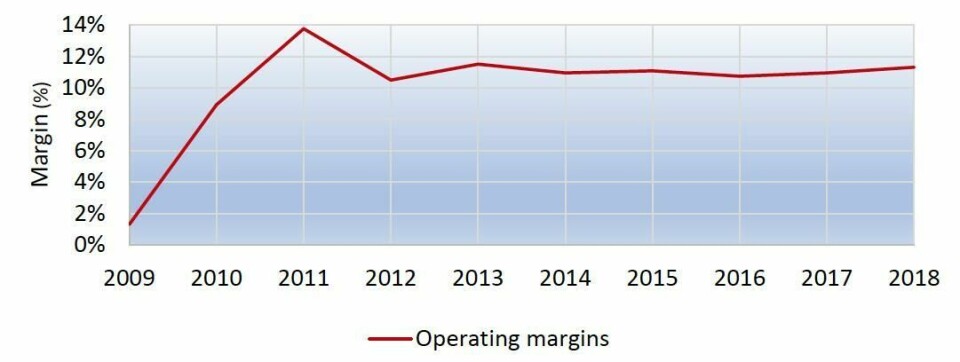

Automotive suppliers buying and spinning their way into high tech segments

As BorgWarner’s acquisition of Delphi Technologies shows, tier one automotive suppliers are turning to acquisitions and restructuring their business to focus on advanced technology, helping to protect margins, avoid commodification and transition to electrified powertrains

However, those suppliers with better performing margins are often those producing more dynamic, specialised technologies, for example in advanced electronics or driver assistance systems, rather than those focused on highly commoditised products, such as seats or mechanical engine parts.

We expect that this divergence in financial performance is likely to continue as vehicles take on more sensors, electronics and software. If suppliers are to protect their profit margins, they will need to offer more than products available at the lowest bid.

Advertisement

In our analysis, for example, suppliers with the best performing margins include Aptiv, the spinoff of the former Delphi Automotive, which is now highly focused on electronics and software products for advanced driving assistance systems (ADAS), with the former powertrain unit now a separate company as Delphi Technologies (which is itself being acquired by another supplier, BorgWarner).

Continental, meanwhile, which has seen its margins decline, has separated its powertrain division into a separate unit, called Vitesco, with a view to focus this business more on electrification. Continental’s automotive division, meanwhile, will look to accelerate higher-performing activities in electronics, sensors and software.

While powertrain component suppliers are challenged by shifts to electric and hybrid vehicles, not all powertrain suppliers are seeing the same level of margin compression. BorgWarner has performed strongly, benefiting from specialisation in automatic transmissions, for example, a segment that continues to grow. Its turbochargers are also competing well, helped by OEMs’ push to improve fuel efficiency whilst improving overall driving performance.

Such companies perform well even if they are not able to invest as much into R&D as the largest, most diverse global players, such as Bosch, Magna or Denso. However, concentrating in key areas where there may be fewer competitors is key for these companies. In our analysis, automotive suppliers focused on high volume, but lower value-add products, whether seating, wire harnesses or ball bearings, have seen profit margins decline faster than those in high-tech areas.

But even if suppliers like BorgWarner have maintained reasonably healthy profits, they face the same challenge as other tier suppliers of declining volume and investment in powertrain components. That is one of the key reasons behind its decision to acquire Delphi Technologies, which will further consolidate its share and scale in powertrain technology. Along with its ICE product technology, the acquisition also gives BorgWarner access to more of Delphi’s electronic and software controls, which will help it to transition to electrified powertrains.

Following our latest report, Automotive Tier Supplier Profit Analysis 2020, our automotive analysts at Automotive Logistics discussed where Tier 1 supplier profit margins are heading, what the impact will be across the supply chain, and provided practical insights around how to manage margin compression.

Mobileye and Intel are developing full technology stacks that include Intel hardware and software, as well as mobility-as-as-service offerings. Such companies may be better placed to compete on software and data monetisation, and become much more significant, if not dominant suppliers.

Advertisement

But these technology and services are also potentially high margin opportunities for traditional tier ones. Most software companies are likely to seek partnerships with manufacturers and integrators to deliver products in the complex automotive supply chain. Suppliers thus have the opportunity to retain their significance in these new segments through closer collaboration, whether through technology sharing or alliances, joint ventures or formal M&A activity.

While each company’s circumstances will vary, our analysis suggests that the new decade will bring with it more disruption to automotive suppliers’ business models and profits, with volumes under pressure, high investment requirements and products at risk of commodification. More consolidation is likely to follow.

But an industry in transformation also brings huge opportunities. One thing is clear, if leading tier suppliers are to maintain their lead, and their margins, they will have to change with the sector.