Automotive logistics and supply chains in 2025: Tariff turmoil, investment uncertainty and further cost pressures

Daniel HarrisonDanielHarrison

PublishedModified

9 min

As tariffs disrupt established trade rules, OEMs and logistics providers must respond to cost pressures, restructuring and uncertainty across the auto sector.AI generated, Adobe Stock

The automotive industry is reeling from the US’s hugely disruptive reset of the world economic order, and this will have profound ramifications for logistics providers around the world.

The automotive sector has faced a multitude of headwinds, including the difficult transition to electrification, structurally lower volumes following Covid-19, rising costs and the threat from cheaper vehicles from China. US president Donald Trump’s new trade war added to the sector’s woes and could fundamentally reshape the global automotive supply chain. In this series, Automotive Logistics will delve into these issues to explore what they mean for the automotive industry and how it can prepare.

Top three challenges

Trump, tariffs and trade turmoil

Investment uncertainty

Cost pressures

1. Trump, tariffs and trade turmoil

On 9 April 2025, President Trump caved in to pressure from the stock and bond markets and reneged on his widely derided tariff policy.

Advertisement

Current US tariff policy is as follows:

Even though many countries did respond to the initial tariffs, all countries that ‘didn’t retaliate’ received a 90-day ‘pause’ on previously announced tariffs and will have a 10% flat rate tariff applied. This lower 10% rate was predicted in our recent European Automotive Logistics Market Report 2025-2035.

China’s tariff rate will go up to 125% due to retaliation.

On 'Liberation Day', 2 April 2025, US president Trump announced sweeping tariffs which had the potential to overturn 80 years of successful globalisation and free-market trade consensus.

For general (non-automotive) goods, the ‘reciprocal’ tariffs applied from 9 April would have been from 10% for the UK and 20% for the EU, following a general principle of higher tariffs for countries with larger trade deficits with the US – leading all the way up to an eye-watering 104% tariffs for China.

Notably, Canada and Mexico were exempt from Trump’s latest tariffs because they are subject to a specific executive order, issued with the justification of a ‘fentanyl’ crisis under the guise of national security. The two countries were initially subject to a 25% tariff for goods that do not comply with the US-Mexico-Canada (USMCA) rules of origin. This has increased to 35% for goods from Canada and 30% for goods from Mexico, although a pause of 90 days has been issued on the Mexico tariffs.

For automotive specifically, the US tariffs were broadly in two stages:

Advertisement

From 3 April 2025, 25% tariffs on all vehicle imports – except for Canada and Mexico, where USMCA compliant parts and vehicles will remain exempt. The 25% tariffs are only applied on the proportion of non-USMCA content, but this USMCA exemption also appears to be up for review.

From 3 May 2025, the 25% tariff will then also be applied to automotive components.

The claimed objective of the tariff policy was to reshore production and ‘bring back’ manufacturing jobs which have been lost overseas – however, the net result is likely to be the exact opposite. The previous Biden administration’s 2022 Inflation Reduction Act (IRA) was demonstrably a far more effective (and less economically destructive) approach which produced a multitude of new investments in the US that peaked during that administration.

Fundamentally, the current US administration wanted to unwind decades of economic integration and risk a 1930s-style global trade war.

Most economists, banks, businesses, governments and trade experts took the strong view that these tariffs would be deeply damaging – they would slow down trade and economic growth, and result in a lower standard of living for individuals. Furthermore, many economists openly condemned the tariff policy as likely to trigger a recession.

In our view, ‘Liberation Day’ (if followed through) would have gone down in history as one of the greatest acts of self-harm to the US economy as well as the global economy, and the financial markets overwhelmingly agreed.

Stock markets around the world unanimously spoke. All fell sharply and approached the technical definition of a market crash (a 20% fall).

So, what were the immediate effects on the auto sector?

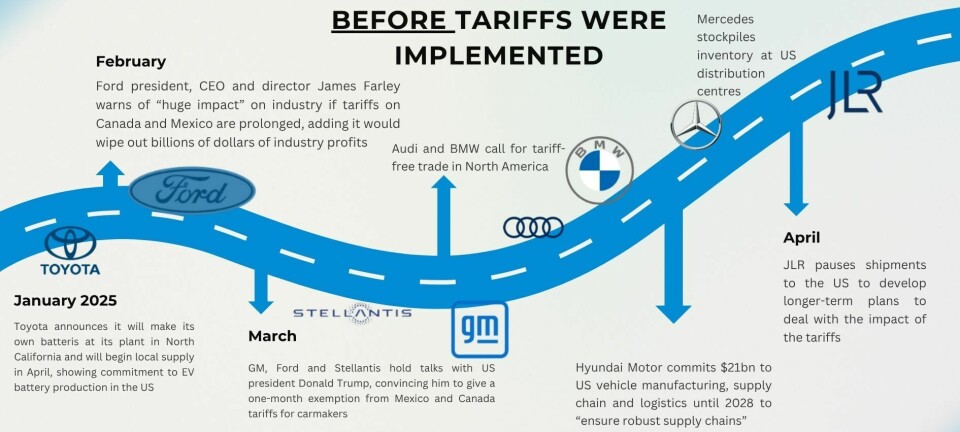

Automotive OEMs such as Stellantis had already temporarily shut down its assembly plant in Windsor, a Canadian city on the US border.

Stellantis suspended production at its Toluca, Mexico plants with the loss of 900 jobs, with the decision likely to also lead to layoffs and work stoppages at US powertrain and casting plants that serve those facilities.

Nissan transferred Rogue production from Japan to Tennessee.

The key word here is ‘uncertainty’. The 90-day pause is far from guaranteed and does not seem to apply to the automotive sector. The initial level of tariffs were widely perceived as unsustainable and, if kept in place, would have had a devastating impact upon both automotive OEMs that export to the US and North American automotive OEMs themselves.

Trump’s strategy initially appeared to be a power play–imposing unrealistically high tariffs to begin with so governments and industries came to negotiate individually in exchange for other concessions, including increased to markets or adjustments to exchange rate. However, the overwhelming pressure of bond markets meltdown changed this plan.

We have already witnessed Chinese retaliatory tariffs as high as 84%, and this will hopefully drive everyone to the negotiation table and lead to agreement for lower tariffs.

As we predicted in our recent European Automotive Logistics Market Report 2025-2035, political, financial market and consumer pressures ultimately forced the Trump administration to back down, and the current high tariff regime has been moderated.

However, our working assumption is that moderate tariffs will remain in place in the medium to longer term at a significantly higher rate than the current 2.5% ‘most-favoured nation’ automotive tariffs.

Consequences

However, even if these lower 10% tariffs remain in place, the impact will still be significant upon OEMs and logistics providers alike:

‘Tariff stacking’ could occur, whereby components are charged tariffs many times as they cross multiple borders or are subject to other additional tariffs. Tariffs could also be charged on both component and finished vehicles.

Because new vehicle prices will increase, used vehicle prices will also go up.

There is likely to be a net overall loss of American manufacturing jobs due to falling demand.

Some European, South Korean and Japanese OEMs will be majorly impacted and may well pull out of the US market. Europe is particularly vulnerable as 20% of vehicle production is exported to North America. Germany and Italian OEMs are particularly exposed.

Rapidly changing component shipments and finished vehicle flows. This could be negative as well as positive, with countries and trading blocs developing new trade agreements or routes, e.g., the recent Canada–EU or India–UK deals.

This restructuring signals major shifts in the demand for logistics services, requiring providers to adapt to new trade flows, routes and sourcing locations. As OEMs respond to changing market conditions, the need for flexible and cost-effective logistics solutions is going to be more critical than ever.

However, there is an even more serious problem for the US and the Trump administration. The tariff turmoil has significantly damaged the US’s reputation and standing in the world as a desired place to do business. If you were the CEO of a major OEM or tier supplier, you simply could not rely on the Trump administration or the US to provide a stable environment for long-term investments. That will hold back the country for at least this administration and possibly beyond.

2. Investment uncertainty

The doubt surrounding the Trump tariff announcements – including whether they are permanent, will be moderated or even cancelled at short notice – ultimately means that the business investment climate is one of extreme uncertainty or even paralysis.

Leading automotive experts have stated that a lack of clarity surrounding return on investment (ROI) – 10-year investment plans can’t be made due to uncertainty surrounding the next 10 minutes.

Whilst there is potential for OEMs and tier suppliers to grow and invest in North America and to reshore as much production as possible, the Trump administration will potentially only be in power for approximately 3.5 more years and the tariff landscape may drastically change at that point, nullifying any investment decisions. Therefore, any investments need to take a much longer-term view.

Hyundai’s Georgia Metaplant is an example of an OEM committing production to the US.Hyundai

The week before the 2 April tariff announcement, Hyundai committed to a $21 billion investment through 2028 in the US. This included a new $7.6 billion Metaplant in Georgia, targeting 1.2 million annual units and 100,000 jobs and included vertical integration and localisation of steel, batteries and vehicle production. Alabama and Georgia production facilities will also be upgraded, including Hyundai Motor Manufacturing Alabama and Kia Autoland Georgia.

However, the reality of any such new investment is that it will take several years. Furthermore, new plants are highly automated – particularly so in battery and EV production – demonstrating that reshoring production to the US will only generate a relatively small number of jobs. Hyundai stated that their $21 billion investment will only create 14,000 direct full-time jobs by 2028 with over 100,000 total direct and indirect job opportunities anticipated across manufacturing, technology and infrastructure – however, the US is a country of 340 million people.

Nonetheless, whilst this investment is welcome, this is very much an isolated case that the Trump administration understandably seized upon as proof of auto production being brought back home.

However, it must be remembered that tariffs will inevitably be inflationary. A weak economy and vehicle price rises will lower consumer confidence and vehicle demand, as there is less disposable income for discretionary vehicle purchases. Therefore, vehicle manufacturing capacity in the US is overall likely to decline and lead to job losses elsewhere, nullifying any potential gains that individual investments may make.

From the perspective of an automotive logistics provider, there is a likely to be a freeze on investment in capacity enhancement or any other non-essential area that can be trimmed back.

Alternatively, the extreme uncertainty may lead to very specific strategic investments around increasing flexibility, agility and resilience. Increased investment in digitalisation can enhance visibility, transparency and efficiency, improving network design and optimising capacity utilisation, for example.

One other possibility could emerge: if the US persists in its deeply isolationist and protectionist trade policy, the rest of the world could strategically make up for this loss of business by lowering trade barriers between all other countries, such as Canada-to-EU, China-to-EU, or between Asian countries.This would open up all sorts of new inbound and outbound finished vehicle logistics (FVL) business for LSPs.

3. Cost pressures

Pre-tariffs, automotive OEMs were already under increasing financial strain, driven by inefficiencies in production, heightened competition and the need to transition to electric vehicles (EVs). With demand not recovering to pre-COVID levels, OEMs are facing a price war, particularly against cheaper Chinese imports. This has resulted in margin compression, prompting OEMs to aggressively cut costs such as through plant closures and job cuts.

However, the wide-ranging tariffs will have a further profound impact on margins, resulting in a decline in profits and instabilities caused in both vehicle sales and supply chains. Such impacts will add to the barrage of disruptions already being faced by automakers and suppliers from slowing down electrification and grappling with heightened competition from Chinese OEMs. Automotive component suppliers, especially small and medium sized tier suppliers , will not be able to reshore component manufacturing to the US as higher labour costs impact their financial viability.

For logistics providers, these cost pressures will manifest in increased scrutiny of both inbound logistics and FVL cost structures. While cost reduction is a primary focus, it will require more than just freight rate cuts. Logistics providers must innovate through process optimisation, technology upgrades and improved network design. A top priority for OEMs is likely to be a focus on maintaining low vehicle inventory to reduce working capital, presenting new challenges for logistics providers.

Moreover, digitalisation, AI and automation are emerging as key tools for improving efficiency and reducing costs in the logistics sector. But, the RoI for these technologies remains a challenge, and logistics providers must balance cost reduction with strategic investments to remain competitive in such an uncertain climate.

As the automotive industry continues to evolve, logistics providers must navigate these dynamic trends and adapt to tariff turmoil, nearshoring, industry restructuring and cost-cutting. The key to success will be adapting to shifting supply chains, embracing technological advancements and staying ahead of regulatory changes. For those who can innovate and respond quickly, the immense challenges of 2025 and beyond could still present significant opportunities for growth and transformation in automotive logistics.