in inventory management thanks to ‘segmented warehousing’, pioneered in the US around the turn of the century by Ford under the leadership of Don Johnson, then head of global parts logistics. This approach means allocating parts to different warehouses depending on whether they are fast or slow movers, which helps carmakers to reduce overall inventory. Anu Goel, who worked for Ford at the time, recalls how the company added new buildings to the handle “the big uglies” – parts such as sheet metal and powertrain that took up a lot of space but were  less frequently ordered and depended on more complex repairs. By separating out these parts, fast-moving collision parts could be kept together in more efficient warehouse operations. Goel estimates that inventory savings from such an approach can be up to a third.

less frequently ordered and depended on more complex repairs. By separating out these parts, fast-moving collision parts could be kept together in more efficient warehouse operations. Goel estimates that inventory savings from such an approach can be up to a third.

Segmented inventory is not universal among all parts and distribution centre operations, but has become more commonplace, according to Carlisle. It is especially evident in large, central parts operations, including Ford’s in North America, as well as large global parts centres such as the Volkswagen Group’s original parts centre (OTC) in Kassel, Germany, and BMW’s central distribution centre (ZTA) in Dingolfing, Germany. BMW’s Wolfgang Baumann cites the restructuring of the ZTA over the past two years. Among the key changes was the opening of a new parts warehouse close to Munich airport dedicated to slow moving parts.  The facility covers around two-thirds of BMW’s contemporary and classic models and considerably freed up space from the ZTA’s main building in Dingolfing. As it is close to the airport, the centre can also better respond to express demand since most orders for these parts have specific customers and require air freight. At the same time, BMW opened another warehouse with BMW’s 3,500 most common part numbers, including wear and tear parts, oil filters and brake discs.

The facility covers around two-thirds of BMW’s contemporary and classic models and considerably freed up space from the ZTA’s main building in Dingolfing. As it is close to the airport, the centre can also better respond to express demand since most orders for these parts have specific customers and require air freight. At the same time, BMW opened another warehouse with BMW’s 3,500 most common part numbers, including wear and tear parts, oil filters and brake discs.

Executives note the increase in data availability and visibility across inventory and ordering as a major step forward. On the whole, carmakers have become much better at collecting and analysing the data in their supply chains, from order fulfilment to sales forecasts.

What hasn’t changed as much as you would have expected?

OEMs are spending more on logistics compared to 20 years ago but overall logistics spending is down, relative to total sales

While information flow has improved, experts admit that they have not entirely seen the benefits from improved technology and IT that they would have hoped for, with gaps in inventory visibility as well as for transport.

Volkswagen’s Anu Goel says most of the industry’s systems are still based on “batch processes”, so that visibility comes at the beginning or end of a process, and not in-between. Such information is not always critical – Goel doubts that the company could do much about an overnight dealer delivery that gets stuck in the snow at 02.00 in the morning – but there are cases when knowing about disruptions can allow for alternatives.

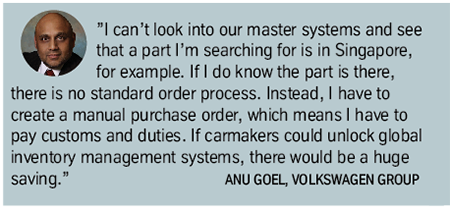

Goel also sees gaps in global inventory management, particularly when it comes to viewing parts availability between regions, where there is also no established mechanism to transfer the parts as simply as possible.

Goel also sees gaps in global inventory management, particularly when it comes to viewing parts availability between regions, where there is also no established mechanism to transfer the parts as simply as possible.

Goel adds that most OEMs use legacy IT systems that communicate poorly with third parties and new software. Neil Swartz also says he would have expected better integration between software and hardware, noting that the promise of ‘plug and play’ has not materialised.

At Opel, Kai Rabe notes that automation uptake in warehouses has been much slower than he would have thought. In fact, David Carlisle thinks one of the most encouraging developments of recent years has been the “death of old-style automation” – mainly equipment from the 1980s and 1990s like goods-picking carousels that proved ineffective.

There are other disappointments. Swartz says that container ships have become substantially larger, but there has been no benefit to lead times. Meanwhile, not every aspect of the supply chain is as customer focused as it has to be in today’s customer-first environment.

Has the cost that logistics represents in aftermarket increased, decreased or stayed the same over the past 20 years?

Carmakers and experts agree that overall spending on freight and transport costs has gone up, driven by faster, dedicated dealer services to reduce lead times, as well as input costs such as warehouse space and labour. Neil Swartz at Toyota cites higher fuel costs and a shortage of labour in parts of the US as factors.

Part numbers have also increased substantially, contributing to the need for more warehousing and more complicated picking and sorting. At BMW, Wolfgang Baumann confirms that the carmaker’s global part numbers have risen from about 165,000 around the turn of the century to around 400,000 today. Other brands report strong growth as well – a current spate of new SUV launches for Volkswagen and Audi are set to increase part

Part numbers have also increased substantially, contributing to the need for more warehousing and more complicated picking and sorting. At BMW, Wolfgang Baumann confirms that the carmaker’s global part numbers have risen from about 165,000 around the turn of the century to around 400,000 today. Other brands report strong growth as well – a current spate of new SUV launches for Volkswagen and Audi are set to increase part  numbers further, for example.

numbers further, for example.

Other cost rises have followed increases in recalls and safety campaigns, from a number of safety-related recalls to Takata airbags and the ongoing Volkswagen diesel scandal. Executives points to number of factors, such as increased government regulations, as factors in rising campaigns. Such recalls are  often tricky to manage, as they may require urgent communication to customers but lack a technical fix, says Goel. Neil Swartz calls special service campaign parts the “most customer critical” in the supply chain, often requiring bespoke processes outside normal network flows.

often tricky to manage, as they may require urgent communication to customers but lack a technical fix, says Goel. Neil Swartz calls special service campaign parts the “most customer critical” in the supply chain, often requiring bespoke processes outside normal network flows.

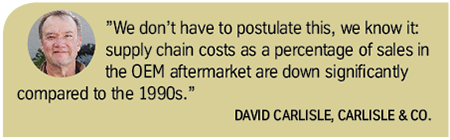

However, executives say that despite higher freight, recall and warehouse spending today, logistics costs are generally lower as a percentage of sales. According to Swartz, Toyota has seen this ratio drop compared to the early 2000s. Kai Rabe says that Opel has seen a similar decrease in logistics costs as a proportion of aftermarket sales over the past decade. Data collected by Carlisle validates these assessments, at least for the US.

Most executives think that the investments made by the industry in more just-in-time supply and delivery have effectively paid for themselves. Anu Goel says that prior to the switch to overnight, dealers had the option of making standard, weekly orders, with an overnight rush order option. Carmakers incentivised dealers to order weekly as they typically only offered discount purchases on standard orders, which ultimately meant carmakers encouraged dealers to opt for the slowest possible service.

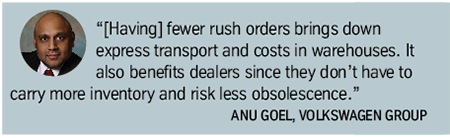

There were a number of negative consequences in pushing for this slower service. Firstly, it discouraged customers from using dealerships, as they were more likely to wait several days to have their vehicles repaired. But it also made dealers more likely to use expensive rush orders. That meant high transport costs, including air freight. Goel points out that rush orders are the least efficient in a warehouse, as they require dedicated picks by workers, while emergency air freight shipments tend to have higher damage rates.

In switching to next-day overnight delivery, dealers moved away from relying on rush orders, using them only to get parts unavailable in their nearest distribution centre, or for an order made after a cut-off time. According to Goel, the ratio of standard versus emergency orders has shifted from 80:20 without overnight delivery as standard to 95:5 today.

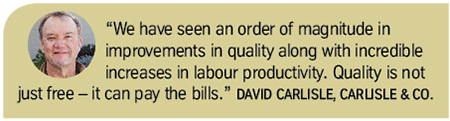

David Carlisle also credits the move towards TPS in warehouse operations and quality improvements with reducing overall costs.

Since the 1990s, how would you describe the development of order-to-delivery lead times to dealers?

David Carlisle offers a potted history of the evolution of carmaker’s dealer delivery services for the aftermarket. In the 1950s, the average lead time for many dealer orders could be up to several months; by the 1980s, lead times decreased to a matter of weeks, coming down further to days in the 1990s, and to overnight in the 2000s. Now, some OEM parts centres are able to fulfil orders within a matter of hours.

The switch in service levels has happened at different stages depending on the manufacturer and region. While Ford would have been among the first to switch in the US to overnight delivery around the turn of the century, Volkswagen Group made the switch in the US in 2013, says Anu Goel, a year after he joined the company.

The switch in service levels has happened at different stages depending on the manufacturer and region. While Ford would have been among the first to switch in the US to overnight delivery around the turn of the century, Volkswagen Group made the switch in the US in 2013, says Anu Goel, a year after he joined the company.

In the US, Toyota also moved to daily ordering methods around 20 years ago, with overnight, unattended delivery to dealers  prior to them opening, according to Neil Swartz (daily orders were already standard in Japan). The carmaker has since increased order cut-off times considerably, with nearly 85% of Toyota’s US dealers able to order at 16.00 or later, and still receive delivery before 07.00 the next morning. The carmaker has also extended same-day delivery services to a growing share of its network.

prior to them opening, according to Neil Swartz (daily orders were already standard in Japan). The carmaker has since increased order cut-off times considerably, with nearly 85% of Toyota’s US dealers able to order at 16.00 or later, and still receive delivery before 07.00 the next morning. The carmaker has also extended same-day delivery services to a growing share of its network.

Carmakers have also adjusted inbound supply order and logistics strategies. David Carlisle says that most carmakers now follow TPS principles insofar as possible for parts orders, including more frequent order and delivery, as well as more targeted ordering based on inventory segmentation.

Neil Swartz at Toyota confirms that the company has made more efforts to apply its namesake production processes to service parts in North America, including an increased order frequency that has reduced inbound lead times. While he acknowledges that parts ordering is not yet a daily process to the level that would be seen by Toyota plants, his division is aspiring to approach a “manufacturing-level TPS”, the realisation of which will depend on close partnership with suppliers and logistics providers.

However, even as carmakers have improved inbound lead times and logistics flows, the reality is that aftermarket volume is simply much lower than for production. As Volkswagen’s Anu Goel points out, while production orders of parts might number 1,000 or 10,000 units at a time, aftermarket orders are often as few as 10-15 parts. As such, suppliers still tend to wait to ship parts until they can combine them with other flows, which keeps OEMs from progressing to more of a daily or hourly ordering process.

Along with improving delivery lead time to dealers, OEMs have increased inbound parts order frequency

One way that carmakers are working to improve inbound supply is by combining it where possible with production parts. Ford has made a specific effort to do this both in ordering, production and logistics for several years now. Toyota has recently started to work more with inbound and production logistics teams, including combining crossdocks and milkruns where feasible. This collaboration has been fostered at the company in part by the recent consolidation of Toyota’s North American sales, production and aftermarket functions at its new headquarters in Plano, Texas.

BMW has made efforts to improve its regional inbound supply. Just this past summer, for example, it opened the first stage of a continental distribution centre (ConDC) in Spartanburg, South Carolina, close to its assembly plant in Greer. At this new type of facility for BMW, locally sourced parts in North America will move directly here for crossdocking and quality checks before moving onto regional parts centres for distribution, rather than being centralised at the ZTA in Germany first. Such a facility drastically reduces the inbound lead time for regional parts by as much as 80%, as well as saving on logistics costs.

According to Wolfgang Baumann, building such a new flow required tight integration of BMW’s production and aftermarket systems, with shared suppliers and logistics providers for the plant serving the ConDC. This collaboration helps make faster supply possible, since suppliers sending shipments to Greer typically only send less than 1% of parts ordered to the ConDC. BMW is currently planning a similar ConDC for China. Both ConDCs will eventually export parts directly to international locations, again decentralising a process currently concentrated at the ZTA.

According to Wolfgang Baumann, building such a new flow required tight integration of BMW’s production and aftermarket systems, with shared suppliers and logistics providers for the plant serving the ConDC. This collaboration helps make faster supply possible, since suppliers sending shipments to Greer typically only send less than 1% of parts ordered to the ConDC. BMW is currently planning a similar ConDC for China. Both ConDCs will eventually export parts directly to international locations, again decentralising a process currently concentrated at the ZTA.

What do you anticipate will be the most significant developments for service parts in the coming decade?

Executives are looking to continue on the path of customer service, manage rising competitive threats, as well as adjust aftermarket service to reflect the changing concepts of mobility and vehicle ownership. Such areas bring plenty of risk for carmakers and logistics providers, but also opportunities.

At Toyota, Neil Swartz thinks carmakers should work together more, whether in protecting their brands or running joint logistics. Such collaboration would help OEMs pool their strength against competitors for non-original parts.

Opel’s Kai Rabe thinks systems and data integration across the value chain will be important, driving transparency thanks to more visibility in inventory and transport, as well as control as data analytics and forecasting improve.

Aftermarket executives predict the move to electric vehicles and 3D printing could radically shake up current service parts operations

Others point to wider technological and cultural changes gripping the automotive industry, and anticipate that the impact for service parts could be radical. At Volkswagen Group, for example, Anu Goel anticipates that the planned rise in electric vehicle offerings could reshape the aftermarket supply chain. Firstly, OEMs’ most common, profitable aftermarket sales are collision parts, as well as certain servicing like oil changes – electric vehicles have far fewer parts and don’t require oil.

And then there is also the question of the lithium-ion battery, which is expensive, heavy and highly regulated in terms of its transportation. At BMW, Wolfgang Baumann admits that the company is currently studying the best ownership and service models for batteries.

Goel also points to the potential role that 3D printing could play in the aftermarket. While he acknowledges there is a risk, including over intellectual property rights and distribution, over the next 5-10 years he does not envision 3D printing will play a major role in replacing major parts. Rather, it could be an effective technology to provide rare or classic parts, which currently take up space in distribution centres but do not sell in high numbers.

Perhaps the biggest shake-up will come as the notion of mobility itself continues to change. David Carlisle thinks that vehicle sharing could significantly increase, especially once autonomous cars start to gain critical volume. This change would push more consumers away from ownership and towards fleet membership – a dynamic that tends not to include specific service visits to dealers. In response, Carlisle thinks that carmakers and dealers will need to adjust to serve fleet customers, including better segregating dealership work clusters to accommodate more ‘express work’, for example, which will also require more flexible order and delivery processes.

Perhaps the biggest shake-up will come as the notion of mobility itself continues to change. David Carlisle thinks that vehicle sharing could significantly increase, especially once autonomous cars start to gain critical volume. This change would push more consumers away from ownership and towards fleet membership – a dynamic that tends not to include specific service visits to dealers. In response, Carlisle thinks that carmakers and dealers will need to adjust to serve fleet customers, including better segregating dealership work clusters to accommodate more ‘express work’, for example, which will also require more flexible order and delivery processes.

To maintain dealer loyalty, especially for luxury brands, Carlisle also thinks carmakers will have to expand offerings to include more ways to save customers trips to dealers, such as home pick-up and delivery, services that he thinks many customers will pay for. If carmakers don’t further adjust to the changing landscape for mobility and service, they are likely to fall further behind independent and online retailers.