Supply Chain Conference executive report: A connection worth more than the sum of its parts

The first Automotive Logistics Supply Chain conference explored the extreme complexity of production and service parts logistics across North America. Amid rising global and regional flows, opportunities for freight consolidation and new ways of collaborating across the industry emerged. Christopher Ludwig reports from Atlanta, Georgia.

[sta_anchor id="1"]The growth in the automotive industry in North America has not just represented an increase in volume across the parts supply chain – although, with sales and production expected to rise for an unprecedented seventh consecutive year, there are plenty of capacity issues in tier supplier and logistics capacity. Perhaps even more significant, however, has been the substantial increase in complexity, including in parts variety, supply locations, fast-changing technology, as well as regulatory and consumer demands.

[sta_anchor id="1"]The growth in the automotive industry in North America has not just represented an increase in volume across the parts supply chain – although, with sales and production expected to rise for an unprecedented seventh consecutive year, there are plenty of capacity issues in tier supplier and logistics capacity. Perhaps even more significant, however, has been the substantial increase in complexity, including in parts variety, supply locations, fast-changing technology, as well as regulatory and consumer demands.

For example, while North America has benefitted from investment in regional production from carmakers and suppliers, logistics executives point to the difficulty of managing supply chains that stretch long distances, whether between the US and Mexico, or global poles of supply. In many cases, vehicles produced across the same platform in multiple plants share components from suppliers in single locations, or because of specialisation in a particular region, such as Japan for microchips.

In this story...

- -Complexity rising

- -Competing on service

- -Production and capacity growth

- -Service parts combinations

- -Hyper network possibilities

- -Open to new possibilities

Wendi Gentry-Stuenkel, head of inbound logistics and automotive transportation at Fiat Chrysler Automobiles US, pointed to the carmaker’s global production growth, including for the Jeep brand – versions of which are now or will soon be built in the US, Mexico, Italy, Brazil and China – and the consequent increase in sharing parts across regions.

“Even in the context of the NAFTA region, managing global parts complexity in the supply base and transport networks is continually a challenge,” she said. “You can see it in the struggles in Japan we are seeing [following the recent earthquake] and the ongoing trade offs in regional plants, all of which need the same parts. And that is before we even get into [other OEM] competition, which are often using the same suppliers.”

Such global flows represent not only high logistics costs and potential risk, but they also require careful management attention, including close collaboration with suppliers and logistics providers. At FCA, Gentry-Stuenkel discussed using a supplier quality survey to assess operational performance at logistics carriers that had, until recently, been used only for parts suppliers.

Paulo Monteiro, inbound logistics manager at Volkswagen Group of America, which has an assembly plant in Chattanooga, Tennessee, also emphasised the necessity of working closely with suppliers and logistics providers further upstream. The carmaker is set to launch production later this year of a new, midsized SUV, which will nearly double the size of Chattanooga and increase the amount of global and regional parts that serve it. Though Volkswagen has a high proportion of its suppliers based within the US, including eight just-in-sequence suppliers in an adjacent supplier park to its plant, the carmaker has made more efforts, together with its tier ones, to track the long supply chains that often precede these suppliers, whether it is trim parts from Mexico, leather from Argentina or electronics from Asia.

“Tier one suppliers are autonomous and we don’t tell them how to run their business. However, it is our responsibility to get involved across the supply chain and help manage lower tier suppliers and logistics providers, where necessary,” he said. “It is risk management for [Volkswagen].”

Regional expansion within North America has also brought its share of complexity to parts and material flows. Mexico’s production boom has already seen vehicle assembly rise by 50% since the start of the decade to 3.4m units last year, and is expected to reach 5m by 2020 as more OEMs and suppliers open or expand plants.

More news and feature stories from the Supply Chain conference in Atlanta, Georgia

- -View video recordings of most sessions

- -Intermodal opportunities for OEMs

- -Recalls are a heavy burden for logistics

- -Only the tech and data you can handle

- -Getting the service parts there ASAP

- -Volkswagen, Audi and Porsche to share LA PDC

- -A supply chain no less global than ever

- -Mexican and intermodal shockwaves

- -Last panel: question time

This expansion has helped manufacturers to meet more demand for the growing US market with shorter lead times and reduced currency exposure. However, higher-than expected production, long internal supply chains over trucking and intermodal routes, along with congestion and potential delays at the US-Mexico border, have led to logistics disruptions and increased risks. The fast growth has also led to struggles in the supply base to recruit and maintain staff, including management and maintenance for logistics, according to Gentry-Stuenkel, all of which can affect flow, inventory strategy and variability in production and distribution.

“All the things that can happen crossing the border can keep you up at night in paranoia,” she said. “When we have these longer supply chains, there is no tolerance for things going wrong.”

Service parts delivery pressure, recalls and consolidation[sta_anchor id="2"]Complexity in the automotive supply chain does not begin and end with inbound logistics. Rising part numbers, changing demand patterns and regulatory pressures have also impacted service parts distribution. Next-day delivery to dealers has become virtually the norm for standard orders of original OEM parts across the US, as carmakers use logistics to compete with independent parts distributors and generic brands.

At the Volkswagen Group of America, for example, Anu Goel, vice-president of parts and vehicle logistics, revealed that Volkswagen and Audi dealers in the US now receive 94% of stock orders placed before the daily cut-off times by 8am the next day. Several years ago, the company’s standard for such orders was 2-4 days (compared to a US industry average of around two days), while dealers relied on emergency orders for overnight delivery.

Today, dealers are actually getting better service on stock orders than they are emergency ones delivered by FedEx, said Goel, since emergency orders typically arrive by around 10.30am. The difference is that emergency orders have a longer cut-off time, at 5pm, compared to 1pm-3pm for stock orders.

“Our stock orders arrive in cages on dedicated dealer services, with fewer damages on average that FedEx,” he said. “Having this next day service allows dealers to stock a wider inventory of parts because they can replenish them faster.”

Other major OEMs, including Ford and Toyota, have equally ambitious replenishment models for dealers. At Toyota dealers, most even have the option for a same day collection for certain parts.

According to Anu Goel, Volkswagen has improved its stock delivery lead time from 2-4 days to overnight delivery in 94% of cases

Over the past half decade or so, carmakers have also seen a significant spike in extended warranty adjustments and recalls across the US and North America, from safety to emission issues, that can cause significant variation in parts purchasing and inventory planning, and which are compounding already tight supplier capacity. Two current high profile recalls, around Takata airbags and the Volkswagen diesel scandal, are both not yet resolved, which points to further supply chain costs and uncertainty.

Helmut Nittmann, global director of parts supply and logistics at the Ford Customer Service Division, which is responsible for service parts across the carmaker (read an interview with its president, Frederiek Toney, here), said that the growth in recalls has had real impacts for logistics. “The inventory that we have to support those recalls is now about four times higher than it was 5-6 years ago,” said Nittmann. “On the plus side, Ford is catching issues a lot earlier, which definitely helps on the total cost.”

However, carmakers have been looking more carefully at ways to leverage production teams, whether in purchasing, manufacturing or distribution. Eduardo Huante, general manager of service parts and accessories supply at Toyota’s North American Parts Organisation (NAPO), pointed to strategies that include working with Toyota’s production team to help suppliers increase their production capacity, as well combining transport where possible. (For more on NAPO's supply chain, read here.)

Such combinations, together with the automotive supply chain’s complicated global and regional flows, beg another question. If manufacturers are already sharing so much of the same technology, the same production and distribution ambitions, the same suppliers and in many instances even the same locations, then why do OEM logistics networks still tend to operate mostly in isolation?

It’s a question that more executives and experts in the supply chain are starting to ask, with some responses and alternatives emerging at the conference both for production and service parts.

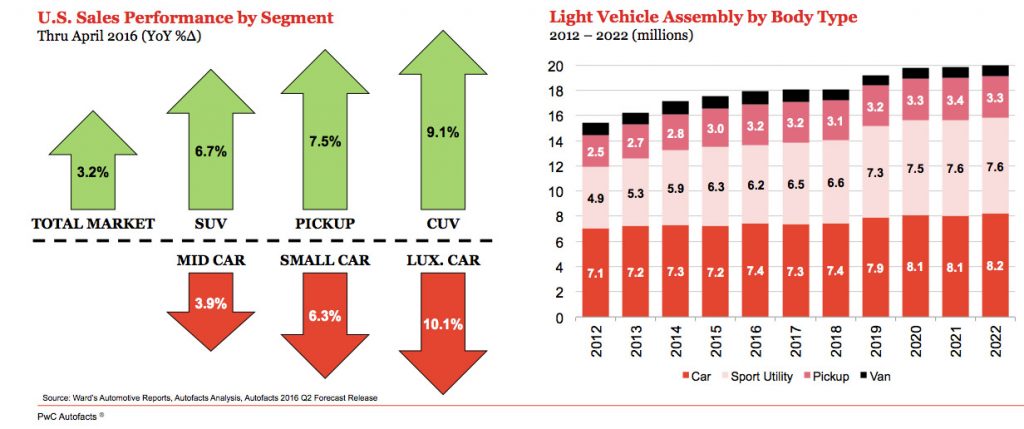

The growth saga continues[sta_anchor id="3"]The North American automotive supply chain has mostly been a story of recovery and increasing prosperity, buoyed by record light vehicle sales in the US in 2015 – and the narrative may still have more positive chapters before it takes a darker turn. Brandon Mason, lead analyst for the Americas at forecasting firm PwC Autofacts, predicted that the US market could see light vehicle sales reach a record 17.8m units this year.

That rise continues to mask significant variances in the market, however. Thanks to the low oil price, SUV, crossover and pickup truck sales continue to surge ahead, even while demand for all classes of sedans, including luxury, midsized and compact cars, is falling.

PwC forecasts that the US is due for a cyclical downturn, and perhaps even a mild recession, which it currently anticipates for 2018. However, the forecasted drop in vehicle sales in such a scenario, at around 4%, is expected to be “mild” according to Mason, and growth should resume fairly quickly – barring a major global economic disturbance.

Even with a sales decline expected at some point in the near future, PwC sees positive growth for North American production. Light vehicle assembly across the US, Canada and Mexico, for example, is forecast to rise from 17.5m units in 2015, to 20m units by 2022. Of that growth, around 1.8m units of expansion are expected in Mexico, while Canada’s vehicle assembly is expected to contract.

US SUV growth to continue (click to expand)

US SUV growth to continue (click to expand)The bulk of expansion in production growth in the US is also expected to be for larger vehicles. Even though the price of oil has risen from below $30 per barrel earlier this year to closer to $50 now, Mason still sees prices remaining at relatively low levels compared to the highs of around $120 just two years ago.

Further volatility in foreign exchange rates, including a 6% rise in the Japanese yen in recent months against the US dollar, is also likely to accelerate investment in North America, added Mason.

Growth across the supply chain since the financial crisis has led to some consistent strains in capacity, particular for tier suppliers and certain logistics providers who have struggled to keep up. Italian tyre manufacturer Pirelli, for example, is rapidly expanding production at its plant in Silao, in central Mexico, to serve North America, its fastest growing global market. Tyre output at the plant, which opened in 2012, rose to 2.7m units last year, is planned to reach 4.7m units by 2017 and jump to 7.5m by 2018, according to John Godfrey, vice-president of NAFTA logistics.

Around 70% of that volume is expected to be exported to the US and Canada. Already, Pirelli faces logistics and border difficulties, including complexities in changing border equipment, risks to just-in-time production and driver shortages.

While these issues would be helped by using intermodal transport, tyre demand has been so high that Pirelli has struggled to use the mode as much as Godfrey would like. Congestion and visibility issues around interchanges in Chicago have made intermodal more difficult.

“We started with intermodal, and that is my goal, but we are now shipping 80% by truck into US,” said Godfrey. “We are trying to reverse this trend.”

Supplier capacity has also caused issues for service parts logistics. NAPO’s Eduardo Huante said that high production and sales rate in the US was putting strains on the carmaker’s suppliers. For example, some suppliers had built more factories in rural areas to achieve lower costs, however they were now struggling to keep up with demand, particularly in areas where unemployment has fallen as low as 2%. “Some of our suppliers who moved to these rural areas for good economic reasons now cannot get enough workers in to produce enough of our parts,” he said.

Huante and Gentry-Stuenkel pointed to weather events that have also hurt the supply chain. They both highlighted the earthquake in Japan earlier this year that disrupted component supply, including microchips, while Huante also pointed to extreme rain and hail this spring that has damaged vehicles, as well as a storm that even shut down Toyota’s plant in San Antonio, Texas.

"As the industry recovered we were having a hard time keeping up with suppliers, and even though the ideal transit would have been rail and intermodal, I just couldn’t get to those modes because I didn’t have the supply of parts" - Wendi Gentry-Stuenkel, FCA US

"As the industry recovered we were having a hard time keeping up with suppliers, and even though the ideal transit would have been rail and intermodal, I just couldn’t get to those modes because I didn’t have the supply of parts" - Wendi Gentry-Stuenkel, FCA US

However, with a measure stability now expected in production and demand, manufacturers are anticipating opportunities to improve logistics flows.

Wendi Gentry-Stuenkel, for example, pointed to assembly volume that was consistently above forecasts in recent years, during which time railways in particular faced capacity shortages, leading to transport deviations. For example, in 2014 – a year in which railways were hit by bad weather and a spike in demand for energy commodities – FCA’s proportion of rail and intermodal transport for inbound material declined from 40% of transport miles to 39% (a drop that resulted in a rise in trucking of nearly 55m miles).

“As the industry recovered we were having a hard time keeping up with suppliers, and even though the ideal transit would have been rail and intermodal, I just couldn’t get to those modes because I didn’t have the supply of parts,” she said.

In 2015, however, rail modes started to recover thanks to some further consistency in production, as well as more service capacity following declines in the energy sector. FCA’s use of rail and intermodal recovered to 44% last year, and is expected to be “substantially higher” this year.

“Now we are finally getting to the point where we can better match our preferred transport mode because of the levelling out of volumes and better service [on the railways],” she said.

Sharing is caring for service parts[sta_anchor id="4"]On the service parts side, carmakers have dealt with capacity issues in some instances by getting closer to counterparts in production parts logistics, with strategies that include combined efforts in purchasing, working with suppliers to increase production capacity, and even sharing logistics flows.

It’s an approach that Ford has taken for several years, both to increase transport efficiency, but also to deal with supplier shortages. Helmut Nittmann said that the service parts team worked closely with its production team – whose parts demand is often 5-6 times higher – to use their influence in increasing supplier output, especially for volume spikes and safety recalls. “We will actually talk about taking production down to meet service requirements,” he said. “We'll pull schedules ahead. That is a big benefit, especially with in-house suppliers.”

Nittmann also pointed to benefits both in parts purchasing and planning, as well as in logistics. “The key thing is to run milkruns from sub-suppliers to distribution centres,” he said.

At Toyota this combination is even newer, and has started to come together over the past 18 months. “We are going slow with our consolidation with inbound logistics, but we are making in progress,” said Ed Huante. “We have taken some full truckloads [from suppliers] and have basically handed them over from the service parts side to our manufacturing counterparts at Toyota and said, ‘Through your purchasing, manufacturing and logistics planning, please maintain all the inbound [transport] for North America’.”

Toyota's Ed Huante and Ford's Helmut Nittmann said service parts could benefit from combinations in purchasing and logistics with production parts

Toyota's Ed Huante and Ford's Helmut Nittmann said service parts could benefit from combinations in purchasing and logistics with production partsSoon, Toyota will also be integrating milkruns between service and production parts as well, although this will require changes mainly on the service parts side, said Huante. For example, the service parts team has had to do more advanced supplier planning for six months up to three years in advance, which he admitted was “not perfect” for service parts demand.

Furthermore, service parts packaging engineers have had to change its packaging approach to combine with production parts, since for inbound the milkrun routing is adjusted around ten times per year. “So based on the size of the position [the production parts team] is going to give service parts, we need to redesign our master packs about ten times a year as well,” he said.

Towards a 'hyper-connected' supply chain[sta_anchor id="5"]Collaboration in moving parts, including in freight consolidation, was a major topic at the conference, whether in combining service and inbound parts, sharing expertise and resources with suppliers, or in improving the routing and tracking of returnable packaging.

Tier supplier Magna International, for example, is making a concerted effort for the first time to plan and coordinate its packaging assets across various plants, including through the use of crossdocks to ensure containers do not move empty over long distances. According to Bridget Grewal, packaging continuous improvement manager, the supplier expects to save around $25m in reducing empty transport and packaging waste.

Packaging providers, including Surgere and Chep, also reported growing interest and activities around sharing and tracking returnable containers. William Wappler, president of Surgere, a returnable packaging management provider that uses RFID to monitor containers, said that, over the past year, Surgere had started projects or trials with four OEMs and eight tier suppliers.

Some carmakers continue to make progress in finding ways to better combine freight within their own networks, or of those across different plants and legal entities across North America. The Volkswagen Group, for example, is moving towards a more integrated supply chain network across its operations in the US, and its three plants in Mexico, including Audi’s factory set to open later this year, according to Paulo Monteiro.

On the service parts side, meanwhile, a new regional parts centre in northern California has helped to free up space in Volkswagen’s existing warehouse near Los Angeles. This year, for the first time, fellow group member Porsche will lease part of the warehouse from Volkswagen Group of America, helping not only to share physical space but also distribution. “Around 20% of Audi and Porsche dealers are shared,” said Anu Goel.

In at least some instances, OEM executives revealed projects in which they were also sharing freight or warehouses with other brands. Kevin Wade, senior staff administrator for the transportation department at Honda of America, noted increased collaboration with other OEMs and tier suppliers.

“We have found that sharing crossdocks with others has been the most economical way to support a lot of our lanes,” he said. “We now have more shared and common lanes.” (Read more about Honda sharing crossdocks with other OEMs here.)

In Benoit Montreuil's 'hyperconnected' automotive supply chain, carmakers and suppliers would share a dense network of crossdock and consolidation hubs (click to expand)

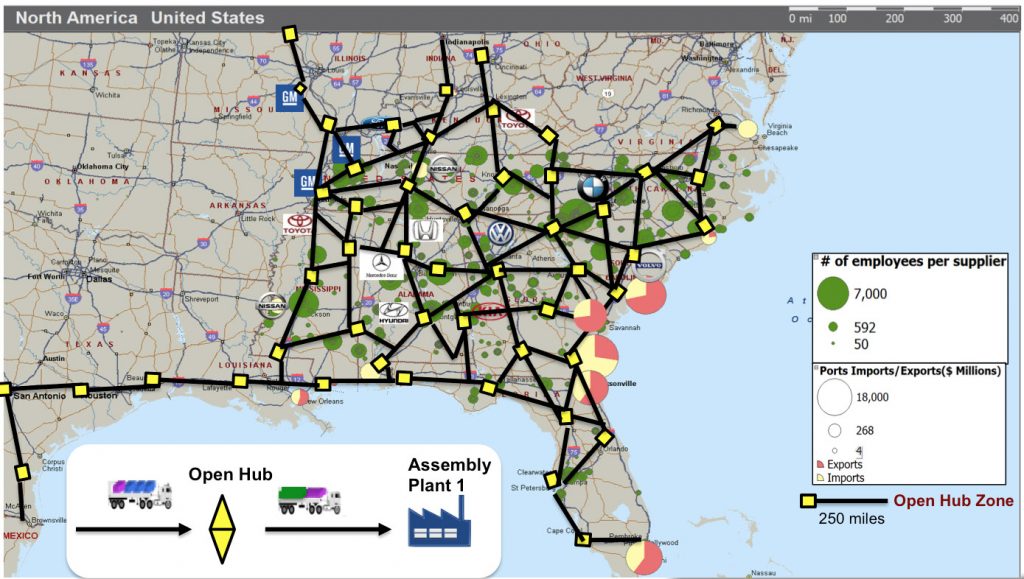

In Benoit Montreuil's 'hyperconnected' automotive supply chain, carmakers and suppliers would share a dense network of crossdock and consolidation hubs (click to expand)However, most executives admitted that such sharing remained relatively rare. An alternative, radical new vision of the supply chain was offered by Dr Benoit Montreuil, leader of the Supply Chain and Logistics Institute at the Georgia Institute of Technology.

Montreuil is one of the leading researchers on the ‘physical internet’ and what it could mean for transport and logistics. He suggested a radical transformation of the automotive supply chain in which logistics networks were completely open and shared between companies, packaging was standard and highly modular, and in which parts and material moved through shared consolidation hubs. Information would be tracked through connected vehicles and logistics equipment in real time.

“We foresee improving logistics by an order of magnitude, and making it faster and greener,” he said. “This would be a hyper-connected global logistics system enabling seamless open asset sharing and flow consolidation through standardised encapsulations of goods – including modularisation, protocols and interfaces.”

According to Montreuil, an internet of things for logistics, whereby trucks, packaging and locations could automatically sense and communicate with each other, would help eliminate many inefficiencies inherent in the freight network, particularly by allowing material to move through almost any logistics channel. Empty trucks could be avoided, while material would no longer have to sit for long periods awaiting a full delivery load, since material could be pooled faster. IT systems would have open, common protocols, while packaging and containers could be adjusted for almost any equipment.

In Montreuil’s 'hyper-connected network', multiple suppliers would move freight through a series of shared, multimodal consolidation hubs to ensure transport equipment was full in both directions. And thanks to the modular equipment a truck or train moving into an intermodal centre would be able to transfer material to other equipment in a matter of minutes rather the hours, or even days, it currently takes.

"If you look at the South, we have many suppliers and carmakers in the vicinity, and with the supply base around it, it looks good as a network – but it is entirely disconnected. Suppliers might be the same for Mercedes-Benz or BMW, but they are separate." - Dr Benoit Montreuil, Georgia Tech

"If you look at the South, we have many suppliers and carmakers in the vicinity, and with the supply base around it, it looks good as a network – but it is entirely disconnected. Suppliers might be the same for Mercedes-Benz or BMW, but they are separate." - Dr Benoit Montreuil, Georgia Tech

Montreuil pointed to a map of the automotive supply chain in North America to demonstrate the possibilities of such a network – as well as how far the current reality is from his vision. OEM plants are located in relatively close proximity across numerous regions, whether in the Midwest, the South, or parts of Mexico, while suppliers are bunched in dense, overlapping clusters within the vicinity of plants. Much of these hubs stretch along the US Interstate highway network, as well as major railways and airports.

However, while the supply chain has a clear and connected geography, most of it operates independently for logistics. Suppliers might be shared, but logistics networks tend to be organised into dedicated storage and fulfilment operations. While there is some degree of sharing and consolidation – particularly across an OEM’s different plants – links across carmakers or other industries make up a small proportion of freight.

“If you look at the South, we have many suppliers and carmakers in the vicinity, and with the supply base around it, it looks good as a network – but it is entirely disconnected,” Montreuil said. “Suppliers might be the same for Mercedes-Benz or BMW, but they are separate. There is much opportunity for better asset sharing and [freight] consolidation across the industry.”

A fully connected network, supported by constant tracking and cloud-based visibility and control, could reduce costs by as much as 33% and substantially cut lead times, he estimated.

In an even more advanced version, manufacturers could go a step further and even share assembly and parts-making factories, although Montreuil admitted that this would be difficult to achieve.

Far off but not so far away[sta_anchor id="6"]While the shared logistics network would be a big jump from today’s level of logistics consolidation, many at the conference thought Montreuil’s idea of a hyper-connected network made sense to at least some degree. FCA’s Wendi Gentry-Stuenkel agreed that while carmakers were often using the same suppliers and in many cases even the same supplier locations to serve assembly plants, most OEM networks remained dedicated and disconnected. For example, only a small amount of FCA’s logistics network is shared in anyway with other carmakers.

“FCA is going into the very same suppliers that many of my competitors are. Can we consolidate our freight? Yes,” she said. “We are already doing some of that. But the next horizon is actively managing the relationship.”

Montreuil and others at the event admitted that some aspects of the connected network were happening either within OEMs or between brands. For example, the idea of a container pool itself is something of a model for the hyper-connected network on a smaller scale, including the use of shared crossdocks to bring together standardised packaging and avoid long empty transport routes. Chris Buchanan, sales director for pooling provider Chep, compared such a network to an “Uber of logistics”, allowing manufacturers to share equipment and to move containers on a shorter transport routes for replacement.

Integrated providers, such as Ryder, also supported the concept, and indicated that they were already carrying out aspects of it in their third party logistics network. Juan Calvillo, director of supply chain excellence for Ryder Mexico, said that much of the provider’s services in Mexico already move through multi-client facilities, including both for automotive and other industries. For the automotive industry, specifically, the company has developed a spare parts distribution network that combines different OEMs on the same truck.

Montreuil also pointed to trials of the concept outside the industry, including for several supermarket chains in France. He also suggested that Amazon, which is increasingly opening up its network and fulfilment centres for other retailers to share its distribution channels, could lead the way. “If those guys [at Amazon] decide to make a change like this, many will follow,” he said.

Ford's Nittmann thought that service parts was an area that could benefit in particular from more freight sharing across brands

Ford's Nittmann thought that service parts was an area that could benefit in particular from more freight sharing across brandsIn automotive and across the wider logistics industry, however, much of the concept remains limited or untested. Montreuil and others pointed to cultural barriers to change as the biggest obstacle to moving towards a more shared network. Speakers at the event noted the difficulties involved, not least the pressures of meeting strict, just-in-time delivery schedules, and the risk of that shared transport might pose to shutting down another OEM’s plant should their be a disruption in transport.

Ryder’s Calvillo agreed that the industry lacked a clear method of bringing together different manufacturers to agree such collaboration. “I see willingness among some, but not in a robust process as it should be to leverage all the potential savings and improvements as well. It is hard to get them on board,” he said.

FCA’s Gentry-Stuenkel also thought OEMs needed to be more engaged in such sharing and collaboration. “If we want to get to the next level it requires a lot more collaboration on a continual basis, on a weekly basis, not just annually,” she said. “And that is where efficiencies will come from.”

The good news was that most executives said that they were open to such collaboration. A live voting session of delegates found that 70% believed such a network would have important benefits for both production and service parts logistics, while only 19% thought it would not be relevant.

At Ford, Helmut Nittmann supported the idea of a more common, shared network, perhaps especially for service parts. “I really like the idea of a hyper-connected network on the service side, where OEMs could use that ability to collect especially those smaller shipments and bring them back to respective service organisations,” he said.

Gentry-Stuenkel added that logistics and material availability at suppliers was not what she considered to be a competitive area between carmakers, and that ways of more sharing should be explored.

“Except for those who are contiguous to one of our plants, our tier suppliers are usually supporting many of my competitors,” she said. “We are all fighting for the best resources at each of them, while those tier one material managers are trying to satisfy customers who are not always aligned in standardised processes. That is a key opportunity.

“Open consolidation is how we will make progress,” she said. “It is about relationships and being open to help the efficiency of our suppliers.”

The inaugural Automotive Logistics Supply Chain Conference is part of the global Automotive Logistics series of conferences.

The next conference in the series is Finished Vehicle Logistics North America on June 7-9th in Newport Beach, California.

The next conference in Europe will be Automotive Logistics Russia in Moscow on June 28-29th.