Global trade disputes could dim electric vehicle supply chain potential in key markets

Trade uncertainties such as those between the US and China, or the UK and the EU, could put the brakes on growth in the electric vehicle and battery supply chain for some OEMs and countries, despite bullish forecasts for alternative powertrains

The automotive industry is highly exposed to trade disputes, tariffs and the ongoing ideological and economic battle between protectionism and free trade. The industry has some of the world’s most complex supply chains, many of which cross multiple borders as a matter of course, including a large number of international shipments that move in just-in-time, if not just-in-sequence flows.

As has been widely discussed and cited by automotive firms and associations both in the debates over Brexit as well as in renegotiating the North American Free Trade Agreement (Nafta), any significant disruption to these movements, be it higher tariffs, lengthy border checks or regulatory compliance issues, can put assembly lines at risk. The costs would also likely erase the relatively low operating profits typical across OEMs and tier suppliers – margins which have averaged just 4-8% and are under even more pressure today in the face of sluggish economic growth.

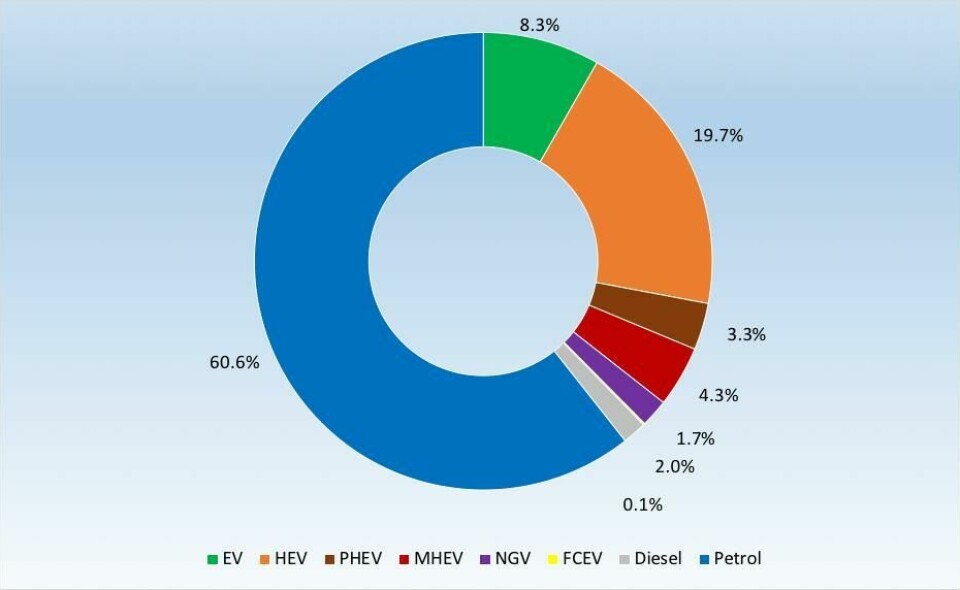

What’s more, the extra costs and red tape in global trade complicate OEM and tier supplier investments and plans for significantly greener, more efficient technology. For example, automotive companies are spending billions of dollars to transition to electrified powertrains, in part to meet tightening emissions regulations in major markets like the EU, China and Japan. Over the next decade, Automotive from Ultima Media forecasts that the combined market share of hybrid, electric and hydrogen powertrains among new vehicle sales will increase from around 8% today, to 55% by 2030 (download the full report, Automotive Powertrain Forecast 2020-2030).

For electric vehicles, supply chains are and will be intensely global, whether in sourcing battery cells, microchips and electronics, or in spreading R&D costs and intellectual property across regions. We expect that alliances between OEMs and suppliers in sharing electric vehicle development, production and charging infrastructure costs – such as those recently agreed between Volkswagen and Ford, Toyota and Subaru, BMW and Daimler – will only increase, spreading across more regions and over more borders.

Extra burdens that arise from tariffs, as well as border checks, certifications and rules-of-origin declarations, not to mention restrictions on labour and talent, slow down many aspects of the automotive supply chain. But we believe that they pose a particular risk to the developing value chain for electric vehicles. Just as closing off trade and technology exchanges between, for example, the US, Japan and China would have greatly hindered the rise of the smartphone industry over the past 15 years, so too would higher tariff and other barriers slow the development of EV and battery technology and make it more expensive – costs that the industry and consumers can ill afford given that EVs are still largely unprofitable for most OEMs and seen as too expensive by most consumers.

US-China trade war could block EV market and technology access

A glimpse at ongoing trade disputes illustrates the risk to current and future supply chains. The continuing US-China trade war, for example, has undoubtedly impacted global growth across multiple industry verticals. Ongoing sanctions by the US government have clouded the macroeconomic climate, harmed consumer and investor confidence, and particularly affected the automotive industry.

Automotive manufacturers and associations have voiced serious concerns about the dispute, and it remains one of the biggest issues challenging the overall health of the sector – with an even bigger impact than a potential no-deal Brexit or delays in ratifying Nafta’s successor, the US Mexico Canada Agreement (USMCA).

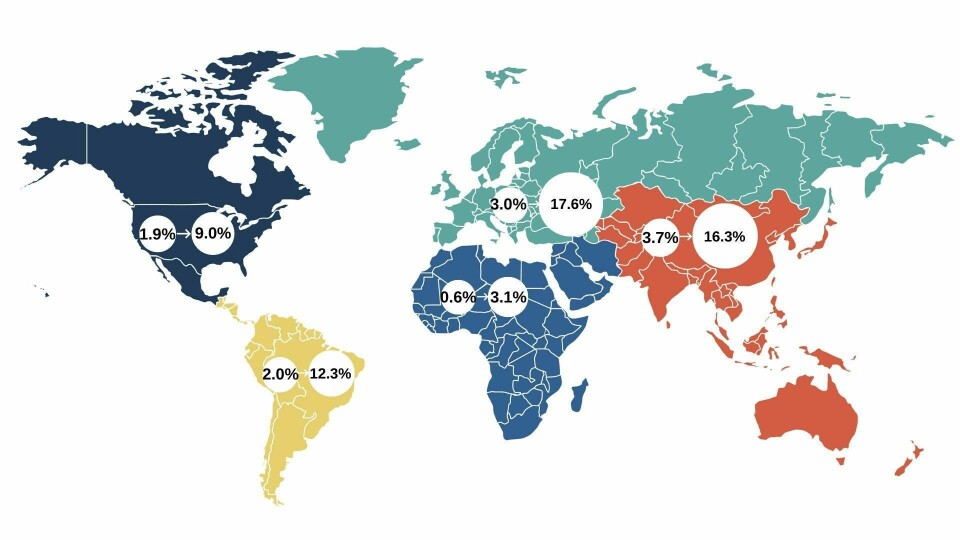

This trade war carries significant risk as well as for electric vehicle development and sales. China has emerged as the largest global market for EVs, with sales of such vehicles largely bucking declines in the wider market over the past two years. We forecast that the sales of pure battery electric vehicles in China will rise dramatically over the next decade, from 700,000 units in 2018 to 7.2m annually by 2030.

For a full forecast of global and regional powertrains to 2030, download our report here

Just as the rise of Chinese vehicle sales and especially premium vehicles fuelled profits for many OEMs over the past decade, so too will EV growth be central to their expansion and financial health in the next decade. Whilst American OEMs continue to build, invest and sell in China mainly through joint ventures, both the political, economic and consumer backlashes of the trade dispute risk weighing on the sales of brands like Buick, Jeep and Ford. Tesla, which has started work on a China factory, has had to increase prices of its US-built vehicles to China following higher tariffs. Chinese vehicle brands and startups, meanwhile, stand to make gains.

American manufacturers or US-based factories that face barriers to the Chinese EV market over the next decade would be at a huge disadvantage. So, too, would those companies’ supply chains, as the economies of scale in China will be essential in lowering overall EV and battery costs.

Of course, the blade cuts both ways. The US-China trade dispute has negatively impacted China’s overall economy. It will also hinder Chinese brands and startups from entering and competing in the lucrative American market. Chinese EV startup Nio, for example, has hit financial trouble and its earlier plans to sell vehicles in the US now look likely to be delayed if not cancelled.

What might USMCA mean for EVs sales and production?

Along with the China dispute, the US had also been locked in negotiations with Mexico and Canada over a replacement for Nafta. The subsequent USMCA still needs to be ratified by both the US and Canadian governments, with uncertainty remaining over its passage. But even as the worst-case outcome of a US withdrawal from Nafta appears to have passed, questions remain about how positive the new deal will be for automotive production and sales – including for electric vehicles and batteries.

The key differences between the USMCA and Nafta are new rules-of-origin and labour stipulations. The new agreement increases North American content requirements for vehicles built in the region eligible for duty-free trade from 62.5% to 75% of components (by net cost) by 2023; OEMs will also be required to source 70% of steel and aluminium for these models from within North America. Furthermore, OEMs must manufacture at least 40% of vehicles in factories where production line workers earn at least $16 per hour.

Whilst there are different estimates of the deal’s impacts, it is likely that the cost of vehicle manufacturing in Mexico – where labour costs are on average well below $16 per hour – will increase. Likewise, with higher levels of US and Canadian components instead of lower-cost Mexican or imported parts, North American production costs overall will rise. That would mean either higher vehicle prices and a likely decline in new vehicle sales, or lower margins for OEMs as they absorb higher costs. We expect that OEMs will implement a mixture of these strategies, including exerting more pressure for cost savings on their supplier base.

Download the full report and powertrain forecast here

While the USMCA is likely to maintain if not encourage more investment in North American vehicle manufacturing, its impact on electrified powertrain development in the region is likely to be mixed. Thanks to looser overall regulations on carbon emissions and fuel economy, longer driving distances and different cultural preferences, we forecast a lower penetration of EVs in North America than in Europe and China.

Those differences will challenge carmakers; with lower volumes in the US and a higher dependence on petrol powertrains, they may not be able to leverage global electric vehicle platforms and battery technology to their fullest extent. Complications in rules of origin under USMCA could bring more difficulties, especially for electric batteries and battery cells, which make up a large share of an EV’s value.

For example, both Volkswagen Group and Mercedes-Benz are preparing to build electric vehicles at US plants in the coming years. However, lower EV sales in the US make it more likely that these OEMs would look to import battery cells from Asia or Europe where EV supply chains will be stronger. Indeed, German brands producing in North America already import most engines and powertrains from Europe.

However, such high-value imports would make it more difficult to meet local content requirements, leaving manufacturers with a tough choice between investing in potentially unprofitable local supply, or risking additional tariffs and red tape across North America.

According to analysis by the US International Trade Commission, an independent federal agency, current classification rules mean that even assembling batteries in North America would not be enough to confer local origin to these parts; the battery cells must also be produced locally. This would currently be a supply challenge for all vehicle manufacturers in the region besides Tesla.

Over time, the value chain for battery cells will grow in North America. However, imports are likely for the foreseeable future and, even over the long term, OEMs and suppliers will need to leverage battery and EV value chains across global markets to make them viable.

Brexit could divide UK and EU electric vehicle markets

As has been well reported, a disorderly Brexit would result in tariffs on automotive goods moving between the UK and EU as well as new customs checks. The consensus view across the automotive sector is that the imposition of such barriers would be extremely detrimental for the sector and likely make a large amount of current UK-based vehicle manufacturing unviable. The European automotive industry would also be badly impacted, with the UK a large market for imported European-built vehicles and components.

The impact for future EV sales, development and production in the UK could also be severely negative depending on the Brexit outcome. In our forecast, Europe (including the UK) will be the second largest market for EVs after China, with strong growth also expected in hybrid powertrains, driven in large part by very strict carbon emission rules set to tighten in 2020.

For a full forecast and analysis of powertrain types to 2030, download the report here

There is some speculation that, in the event of a no-deal outcome, UK sales might no longer count towards the fleet targets set by the European Commission for carmakers selling in the EU. That could, in theory, result in OEMs offering more EV and hybrid models in EU countries than they would in the UK as higher EU sales of low-emission vehicles would mitigate potential fines.

We are broadly unconvinced that this would be the case, in part because the UK is a large vehicle market that OEMs are unlikely to ignore. The UK government has said it would maintain emission targets, while EV and hybrid sales in the country will be influenced by incentives set by the government. However, until it is clear how aligned the UK remains to the EU single market for goods, it is hard to predict with uncertainty what specific role it will play in calculating European fleet emission targets.

What is more certain, however, is that economies of scale will be king when it comes to battery production. Currently, Nissan produces an electric model and assembles battery packs in the UK, whilst Jaguar Land Rover and BMW have planned assembly of EVs; all, however, will import most high-value battery cells and components from Asia or Europe. Furthermore, the European battery supply chain looks set to grow strongly beyond UK shores. According to an analysis by the environmental campaign group Transport & Environment, 23 large-scale lithium-ion battery cell plants have been confirmed or are likely to open by 2023 in Europe – none of them so far in the UK.

Whilst the UK is rich with research and science in battery and electric vehicle technology, both production and sales of EVs will depend on access to large markets and developed supply chains. Whilst Brexit may well create opportunities for global trade and technology exchange with the likes of China and the US, over the next decade we see the most certain opportunity for UK to be in Europe’s expanding EV and powertrain market.

Uncertainty burns

The biggest challenge for most OEMs and tier suppliers in global trade policy today is the uncertainty in so many areas as they plan large investments. That is why many manufacturers have supported resolutions to trade disputes even if they are less optimal than originally hoped. The automotive industry in Europe largely supports a withdrawal deal for the UK even if it does not guarantee frictionless trade in the future. In North America, OEMs such as Ford have supported the USMCA even if it seems likely to result in higher production costs, in part because the company sees it a price worth paying for more certainty.

And yet, the Brexit saga continues, with further delay now confirmed but little guarantee that the outcome won’t be messy. The US-China dispute has only worsened, with the latest tariffs escalating this past month. The USMCA is still held up in both Canada and the US, made even more complicated by recent elections and political turmoil.

Our forecasts assume eventual compromises to these issues. However, the longer they remain unresolved, the more complicated it will be for automotive manufacturers to develop and produce electric vehicles and powertrains across the stable, open and global supply chains that they will continue to require. More costs and restrictive barriers could over the coming years dim one of the more positive outlooks for what we already think will be a difficult period for the automotive industry.