Automotive Logistics explores what each of the main challenges facing the industry will mean, and how the automotive logistics industry is responding.

1. Cost pressures

Automotive sector margins are being squeezed by a number of factors including tariffs, rising labour, energy and material costs, inefficiencies in production, increasing competition and the need to transition to electric vehicles, particularly within the context of much cheaper Chinese EVs.

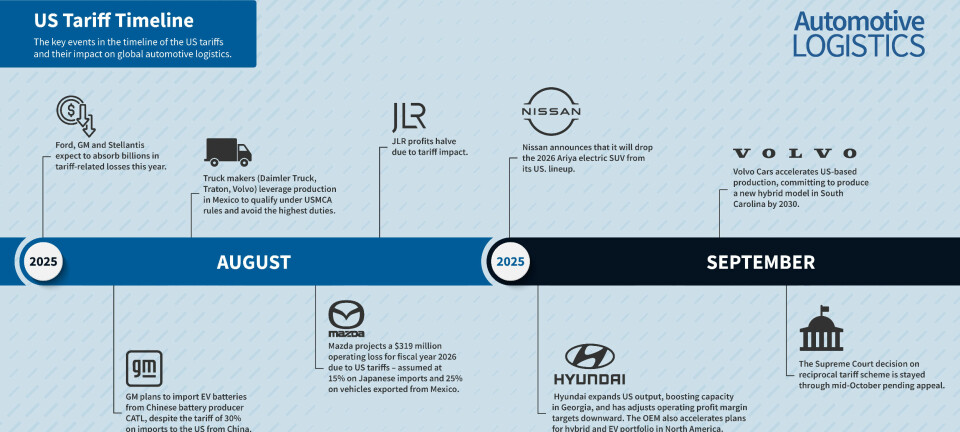

But what we do know for certain is that OEMs are currently absorbing the cost of tariffs, with prices set to rise according to Mike Wall, executive director of automotive analysis at S&P Global Mobility, speaking at our recent Automotive Logistics & Supply Chain Global 25th anniversary event in Michigan, US.

Another factor is that vehicle volumes also remain structurally below pre-Covid levels in both North America (approx. 1 million down and Europe (approximately 3 million down), so the previous economies of scale and plant utilisation rates OEMs relied upon, are no longer as possible, raising costs per unit. Furthermore, the gradual shift to EVs typically involves huge capital expenditure, combined with selling electric vehicles with lower margins. If EV sales targets are not met, in Europe at least, this can invoke OEM group-level fines.

Of course, this strategy of simply absorbing additional costs and eroding margins can't go on forever, as OEMs haemorrhage cash to remain competitive and retain market share. The consequence is margin compression, prompting OEMs to aggressively cut costs, including through plant closures and job cuts. OEMs and tier suppliers are therefore looking for any cost savings in the value chain, including inbound logistics and FVL, and there are anecdotal examples of OEMs pulling out of existing logistics contracts to reduce costs.

The impact of cost pressures, fluctuating demand patterns, and the gradual shift to EVs is also impacting the wider automotive supply chain with major german tier suppliers announcing significant job cuts.

Furthermore, in the US, leading service parts supplier First Brands has filed for bankruptcy, revealing billions of dollars in liabilities which also indicates considerable cost pressures are at play.

The impact of these decisions will cascade down the value chain , and create huge uncertainty for logistics providers. These cost pressures will manifest in increased scrutiny of both inbound logistics and FVL cost structures. While cost reduction is a primary focus, it will require more than just freight rate cuts. Logistics providers must innovate through process optimisation, technology upgrades and improved network design. There is also likely to be a focus on maintaining low vehicle inventory to reduce working capital as a top priority for OEMs, presenting new challenges for finished vehicle logistics providers.

2. Tariffs and trade uncertainty

The tirade of Trump tariffs in the first half of 2025 dominated the news agenda. These tariffs affected a wide range of sectors, but hit the automotive industry particularly hard, being one of the most complex and globalised sectors in the world and therefore one of the most exposed to trade barriers. Such is the level of uncertainty that stakeholders have effectively moved into a 'wait-and-see' holding pattern that creates strategic paralysis, resulting in major investments being paused, delayed or even cancelled.

The broad tariffs go beyond just finished vehicles and inbound components but also include raw materials such as steel, aluminium, copper, rare earth materials and semiconductors – all of which are major components featuring in modern vehicles.

But the trajectory of tariff policy has now taken a major turn and is at a significant juncture.

On August 29, the US Court of Appeals for the Federal Circuit ruled that US president Donald Trump cannot use the International Emergency Economic Powers Act (IEEPA) to impose broad tariffs and bypass congressional powers to impose so-called ‘reciprocal’ tariffs. The ruling won’t take effect until October 14 to give the Trump administration time to appeal to the Supreme Court, which it has done.

A Supreme Court appeal hearing was heard on November 5, with justices expressing doubts over the White House's justification of Trump's so-called 'Liberation Day' tariffs.

On the face of it, the Republican majority on the Supreme Court would indicate they may overturn the lower courts’ ruling. However, most commentators, based upon previous rulings, predict that the Supreme Court will likely uphold the lower courts’ ruling that Trump cannot use the International Emergency Economic Powers Act (IEEPA) to impose broad tariffs.

However, even if the Supreme Court rules against Trump’s tariffs, that won’t put an end to the trade war as many other legal avenues available are not likely to provide the same speed, scale or flexibility of using IEEPA and are unlikely to raise the same level of revenues.

In the meantime, the US government has announced a new US truck tariff from November 1. Nonetheless, the automotive industry remains in a holding pattern as we await the Supreme Court ruling and the next steps from the Trump administration. Therefore, uncertainty continues to reign supreme.

But what we do know for certain is that OEMs are currently absorbing the cost of tariffs, but prices are set to rise – that's according to Mike Wall, S&P Global Mobility, speaking at our recent ALSC Global event in Michigan, US. Therefore, tariffs will inevitably be inflationary and – once higher vehicle prices feed through – decrease consumer affordability, resulting in lower volumes and ultimately reducing automotive logistics flows and revenues.

This restructuring signals major shifts in the demand for logistics services, requiring logistics service providers to adapt to new trade flows, routes, and sourcing. As OEMs respond to changing market conditions, the need for flexible and cost-effective logistics solutions is going to be more critical than ever.

3. Supply chain disruption

Trade wars are the primary cause for current supply chain disruption, with multiple knock-on effects. The consequence of widespread tariffs, is that OEMs are investigating near-sourcing or alternative sourcing of components to avoid tariffs, whilst tier suppliers are seriously considering re-shoring/nearshoring their manufacturing footprint to help meet that changing demand.

For example, the more protectionist stance driven by Trump’s tariffs has already driven OEMs to reshore, with major announcements regarding nearshoring strategies issued by the likes of GM, Hyundai, and Stellantis. This has real implications for supporting tier suppliers and logistics providers as trade flows evolve and new routes emerge.

With most companies following a similar rapid shift in sourcing strategy, this clearly leads to significant changes within long-standing supply chain flows, routes and component production, creating shortages and affecting inventory levels, which in itself is contributing to supply chain disruption.

Tariffs applied by the US onto Chinese imports, led China to retaliate to those trade barriers not only with tariffs, but also by imposing export controls on critical rare earth materials leading to shortages in many parts of the supply chain around the world. Rare earth materials are critical within the manufacturing of a multitude of different automotive components, not just the obvious powertrain electric motors of EVs, but also non-powertrain electric motors, catalytic converters, sensors, and many other electrical components in all types of modern vehicles.

A breakthrough in the flow of rare earth materials from China came after Trump's recent meeting with China's president Xi Jinping in Busan, South Korea, fuelling hope in this regard for the automotive sector. Nevertheless, trade wars and tariffs fundamentally multiply complexity exponentially for OEMs, tier suppliers and logistics providers, around suppliers, sourcing location, routes and volumes.

Another impact of tariffs are the challenges around understanding HS codes, tariff stacking and the minutiae around USMCA rules of origin, and developing the lowest cost sourcing strategy to improve that USMCA compliance as the potential costs savings are significant. As a consequence, huge demand for employees with tariff expertise has been created in helping to navigate this rapidly evolving trading landscape.

Furthermore, on the outbound FVL side, many OEMs are prioritising low inventory levels to help reduce working capital, which adds further complexity to logistics operations.

However, the wide-ranging tariffs will have a further profound impact. Many automotive component suppliers, especially small and medium-sized tier suppliers, may not be able to reshore component manufacturing to the US due to higher labour costs in the US impacting their financial viability.

Furthermore, within the context of continuing chronic uncertainty and disruption, we are detecting a gradual shift away from supply chains being designed around the usual ideal (cheapest) business case, but instead network design being optimised around the most robust and resilient option. This may be slightly more expensive in the short term, but in the medium to longer term will lower cost, and ultimately better protect the business from unforeseen events.

Looking ahead

As the automotive industry continues to evolve, logistics providers must navigate these dynamic trends, adapting to tariff turmoil, nearshoring, industry restructuring and cost-cutting. The key to success will be adapting to shifting supply chains, embracing technological advancements and staying ahead of regulatory changes. For those who can innovate and respond quickly, the immense challenges of 2025 and beyond could still present significant opportunities for growth and transformation in automotive logistics.