Russia conference: learning to grin and bear it

The Russian market has fallen to its lowest level since the global economic crisis, and manufacturers and logistics providers may face a long road to recovery. However, more than 150 delegates at the Automotive Logistics Russia conference made it clear that they remain committed to the market. Christopher Ludwig and Marcus Williams report from Moscow

The Russian market has fallen to its lowest level since the global economic crisis, and manufacturers and logistics providers may face a long road to recovery. However, more than 150 delegates at the Automotive Logistics Russia conference made it clear that they remain committed to the market. Christopher Ludwig and Marcus Williams report from Moscow

Not much can be said to prettify the current situation in Russia’s automotive industry. The economy is straining under the pressure of a weak rouble, low oil prices, high inflation and tight credit. Added to this, there is no end in sight to the conflict in Ukraine and the resulting economic sanctions from the European Union and the US. Overall the country is experiencing a deep recession. Vehicle sales are dropping fast and are on pace to finish this year around 1.5m units – in other words, back to the level last seen in 2009 during the global economic crisis, when the Russian market collapsed by half.

Executives from logistics providers at the Automotive Russia Conference in Moscow admitted that they were mainly in ‘survival mode’, however a resilience and determination was evident among many speakers to remain in the market and play a role in its eventual recovery. Elena Lukanova, the president of Adampol, a Polish-based logistics provider that also has a Russian fleet along with warehousing and knockdown business between Europe and Russia, even pointed to the bright side of Russia’s otherwise dark economic indicators. Just this month the World Bank revised its forecast for Russia’s economy, predicting a contraction of 2.8% of GDP rather than 3.8%, while growth should resume next year. For vehicle sales, increases could be as high as 20% by 2017 from today’s low base. Meanwhile, Lukanova also expected more countries to join the Eurasian Customs Union that Russia has initiated with neighbours including Kazakhstan, Belarus and, as of this year, Armenia and Kyrgyzstan.

In this report...

More news from Moscow...

Video recordings are available here

“This is positive for logistics, because it means that a car assembled in Kazakhstan or Russia can be moved more easily throughout any country in the Customs Union,” she said.

Lukanova also pointed to higher investments likely to come from China and Asian companies as Russia shifted more of its trading focus east. Her company was something of an example – earlier this year Hyundai Glovis, part of South Korea’s Hyundai Motor Group, completed its acquisition of a 70% stake in Adampol. Incidentally, Hyundai-Kia has been among the brands that have greatly increased their marketshare in Russia during the crisis (the two together now outsell the Lada brand, for example).

Striking an optimistic and patriotic note, Lukanova, herself Russian, even suggested that the absorption of Crimea from Ukraine would eventually benefit Russia by growing its population (although currently, there are virtually no vehicles able to arrive in Crimea). She praised companies like Ford and Jaguar Land Rover, who were maintaining or expanding operations in Russia or the Customs Union even in hard times; she suggested that General Motors, on the other hand, which is withdrawing most of its sales and production in Russia, would go the way of Pizza Hut, which left the Russian market in the late 1990s and struggled to re-enter it later.

Despite its obvious problems, there is still considerable automotive investment in Russia. The country’s largest carmaker, Avtovaz, is modernising under the leadership of its CEO, Bo Andersson, and in partnership with the Renault Nissan Alliance, which owns a majority stake. Despite drops in sales, Avtovaz production this year is actually expected to remain stable or slightly increase from its 2014 levels, as the Lada brand launches several new models, and further Renault, Nissan and Datsun models are built at Avtovaz factories. (The scale of the company’s difficulties was demonstrated this week, however, as supplier issues led to a production stoppage.)

Ford Sollers, a joint venture with three plants in Russia located in St Petersburg and Elabuga in Tartarstan, is in the midst of a major launch schedule in Russia, with seven new models in two years. These sales and production launches are also being done in conjunction with efforts to increase the localisation of suppliers in Russia from a ratio of just 25% to more than 50% in a short timespan.

“We have never launched seven vehicles in 24 months before anywhere in the world,” said Roger Rogers, executive director of material planning and logistics at Ford Sollers. “We’re also increasing localisation in a market that has fallen for us by more than half.”

Karel Schnock, executive director of HWC International, which specialises in parts logistics and warehousing for a number of OEMs, pointed out that this was already the third crisis that he had seen in just a few years of working in Russia. “Business will pick up again, we firmly believe this,” he said. “The challenge is to cope with all of this, stick to the rules, but also to set up a transparent, cost effective supply chain that benefits all the participants – not just the OEM.”

Resilient Russians

Speakers also noted resilience among logistics providers and suppliers in Russia. While some smaller companies have gone out of business, so far the major providers have not succumbed to financial collapse or withdrawal from the country. Alexey Kokotkin, manager of vehicle logistics for Toyota Motor Russia, said that the company was looking carefully at the financial results of its carriers, but that it still made sure the routes and services were profitable for logistics providers.

“We run an open book principle with costs broken out. We are sure from both sides that it is real costs included in the tender, plus some ‘alpha’ that is for the provider’s profit,” said Kokotkin. “Also, by improving our on-time delivery and truck turnover, we as OEMs and logistics partners profit.”

Alexey Kostenko, who works in supply chain design and logistics services at Magna International Europe, and Adam Misiak, global manager for international logistics at tier supplier Delphi, both agreed that their companies require robust financial reporting, and they remained confident in the ability of their logistics providers in Russia to maintain service.

“We do risk analysis, and it is almost impossible to get the business without reliable financial statements. We look carefully at our logistics providers’ finances and sometimes we even audit them,” said Kostenko. “We do everything possible to avoid the financial failure of a provider.”

Likewise, speakers at the event spoke about wanting to engage more closely with logistics experts, and develop further relationships in Russia rather than cutting providers adrift. Roger Rogers noted that Ford Sollers was specifically looking for development of Russian talent, including local logistics providers that have a full understanding of Russian conditions. “We can’t parachute in expats and run Russia’s supply chain competitively. We need to develop local talent both within Ford Sollers and at our logistics providers,” he said.

Adam Misiak agreed that improving local logistics providers would be a crucial part of Delphi building a successful supply chain in Russia. He still saw huge gaps within the domestic market in terms of moving material. “I think for that, local partners are required,” he said. “We tend to work with the big international logistics providers operating in Russia but there is scope for developing local partners. We know how to bring it in from outside Russia but, as with the suppliers, we need to know how to bring it to our plants within Russia with local providers.”

Rogers added that he saw significant scope for outsourcing more logistics services in Russia, including for in-plant logistics and line feeding, which the joint venture does in-house today in Elabuga, as well as planning and management activities.

“We’re trying to encourage more 3PL and 4PL-type services for our logistics," he said. "We want even existing partners, like deep-sea carriers, to bring some value to the business. For example, rather than me managing transit time, why can’t they manage the mode? We want logistics providers to do more of this.”

Pain in the supply chain

While it was encouraging that the difficult business climate in Russia has not stopped carmakers and logistics providers to invest in and improve their businesses, it is sobering to reflect on a market that may now be facing an even worse economic situation than it did in 2009. Passenger car sales in the first five months of this year are down by nearly 40% compared to 2014 (a year in which the market already declined for the second straight year). According to Sergey Litvinenko, director of automotive advisory services at PwC, the forecast for the rest of the year is a drop of 35% to 1.52m units.

While the whole market is suffering, the pain is particularly sharp for imported vehicles, which are forecast to drop 55% (to 290,000 units). Carmakers that made efforts to localise their production in Russia in recent years are not always getting this benefit either: PwC expects that foreign assembled cars will finish the year 33% down on 2014 at 860,000 units. Russian brand vehicles, meanwhile, helped in part by government subsidies and incentives, will slide 10% to 370,000 units, though that figure may be lower should the government phase out a scrappage scheme in place.

“Government support is important to the sector,” said Litvinenko. “It is an important question whether the government will continue to fund the current programmes. The Russian budget has already been revised and decreased.”

Although the drop in the rouble versus the dollar and euro would in theory make Russian vehicle exports more competitive, the country’s vehicle plants are mainly engineered to serve the Russian market and neighbouring Commonwealth of Independent States, countries whose economies also tend to suffer relative to Russia. The Eurasian Customs Union, which now includes Russia along with Kazakhstan, Belarus and, from January this year, Armenia and Kyrgyzstan, presents further opportunities for export, but little that can make up for the scale of the Russian market’s decline.

Mikhail Cherekaev, deputy director of trade policy at the Analytical Centre for Foreign Trade at Russia’s Ministry of Trade, revealed that vehicle exports had fallen in the first quarter by around 30% in value terms. There are, nevertheless, several examples of carmakers, including Hyundai, Nissan and Lada, trying to increase exports.

Carmakers and their suppliers may be bunkering down for a long slog. Although the Russian economy is expected to return to moderate growth next year, vehicle sales are not expected to make a quick rebound the way that they did after 2009. PwC doesn’t see passenger vehicles reaching their 2012 peak of 2.8m units until 2019 at the earliest even in a “best case scenario”, said Litvinenko. A market that was once expected to sell more than 3.5m vehicles by 2015, and to have surpassed Germany as Europe’s largest new vehicle market, is now forecasted to sell between 3.1m-3.4m vehicles only by 2024 or 2025.

Already the situation has cost the industry the larger part of one carmaker: GM will stop production at its St Petersburg plant – the capacity for which it had been in the process of increasing – as well as contract assembly volume at Kaliningrad and at the Gaz plant in Nizhny Novgorod. The camaker is ending sales of Opel vehicles in the country along with the majority of Chevrolet models (it will maintain a joint venture with Avtovaz that builds the Chevrolet Niva). While GM’s response is so far the most dramatic, other brands are also withdrawing models from the Russian market and slowing production. Volkswagen Group, Peugeot Citroën and Mitsubishi have temporarily idled their production lines in Kaluga. Logistics providers at the conference wondered who might be the next carmaker to pull out altogether.

The impact of the market’s fallout on the supply chain has of course been dramatic, with freight volumes and rates going down. On top of that, high inflation, which has been close to 12% per year both in 2014 and this year, has led to higher costs. “We have to increase the pay of our drivers by around 15% per year to keep from losing highly skilled, educated and trained people,” said Elena Lukanova.

Even with a positive outlook, she added that business was a matter of “survival” until the vehicle market hopefully improves in 2017. “Everyone has a lot of problems with financing, for example, so maintaining quality is hard,” she said. Other logistics providers in the country have also acknowledged that they are reducing their fleets and staff in response to the crisis.

Local needs

The crisis has other brought other impacts to bear upon the wider supply chain in Russia. Over the past five years since the market first started to recover from the global economic crisis, both government policy and manufacturers’ strategies have focused on increasing localisation of assembly and component supply in Russia. A number of carmakers including GM, Ford, Renault Nissan and the Volkswagen Group, as well as tier suppliers, signed agreements with Russia’s Ministry of Economic Development that set production capacity and localisation targets in exchange for duty and customs exemptions that could be worth as much as 30% of their costs.

The collapse of the market raises issues around both manufacturers’ ability to localise their supply chains as well as how the government measures the targets and will react should a company miss them. The lower production of vehicles makes it harder to attract more tier suppliers to build or expand plants in Russia, or to develop new equipment and tooling. Already, some tier suppliers have started to retreat from the market, while the economy makes it more difficult for local Russian companies to develop further.

However, there is also an issue in assessing carmakers’ progress, particularly in calculating the value of imported content given the depreciation of the rouble, which has lost more than half its value against the dollar. That means the ratio of value for imported components in the final price of a product has consequently risen by more than the value of localised parts.

“Many companies who have been localising their production in good faith already missed targets last year, and would struggle to keep up with the more aggressive localisation rates scheduled for the coming years,” said Wilhelmina Shavshina, legal director and head of DLA Piper’s foreign trade regulatory practice.

Localisation targets themselves vary by commodity, with things like suspension modules, engine parts and exhaust systems needing to reach 15% of their value within Russia by 2014, but rising afterwards to 30-45% within several years.

“The initial localisation rates were fairly easy for companies to reach just by setting up local assembly in Russia,” said Shavshina. “But adding value is harder, especially for those who agreed those percentages at a certain dollar-rouble exchange rate. At those rates, they would have reached 45% by this year, but the decline in the rouble last summer has taken that back.”

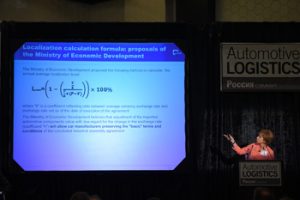

The government has composed a mathematical equation that is supposed to compensate for this change in value, but Shavshina indicated that the formula itself was flawed, if not altogether baffling. “It is not based on logic,” she said, explaining that it doesn’t compensate for the actual fall in the rouble’s value. The risk is that companies who fail to meet their targets might then lose benefits from the programme.

Localisation is critical for manufacturers in Russia, not least to contend with the risks around the rouble’s depreciation. It is evident that some companies have struggled or for various reasons decided not to move much further than setting up assembly operations in Russia, continuing to rely on a high amount of imported parts or knockdown kits. Sources suggest that GM’s production in Russia was only around 20% localised. Delphi and Ford have also had localisation rates of around 20-25%, although this is now changing.

Ford Sollers’ Roger Rogers acknowledged that setting up a new supply base was difficult, and in some cases had resulted in line stoppages or quality issues in Russia. The carmaker’s supply chain for Russia remains remarkably global, with sources that include China, Turkey, Germany, the US, Mexico, South America and others. “The pipeline is often 60-70 days. Every time something happens, it ripples out everywhere,” he said. “If we cut 10 units from production, I’ll get demurrage. If I add 10 units of freight, I have premium freight.”

However, he says that Ford Sollers continues to localise its products in line with targets, and that it would be essential to the carmaker’s success. “We all recognise that localisation has to take place, even if it is just to avoid Russian customs,” he said.

This concern is shared at the tier one level. Delphi’s output of components in Russia is exclusively for the domestic market but it still has to being in 80% of the materials it uses from outside the country.

“We have challenges in bringing our suppliers closer to our plants,” said Adam Misiak at Delphi. “The challenge is always the cost here. I don’t know why but Russian customs is extremely expensive.”

Speakers acknowledged that the challenge was not only about the quality of parts suppliers, but also the quality of local logistics providers. Magna’s Alexey Kostenko said that logistics providers in Russia should be able to offer the same quality service as Magna would expect in Europe.

“We need local LSPs with the same standard of services we get in Europe,” he insisted. “A cheaper company should not mean a drop in the service level.”

Kostenko pointed to Magna’s web-based portals used to running logistics tenders, which applies global standards and processes across the tier supplier’s logistics procurement. “By running the demand for a specific project we invite up to 100 service providers to the table and then by tendering over several rounds and negotiating we select one,” he said. “This is a transparent process and every service provider can take part. It works in Russia.”

No easy way out

For today’s Russian automotive industry and supply chain, there is no one single solution that would likely solve its fundamental problems. There was and remains long term recognition about poor infrastructure, inflexible rail services, complicated and costly customs procedures, and the need for more quality, local suppliers. However, as companies brace themselves for further falls or a lengthy wait for economic recovery, there is clearly less appetite for investment, fleet renewal, or lengthy IT projects.

However, speakers and participants demonstrated that they have not lost focus on improving everything they can about their supply chains. Roger Rogers, in a focus on “back to basics”, stressed the importance of using the right plant logistics and line-feeding systems and processes, whether that means visual cards, iPads for call-off information, kitting for some commodities and pick-by-light systems.

Toyota’s Alexey Kokotkin, meanwhile, revealed how Toyota has improved its damage rates for road and rail flows, while also making important productivity improvements in its vehicle yards and distribution centres. Backlogs having been reduced from 15.7% last year down to 2.4% in the first five months of this year, for example. Perhaps most critically, Toyota has switched to a multi-shift loading process at storage terminal points of pick up for onward delivery, with specified delivery windows.

“Last year we had no standard for arrival [of trucks] within the day. They could arrive day or night,” he said. “Now it has been standardised with two daily specified slots within three hours on two time slots or loading shifts. Providers now have to follow this procedure and have a standard loading duration of two hours.”

Nataliya Zakirova, head of sales for Gefco Russia, pointed out that the company, majority controlled by RZD Russian Railways since the end of 2012, had further increased its capabilities in Russia, including in customs clearance and brokerage. A number of companies, including Ford Sollers’ Rogers, also voiced interest in Gefco and others’ rail services between Europe and China.

The success of such services and developments will inevitably come down to Russia’s automotive market and economy. But in the meantime, executives stressed the importance of working together and building trust. Karel Schnock from HWC International, challenged carmakers and manufacturers to open up and be willing to build transparent supply chains, rather than looking to “squeeze” supplier on price.

“It all starts with trust,” said Schnock. “Trust is often the dirtiest word in the Russian language because we have so little of it. But if you can trust your partners, together we can build the right supply chain for Russia.”

Magna’s Alexey Kostenko joined others in emphasising the importance of partnership between manufacturers and logistics providers. “Success is about partnership and we are not just talking survival we are talking about moving the industry forward toward the years when the economy will grow and will be ready for the next step to the future,” he said.

Video recordings of the main sessions at this year’s Automotive Logistics Russia conference can be viewed by clicking here.

The next conference in the Automotive Logistics series of global events will be Import/Export North America on August 12th in Baltimore, followed by Automotive Logistics Global on September 22-24th in Detroit.

The next conference to take place in Europe will be the 2015 ECG Conference in Vienna, Austria on October 15-16th.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}