Forecasts for 2025 shows resilience is tested by trade volatility, EV transitions and digital fragmentation

As automotive supply chains navigate rising trade barriers, accelerating electrification and fragmented digital tools, industry leaders explored how logistics must evolve – not just to survive disruption, but to lead through it – during a panel hosted by Automotive Logistics at Transport Logistic 2025.

Automotive Logistics panellists for “Automotive Logistics on the move: Forecast and trends in a disrupted market.” From left to right: Antonio Fondevilla, Maersk; David D’Annunzio, DP World; David Resetar, DSV; Emily Uwemedimo, Automotive Logistics; Richard Logan, Automotive Logistics

Source: Transport Logistic

At this year’s Transport Logistic international trade fair in Munich, the logistics industry was unified not by sector-specific issues but by a shared sense of urgency. Held at Messe München from June 2 to 5, 2025, the event brought together over 2,700 exhibitors and a conference programme centred on recurring themes: geopolitical instability, rising cost pressures, fragmented digital systems and increasingly complex supply chains.

Across sessions – whether focused on air cargo, rail intermodality, chemicals or vehicle logistics – a central question emerged: How can logistics networks remain agile and cost-efficient in a market defined by disruption?

For the automotive sector, disruption is both structural and fast-moving. As part of the official programme, Automotive Logistics hosted a dedicated session where senior executives from DSV, Maersk and DP World joined the content team to discuss the reconfiguration of global automotive supply chains amid escalating market volatility. Titled “Automotive logistics on the move: Forecast and trends in a disrupted market,” the session drew a strong turnout and sparked dynamic discussion.

Advertisement

Speaker line-up

David Resetar, executive vice president, global vertical lead for automotive at DSV: With more than 30 years in commercial and supply chain leadership, including roles at Ford, Visteon and DB Schenker, Resetar currently leads global automotive strategy across all modes at DSV.

David D’Annunzio, global vice president, vertical lead for automotive at DP World: Previously in leadership roles at Neovia, Syncreon and KRE Partners, D’Annunzio now oversees global strategy and implementation for DP World’s automotive logistics division.

Antonio Fondevilla, global head automotive at Maersk: Bringing over 25 years of experience across industrial, consumer and pharma supply chains, Fondevilla leads Maersk’s automotive strategy and business development initiatives worldwide.

Emily Uwemedimo, managing editor at Automotive Logistics and Ultima Media: Leads content strategy and production for the brand, delivering editorial across digital, print and multimedia platforms.

Richard Logan, senior content producer at Automotive Logistics and Ultima Media (session moderator): Producer and presenter responsible for the creation and delivery of original content across the brand’s events and digital platforms.

Market growth under pressure

Forecasts shared during the session pointed to steady but cautious growth for the automotive logistics sector. The North American market is projected to increase from $65 billion in 2025 to $87 billion by 2035, while Europe’s market is expected to grow from €44 billion to €62 billion over the same period, according to Automotive Logistics’ annual regional market reports.

But this forward trajectory is tempered by near-term volatility. In North America, inflation, high interest rates and the aftershocks of tariff announcements earlier this year have created a cautious outlook. In Europe, recovery is still under strain compared to pre-pandemic figures. Carmakers are navigating high vehicle prices, falling incentives and growing competition from Chinese EV imports – while preparing for longer-term regulatory shifts tied to electrification and emissions.

Infrastructure and labour challenges persist. North American rail and port congestion continue to constrain logistics flows, while Europe faces driver shortages and similarly mounting congestion at key finished vehicle ports, where slower sales and onward distribution delays have led to yard overcrowding and rising dwell times. In both regions, the shape of growth is increasingly defined by volatility rather than volume.

Post-event analysis by Transport Logistic reaffirmed the broad nature of these pressures. A survey conducted from February 18 to March 4, 2025, among 1,851 participants – 78% in management roles – identified four dominant concerns:

Cost pressures (77%)

Bureaucratic burdens (58%, among German respondents)

These findings closely mirror – and in some cases intensify – the headwinds facing automotive supply chains. As emphasised by the Automotive Logistics panellists, the sector’s exposure to long-cycle manufacturing, regulatory compliance and ongoing technology transitions adds unique complexity to how these trends unfold in practice.

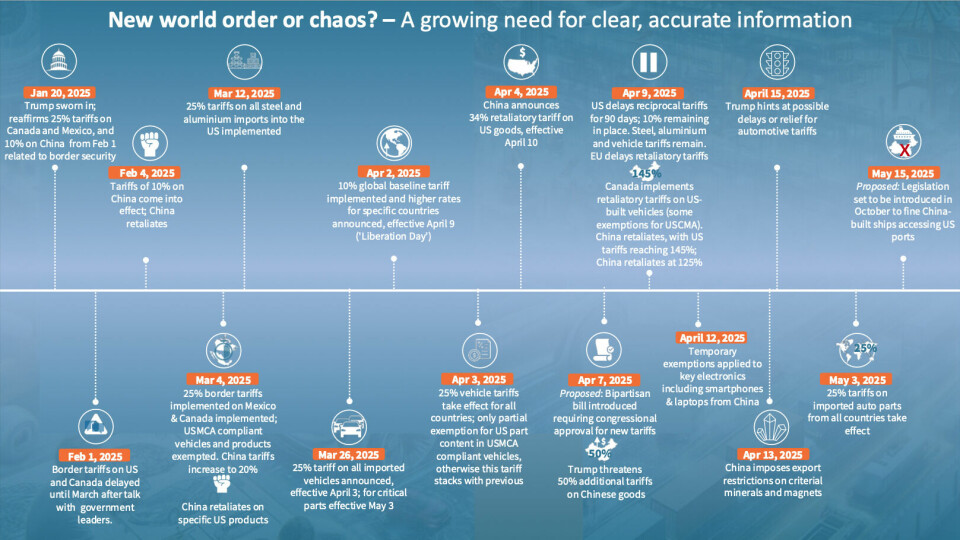

Tariff timeline: From January 20 – May 15

Trade policy volatility

A key visual presented during the session (pictured left) mapped the escalation of US trade policy actions since January 2025. In the immediate aftermath of the 25% import tariff announcements, some automakers – JLR and Stellantis among them – briefly paused to assess their supply strategies before resuming production. Others, such as Hyundai, launched a dedicated tariff task force and shifted some Tucson SUV production from Mexico to Alabama, while Honda redirected its next-generation Civic build from Mexico to Indiana.

Advertisement

No full-scale supply chain shutdowns have occurred, but uncertainty has become the norm. Forward planning is increasingly constrained by shifting policy timelines, and a critical question looms: Who bears the cost burden?

Ford responded by raising prices on select Mexico-built models, while General Motors (GM), projected a $4-5 billion tariff impact this year. On June 11, GM announced a $4 billion investment over the next two years across plants in Michigan, Kansas and Tennessee – part of a broader effort to reshore production of certain combustion-engine models currently built in Mexico. This move is as much a response to tariffs as it is a strategic shift amid softening EV demand and policy changes rolling back EV incentives and infrastructure support originally passed under the Biden administration.

As Automotive Logistics’ Emily Uwemedimo remarked during the session: “OEMs must plan as if tariffs are permanent, even when they may not be.”

Emily Uwemedimo, managing editor, Automotive Logistics and Ultima Media Source: Transport Logistic

Electrification adds complexity, not clarity

Electrification was another major theme of the session from Automotive Logistics – and a clear example of how transformation doesn’t always mean simplification for logistics.

EVs are heavier and often built on more complex modular platforms, affecting how many can be loaded per carrier and how quickly they can be processed. Lithium-ion batteries require specialised packaging, hazardous goods handling and reverse logistics infrastructure to comply with evolving regulatory frameworks.

In Europe, the 2035 internal combustion engine ban has accelerated investment in localised battery production and gigafactory networks. In North America, EV growth remains consumer-led but is increasingly affected by federal policy shifts, including the rollback of incentives earlier this year.

Advertisement

Localisation is a recurring theme for both electrification and a possible solution with the US tariffs in place. But localisation isn’t simple.

Assembly can shift quickly; but upstream inputs like batteries or chips are far harder to reconfigure.

Even as Europe builds out local ecosystems, North American “localisation” often meant nearshoring to Mexico or Canada – until those options, too, came under policy scrutiny.

In both regions, logistics will likely remain international to some degree – because the expertise, labour and parts aren’t always available locally. At the intersection of electrification and tariffs, the core question is: how can partners serve as enablers in navigating and managing that growing complexity?

Digital tools and industry consolidation

The conversation also turned to digitalisation – and the gap between its promise and implementation.

While there are bright spots in automotive digitalisation – such as the growing use of control towers and AI-driven forecasting, exemplified by Renault’s real-time visibility platform and JLR’s risk mitigation tools, as well as their proven value during real crises such as extreme weather events – panellists cautioned that overall adoption remains slow, hindered by legacy systems, fragmented data and cultural resistance within organisations.

The Transport Logistic online survey supports this view: 54% of companies reported some level of AI adoption. Logistics service providers and manufacturers led uptake, especially in administration and customer service, while deployment in production logistics remained limited. Notably, 60% of respondents still cited people as their greatest success factor.

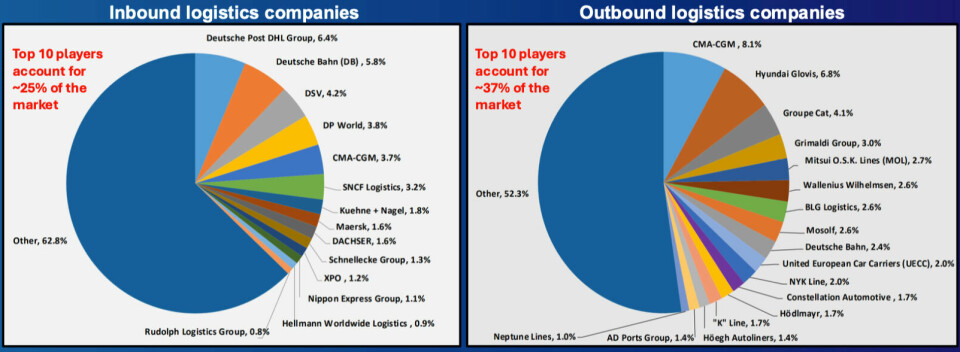

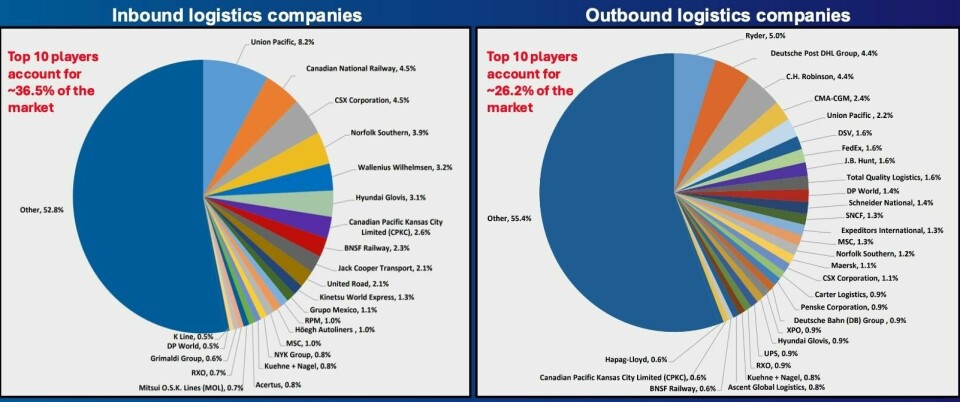

In parallel, consolidation is steadily reshaping the landscape. In both North America and Europe, the logistics landscape for automotive is still highly fragmented.

In Europe, the top ten inbound logistics providers make up just 25% of the market (see Figure 1), and in North America the top 28 inbound players cover just 37% of market share (see Figure 2), according to Automotive Logistics’ annual market reports. That means a crowded playing field, intense competition and thin margins.

European inbound and outbound automotive players Source:European Automotive Logistics Market Report 2025-2035

North American inbound and outbound automotive players Source:North America Automotive Logistics Market Report 2025-2035

Making headlines is DSV’s high-profile takeover of Schenker – but DSV isn’t alone. CMA CGM is expanding into air freight, while Kuehne+Nagel has extended its US footprint by acquiring a 51% stake in intermodal operator IMC, gaining access to 49 rail and port sites and handling roughly 2 million TEUs annually. Similarly, DP World – traditionally known as a port operator – is repositioning itself as a fully integrated logistics orchestrator, investing in inland logistics, digital platforms and even freight forwarding.

So, an open question remains: Will fragmentation give way to consolidation – or collaboration? Early signs suggest a hybrid approach. Some regional 3PLs are already forming alliances, co-investing in digital platforms to extend reach without ceding independence.

Resilience requires more than reaction

The panel concluded with a forward-looking discussion on where strategic value will be created in the coming years. Three priorities emerged:

Operational flexibility, to enable real-time adjustments to disruption;

Clearer digitalisation strategies, focused on measurable outcomes and organisation-wide alignment;

Long-term partnerships, moving beyond transactional arrangements to enable co-creation of resilient supply chains.

As DP World’s David D’Annunzio said on the panel: “The next phase of automotive logistics will be defined by what we choose to build, not what we react to and that’s an exciting opportunity for the sector.”

Live from the show floor

Automotive Logistics also had a strong presence on the exhibition floor. At Stand B2/441, the editorial and intelligence teams engaged with stakeholders across sectors, distributed new reports and magazines, and previewed insights to be featured at upcoming global events in Detroit (September 2025), Munich (November 2025) and Bonn (March 2026).

For further reading and more on upcoming events:

Explore the regional market intelligence reports from Automotive Logistics

Transport Logistic 2025 underscored the extent to which logistics – across sectors – is being reshaped by systemic pressure. For automotive, these pressures are amplified by product-specific regulations, global production footprints and high-cost transformation agendas. But the direction of travel is aligned: towards systems that are integrated, flexible and informed by real-time insight.

As Dr Robert Schönberger, global industry lead for Transport Logistic, put it: “Although the [logistics] sector is under pressure, the mood is improving because industry, trade and service providers are moving closer together.”