Limited inventory because of production shortfalls combined with strong retail demand are driving up sales prices both for new and used vehicles in the US, according to the National Automobile Dealers Association (Nada).

Nissan working with Georgia Tech on improving vehicle deliveries and truck driver routes

The US currently has the lowest vehicle inventory on the ground since 2011, with an average of 25 days of supply in the month of May, compared to 61 days in the same month last year. There continues to be strong demand in the wake of the Covid lockdown, with the seasonally adjusted annual rate of sales at 18.8m in April, one of the highest rates over the last two decades.

However, vehicle production in the US is down as a consequence of the semiconductor supply shortage, which comes on top of production shortfalls last year because of Covid-19-related shutdowns.

That shortfall has hit Ford, GM and Stellantis the hardest and dealers cannot sell enough of the popular models they make, such as the crossovers (CUVs), SUVs and pickup trucks.

“Dealers like to carry a lot of these because customers are looking for very specific options and they can provide them. Unfortunately, this is not the case – pickups are being sold before they get to the lot,” said Manzi. “You want to have some inventory available to show your repeat customers and its tough when all you offer is a sold order.”

It was a similar situation for Toyota, according to Brion Stapp, dealer principal at Stapp Interstate Toyota.

“We have transport trucks coming multiple times per week but 41% of our entire pipeline for the next three months is presold,” he said. “As those trucks roll in on a daily basis we unload them and put them right into the sold inventory for our customers to take delivery.”

What dealers really want is better visibility on what is coming down the pipeline from the assembly plants, something that the outbound logistics sector could help with.

“The more information you can provide to these dealers the better, and the sooner the better,” said Manzi. “They are tired of hearing about delays and that a pickup truck is sitting in the lot waiting for a microchip. Anything that can provide certainty about when they are going to get the product will help and is going to be key and help the relationship [with the customer].

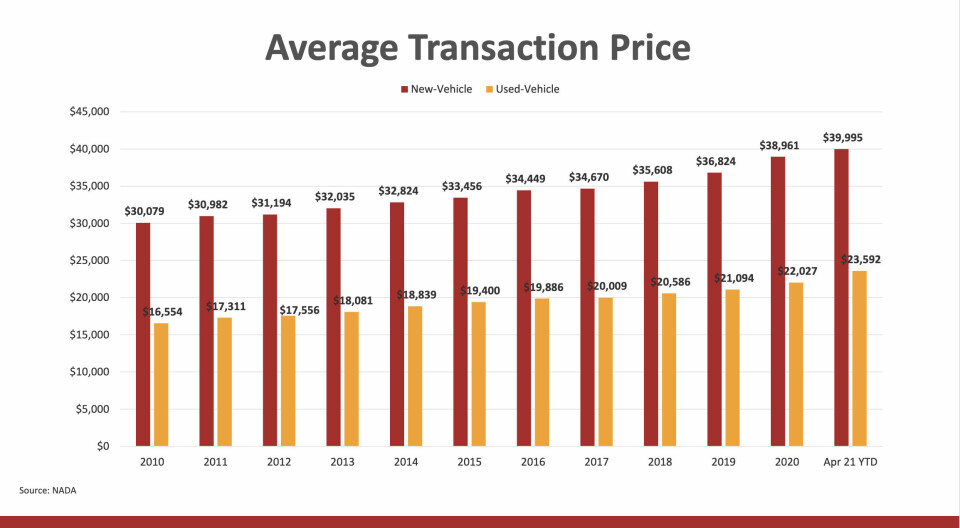

Average transaction price in US

Pressure on pricing Currently, pickups, CUVs and SUVs account for around 77% of vehicle sales against 23% for sedans. The CUV segment in particular accounts for around 46% of sales in the US and customers are now having to compromise on options, such as colour and trim, because of the shortfall in availability. This is also hampered by the reduction of vehicle allocation from months to weeks.

“Toyota would allocate vehicles three months in advance and with that we can make changes, like colour or other options for the customer, but that is now down to six to seven weeks before being allocated,” said Stapp. “The pipeline looks different and we have lost the chance to change the detail of the order.”

Dealer sales are at risk when customers do not find the car they want to buy, though carmakers have done well in reallocating production to make sure the more profitable and popular models are getting through to end-customers. Stapp said, despite the high turnover and shorter allocation period, Toyota ensured there was a clear line of communication to dealer on what was being allocated, helping to make good on promises to the end-customer.

Advertisement

Nevertheless, this pressure on inventory has pushed up the average transaction price on a new car in the US. In April this year that figure was just short of $40,000 for a new car and around $23,600 for a second-hand one, respectively increases of 2.5% and 6.6% on last year (see table).

At the same time sales incentives are much lower than average. In May this year, figures from analyst JD Power indicated the average incentive price per unit was around $2,800, having dropped around $2,000 compared to the same month in 2020 (when it was nearer $5,000). Given the strong incentives that were put in place following the closures caused by the Covid pandemic, including 0% interest over 84 months, that is little surprise, but even in May 2019 the average incentive was nearer $4,000.

There is some consolation, according to Nada in that interest rates on financing are currently low and consumers have better equity at the moment. There has also been an uptick in the average loan level.

Fleet and remarketing Fleet sales remain depressed by comparison, in part because carmakers are going the extra mile to allocate production to retail customers. Resurgent demand from the rental sector is not being met and deliveries are running late.

“Fleet sales have been consistent at 3m units [2019: 3.3m] and between 17% and 19% of sales in any given year, according to Manzi. However, last year that figure dropped to 2.1m because of cancellations from rental car fleets during the Covid lockdown. Manzi estimated fleet sales to hit 2.5m this year, with a full recovery delayed because of the semiconductor shortage.

As a consequence, rental companies are having to rely more heavily on the used car market, while at the same time dealers hang on to vehicles back rather than remarketing them.

“A lot of vehicles that would have been flowing back to the auctions have not been this past year [and] most dealers taking back lease returns are grounding them to retail on their lots.”

That in turn has pushed up the average used car price.

Advertisement

“It is tough to buy vehicles at auction and you are paying a higher price at wholesale,” noted Manzi. He said higher pricing on used vehicles is expected to continue for the next 18 months and will plateau at a higher level than previously. However, one potentially positive outcome of that is that new vehicle leases become more attractive by comparison.

Looking ahead Manzi forecast that inventory levels and pricing will begin to balance out, with June the last month for record low inventory and high retail prices. He said that production would gradually pick up to meet demand once sufficient supply of semiconductors returned through the second half of the year.

“I’m not sure we will necessarily build it all back up within this year but the sooner they can get producing at full capacity, the better,” he said, estimating that production would return to 16.3m next year.