Carmakers spread the cost of tariffs but prices set to rise say analysts

Marcus WilliamsMarcusWilliams

PublishedModified

5 min

S&P Global Mobility's Mike Wall spoke about the impact of US tariffs at Automotive Logistics and Supply Chain Global

The automotive sector is facing significant cost pressure caused by continuing inflation, high capital and labour costs, a situation exacerbated by the higher tariff costs and associated disruption caused by current US trade policy.

Analysts at this year’s Automotive Logistics and Supply Chain Global conference in Michigan revealed that for the time being costs are being absorbed by OEMs through a range of mitigating strategies as they wait and see how the tariff debacle will play out. That can, however, only be for the short term and there may be additional costs down the line as carmakers look at reshoring supply.

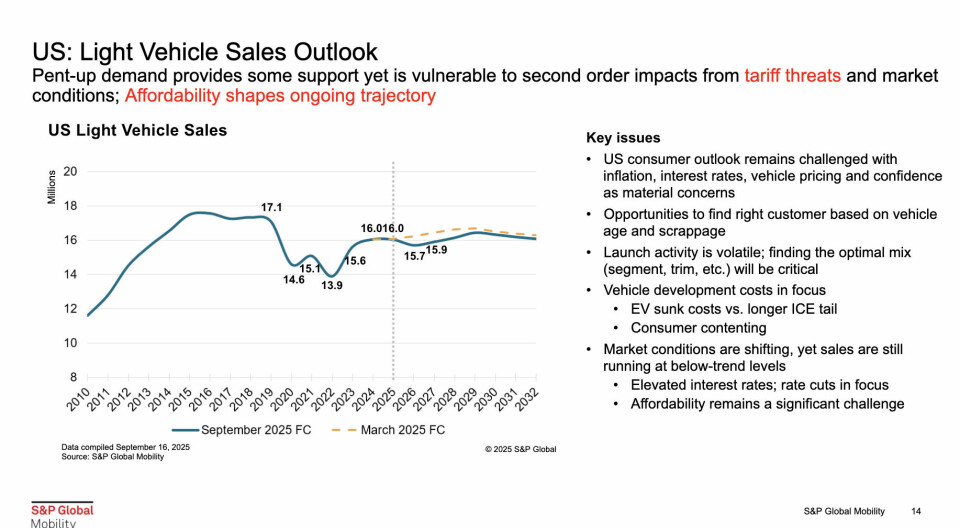

US light vehicle sales outlookS&P Global Mobility

According to figures from market analyst firm S&P Global Mobility, US vehicle sales are currently forecast at around 16m for the year. Light vehicle production is expected to reach 15.2m, down on 2024 and that figure is expected to fall again to 14.7m in 2026 partly because of a projected pullback in US sales.

Mike Wall, executive director of automotive analysis at S&P, said US sales have remained resilient up to now despite the tariff turmoil defining trade with the US this year. Wall said that carmakers are absorbing the increased cost of the tariffs rather than passing them directly to consumers through a number of pricing and cost-containment strategies. They include spreading costs across markets and corporate cost centres, not solely focusing on the US market.

Advertisement

“You've got an automaker that is maybe selling in South Asia and in North America, and maybe in just the broader Asian market or Europe,” noted Wall. “They're adjusting pricing globally and they're not focusing specifically or universally on the US; that's a big deal.”

OEMs are also realigning model mixes to mask price changes and protect margins. That includes moving standard features to optional, adjusting trim and mix, including de-contenting in some cases. It also includes making component material changes, such as sacrificing fuel economy for lower cost but heavier parts made of steel rather than aluminium. It also includes reallocating funds previously spent on corporate average fuel economy (Cafe) penalties or regulatory credits. Wall also pointed to reducing logistics costs where easy raw material sourcing alternatives are available.

Wall said that import-heavy brands experience more price activity, but it is not derailing the overall market.

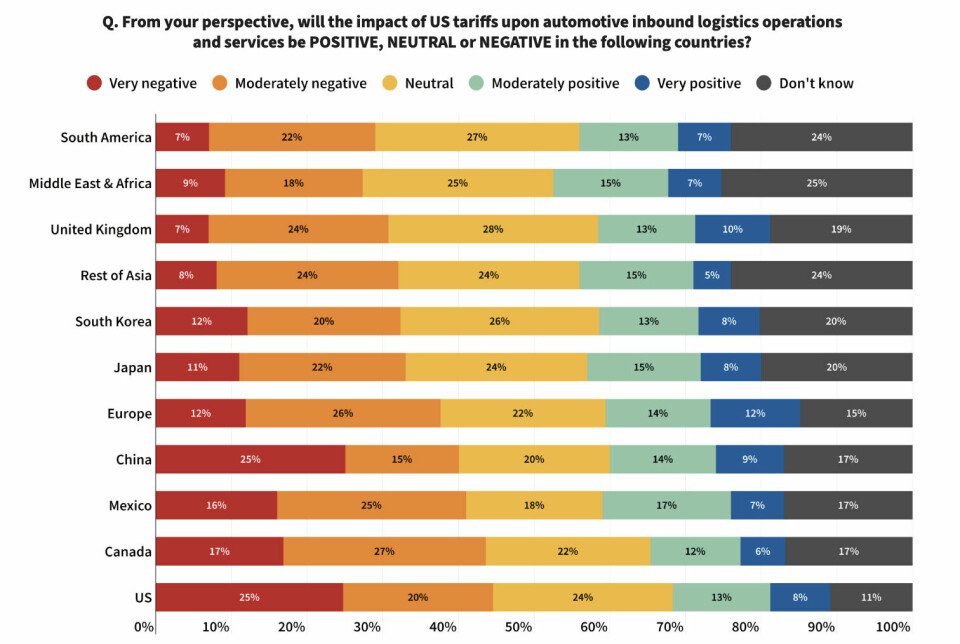

Impact of US tariffs on inbound logistics per country"Automotive Inbound Logistics Survey 2025", Automotive Logistics

However, in a recent survey on inbound automotive logistics carried out by DP World in partnership with Automotive Logistics, vehicle price rises are expected by the end of 2025 because of Trump’s tariff strategy. The Automotive Inbound Logistics Survey 2025 reveals that tariffs are contributing to uncertainty and supply chain disruption, and the majority of global respondents believed that the tariffs will have a more negative than positive impact, with those based in North America expressing the most negative opinion.

Trade wars, tariffs and the associated uncertainty were the second most significant problem that respondents to the survey noted, accounting as a concern for 37% of those responding to the survey globally. Many businesses are still coming to terms with the long-term impact of the US tariffs that the Trump administration brought in this past April and those reciprocal tariffs taken by a number of trading nations around the world.

Carmakers and suppliers are largely taking a ‘wait and see’ approach so far, according to the survey results, while others look at diversifying sourcing and developing new trade routes.

“This survey was conducted in June-July 2025 and I don’t think the tariff situation and the uncertainty around it has significantly changed since then,” said the report’s author, Daniel Harrison, automotive analyst at Ultima Media. “There is a potential Supreme Court ruling on the tariffs, but I don't think that's going to change the trajectory of the tariffs.” Harrison acknowledged that the ‘wait and see’ approach and the tactics for absorbing the cost cannot last forever. “Major investments and more structural changes will have to come down the line, such as, reshoring and near shoring production to get around those tariff pressures,” said Harrison.

One important relief is in relations between the US and its North American neighbours Mexico and Canada, thanks to the existing trade agreement between them – USMCA.

Advertisement

The USMCA is due to be reviewed next year and the expectation is that tariff-reducing concessions could be made during negotiations. For Canada and Mexico, USMCA-qualifying automotive parts are exempt from tariffs temporarily, while vehicles that are USMCA-compliant are currently tariffed at 25%. Cars built in the US and Mexico can claim back the value of US-sourced parts.

“This is what we feel has been a big support to vehicle sales and production – the fact that USMCA-compliant parts are currently exempt from tariffs,” said Mike Wall. “That's a big deal and extremely consequential. It would have been a much worse position were those to be tariffs sort of writ large. That's not the case.”

Wall said automotive companies are looking for a step down on the tariffs that are still affecting Canada and Mexico and gauging when that is likely to occur.

Another important concern for US carmakers and suppliers is production capacity utilisation. “North America is at about 68% and that's a challenge,” said Wall. “It's a challenge for us here, we really ideally want to see that at 75-80% or better. It is a challenge because we've had a lot of capacity, we've got a lot of battery, electric, vehicle capacity. That's a challenge to kind of maximise that utilisation right now.”

Slow take-up and uncertainty with regard to battery electric vehicles (BEVs) are turning into programme delays, cancellations and weaker launch curves. Wall said that dealers have been working frantically to offload BEVs because the incentives used to sell them ended at the close of September this year.

The short-term outlook for the US is that OEMs are prioritising production and US sourcing is not expected to yield much result until 2027/2028.

A related concern revealed in the Automotive Inbound Logistics Survey is that geopolitical and trade tensions could impact the supply of critical materials, such as rare earth metals, and these could impact inventory levels and disrupt logistics flows, leading to the sort of supply chain instability the automotive industry was hit with during and after the Covid pandemic.

Despite the short-term uncertainty, however, the survey revealed an encouraging level of business confidence in automotive logistics. While pessimistic for the rest of 2025, the response of those surveyed was more positive over the next three years.

“I think that's encouraging in this period of intense uncertainty, there's optimism that things will work out one way or another and the future will be around growth,” said Harrison.

Harrison said one very clear recommendation for automotive sector coming out of the findings of the report is to accelerate digital transformation. “If you're not already on that journey, we would encourage you to go even further because there are clear benefits,” said Harrison, “benefits we talk about a lot in this conference around efficiency, visibility, cost reduction and resilience”.

Another key recommendation for business is to enhance planning and optimisation, which is interlinked with digitalisation, network design and the identification of where efficiency can be improved and resiliency strengthened. Harrison said a third priority for industry is to foster collaborative partnerships. “We hear a lot about cooperation and collaboration, whatever form the partnership takes... [it is] a very critical strategy, especially when you're talking about an automotive logistics industry which is highly fragmented.”

Less-than-truckload optimisation

The results of the Automotive Inbound Logistics Survey 2025 revealed that there were three main interconnected problems facing the automotive industry and most significant, cited as a primary problem by 41% of respondents, was the cost pressure caused by continuing inflation, high capital and labour costs. Shippers are looking at a range of opportunities to manage and offset those costs.

Carrier pricing provider AFMS offers one way of doing so. The company specialises in contract benchmarking, negotiation and invoice auditing across the US, Europe, and Canada, and works with major automotive companies such as Honda, Nissan, Stellantis and John Deere. Mike Erickson, CEO of AFMS held a workshop on rate disruptions, cost impact and the mitigation strategies available to automotive shippers.

Using data analysis of the less-than-truckload (LTL) market, AFMS is able to evaluate the number of LTL carriers a shipper uses and their network coverage relative to warehouse locations. Data includes shipper origin, destination of parts and consignment weight, as well as negotiation history. It also looks at operating ratios to understand carrier profitability for specific routes, taking into consideration costs associated with line hauls, break-bulk transfer and handling units.

Erickson outlined AFMS’ two-phase approach to improving an OEM’s carrier contracts.

In the first phase the company analyses up to three months of a carrier’s shipping invoices and service agreements and benchmarks carrier rates, discounts and shipping characteristics against the market. Using that market intelligence and carrier pricing information it can help OEM customers lower shipping costs. It also provides detailed savings projection reports and ‘what-if’ scenario modelling analysis along with a carrier network review.

AFMS also prepares carrier negotiation documents and strategies to obtain new pricing targets. These documents are supported with data analytics, pricing analysis and industry benchmarking that supports a new pricing request.

AFMS can additionally review new carrier pricing proposals along with terms and conditions, ensuring any new proposal is acceptable to the OEM.

In its second phase service optimisation analysis it aims to establish best practices within global LTL networks, including mode of transport, comparing ground or airfreight options, and creating routing guidelines by country or region. It also provides clilents with ongoing reporting and management tools for the LTL distribution network using smart shipping reports.