Production and sales forecasts

Europe's OEMs face pressure as Chinese carmakers drive global growth, S&P Global data shows

At Automotive Logistics and Supply Chain Europe 2026, S&P Global Mobility's Tatiana Hristov shared insight into how vehicle production and sales in Europe compares with the rest of the world. While shifting tariff and trade policies have impacted volumes around the world, Chinese OEMs saw significant growth in light vehicle production volume from 2024 to 2025 and their global expansion is set to continue over the next decade.

S&P Global Mobility's Tatiana Hristov shared data and forecasts surrounding European vehicle production and sales at ALSC Europe 2026

ALSC Europe 2026

Speaking on stage at the conference, Tatiana Hristov, director of EMEA light vehicles sales forecast at S&P Global Mobility, highlighted that while the automotive industry is facing a vast number of different challenges in 2026, not all of them are new. Affordability issues, for example, have been present as a concern in the industry for at least the past four years, and the impact of tariff uncertainty has been very visible since the beginning of 2025.

Challenges and opportunities in today's global automotive market

Hristov identified a number of challenges and opportunities that within the automotive supply chain industry today. These included:

According to S&P data, global light vehicle production volumes increased from 89.6 million units in 2024 to 93.1 million in 2025 – a year-on-year increase of 3.9%. "Considering how many challenges we already had last year, the result of the production from last year of nearly plus 4% is actually a very good result," Hristov commented.

However, growth in mature markets in 2025 was very limited. Volumes declined slightly in North America, Europe and South Korea, while a slight increase was reported in Japan – on average, production volumes in mature markets dipped by 0.5% in 2025. The overall growth, then, was driven predominantly be emerging markets such as mainland China (+10.2%), South Asia (+5.3%) and the rest of the world (+1.6%).

Hristov made reference to the fact that in most metrics, Chinese brands are overperforming while more mature markets are underperforming. "That's the reality right now," she said.

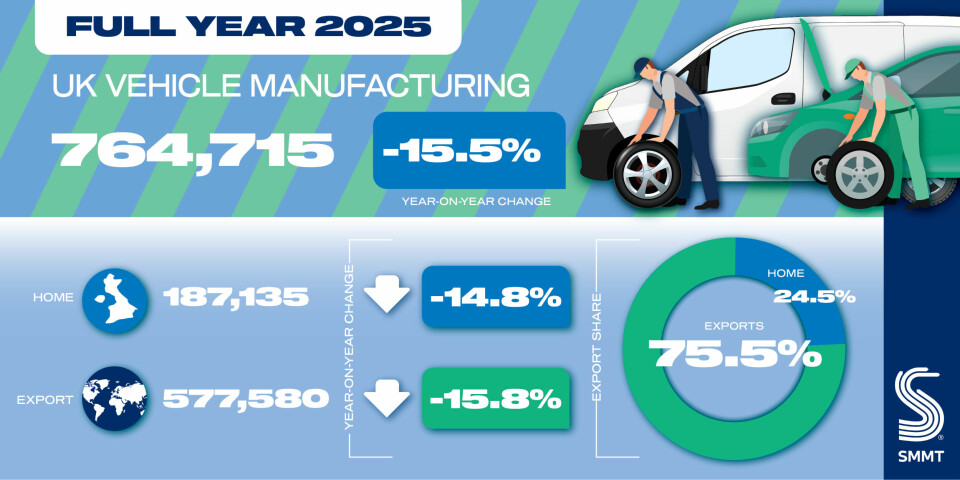

In Europe's case, she noted that the market was constrained in 2025 by compliance with EU regulation – specifically the requirement to reduce the CO2 emissions of fleets by 15% (compared to a 2021 baseline), which was relaxed in May 2025 to enable manufacturers to average their performance over a three-year period (2025-2027).

With constraints such as these, Hristov shared her view that a decline in European light vehicle production of 0.7% from 2024 to 2025 could've been much worse.

Legacy OEMs' growth stagnates while China's 'Big Six' prosper

One particularly interesting observation Hristov made during her presentation was that of the legacy OEMs, only Toyota saw significant growth in light vehicle production volume from 2024 to 2025, and this was driven by "underperformance the year before, relatively weak yen last year, but also very high demand for HEVs from Toyota – which are very successful in different parts of the world". All other legacy OEMs saw growth plateau or decline in the past year.

On the other hand, each of the 'Big SIx' OEMs from China demonstrated significant growth during this period: Geely (+29.4%), Chery (+24.0%), SGMW (+22.6%) Great Wall, (+10.6%), Changan (+6.4%) and BYD (5.0%). From 2026 to 2033, S&P forecasts the biggest growth in vehicle production volume to come from BYD (+41.1%) and Great Wall (+31.4%) as well as other Chinese OEMs outside the so-called 'Big Six' (+46.8%).

These emerging OEMs – the likes of Leapmotor, Li Auto, Huawei, NIO, Xaiomi and Xpeng – are expected to increase their share of light vehicle production in mainland China over the next few years as the share held by foreign OEMs gradually decreases.

Amid the growing trend of protectionism in geopolitics, OEMs in China have begun to explore overseas production alongside their export strategies. Until 2023, global light vehicle imports from mainland China had been below 2 million. In 2026, more than 4 million light vehicles had been imported from mainland China around the world, with Europe alone having imported more than 1.5 million. By 2033, S&P forecasts that 2.2 million vehicles will enter Europe from China annually.

And with Chinese brands introducing almost double the number of models to the market compared with European brands, China poses a real threat to the competitiveness of legacy OEMs and the European automotive manufacturing sector.

S&P Global Mobility's 'Six Ps' approach to improving cost efficiciency

When facing a multitude of headwinds – from the impacts of the Iran war to tariff fluctuations – Hristov outlined six key areas where OEMs, particularly legacy OEMs, can find cost efficiency improvements:

- People (optimisation of workforce and processes; possible HR cuts to streamline operations)

- Processes (optimisation of operations and workflows to improve efficiency and reduce costs)

- PSD (moving away from single-focus propulsion system designs – adoption of multi-energy/platform strategies so one platform can support a range of powertrains)

- Parts / Procurement (where and how expensive to source parts; local content requirements and sourcing strategy to meet regulation and cost targets)

- Product (right‑sizing and adapting the right product for the right segment/market)

- Plant (localisation and plant-utilisation optimisation — addressing overcapacity, adapting production for local demand and plant consolidation)