Evolution of EVs

Car and truck makers adapt transport planning to increase the use of EVs

The rise of the electric passenger car has a longer history than most suppose but now carmakers are engaged with making inbound and outbound transport modes electric as well, which makes for a greener supply chain altogether.

The electric vehicle (EV) market has been one of the fastest growing sectors of the automotive industry over the last decade. In the US alone, the market share of EVs and hybrids increased from 0.2% of total car sales in 2011 to 4.6% in 2021, according to research from the International Energy Agency (IEA), with similar results being seen across the globe.

EVs have the potential to solve several challenges associated with traditional vehicles driven by an internal combustion engine (ICE), most notably greenhouse gas (GHG) emissions, which has led to the sector receiving strong governmental and regulatory support.

However, contrary to popular belief, electric motors are not a new technology, nor is their use in propelling a vehicle. EVs have been around for almost a century, with the first practical electric car being invented by William Morrison in Des Moines, Iowa in 1890.

Evolution of Electric Vehicles (EVs)

Since the Prius was first introduced at the turn of the millennium, hybrid models have proven to be a popular means of EV adoption among consumers and OEMs. Building on an established ICE framework allows for operations to continue with some familiarity.

Governments around the world have incentivised consumers to choose EVs over ICE vehicles, as well as pushing OEMs to invest in electrification. As an example of the former, the US government under former president Biden introduced the Inflation Reduction Act (IRA) to try and encourage domestic production and wider adoption for EVs – a move that proved to be critical in boosting the demand for EVs in the US, according to analysts at Sucden Financial. However, the continued benefits of the IRA might be coming to an end. Early in his presidency, Donald Trump announced a pause on the IRA and other EV-related tax benefits. Should the proposed Bill pass the Senate, where it is currently being debated, it could end an important lever for EV adoption. Meanwhile, the UK government’s zero emissions vehicle (ZEV) mandates and changes to vehicle excise duties are examples of mechanisms targeting both OEMs and consumers to hopefully boost EV production and demand.

While indicative how much the landscape has grown, both bring with them challenges for the future.

On the commercial vehicle side of the business, major car and truck makers, including Daimler, GM and Hyundai, are committing to the adoption of electric vehicles in their delivery fleets, as are major logistics providers, including DHL, DFDS, FedEx and XPO Logistics. However, increasing commercial EV adoptions requires some rethinking of transport operations and supply chain planning.

Inbound infrastructure

OEMs are increasingly turning to electrified modes of transport for inbound logistics. For example, a joint venture launched last year between Daimler Truck North America (DTNA) and Salem Carriers sees the partners using DTNA’s eCascadia electric trucks (etrucks) to deliver parts between several DNTA manufacturing sites in the US. Similarly, Hyundai is already using its Xcient Class 8 etrucks in day-to-day logistics operations at its dedicated EV mass-production plant in Georgia, US.

While efficiency might play a role in the decision to adopt etrucks in inbound logistics, sustainability is also a significant factor as “long-haul transport accounts for around two-thirds of CO2 emissions in the transport industry,” said Dr Andreas Gorbach, member of the Board of Management responsible for Truck Technology at Daimler Truck. Initially commenting on the Mercedes-Benz eActros 600 etruck going into production at its Wörth, Germany site, he added that the start of production is an important milestone and its customers in decarbonising the supply chain. By reducing emissions during inbound logistics, OEMs can ensure Scope 3 and other emissions-based targets are more easily achieved.

Routes are primarily dictated by available charging infrastructure. As a result, there has been a significant growth in companies offering ‘power-as-a-service’ models that allow for increased freight flexibility, as well as OEM’s pushing for more diverse and effective charging networks. There is still more work that can be done to make charging infrastructure more accessible, as exemplified by recent moves to make power management in charging more intelligent.

Electric haulaway

While the use of EVs for logistics operations can cut emissions in the supply chain, the transport mode brings with it its own logistical challenges. Various OEMs and their logistics partners have recently discussed how they’ve had to catch up with demand and completely redesign inbound and outbound flows to counter one of the key problems in the EV logistics space – insufficient architecture. GM, for example, has had to invest heavily in charging stations along its EV freight routes to solve the problem of batteries dying mid-transit. Speaking at FVL North America 2025, Amy Paulsen, director, finished vehicle logistics at GM, outlined how the automaker had introduced charging stations across its EV FVL network to reduce the amount of “bricked” vehicles in transit. However, while such measures have proved beneficial to smoothing EV transit, Paulsen goes on to state that these measures are only stopgaps, and more significant infrastructure investment is required in high-traffic areas, showing that there is still room for improvement to further streamline EV logistics.

An example of the ‘skateboard’ design, it has the vehicle’s architecture on the base of the chassis.

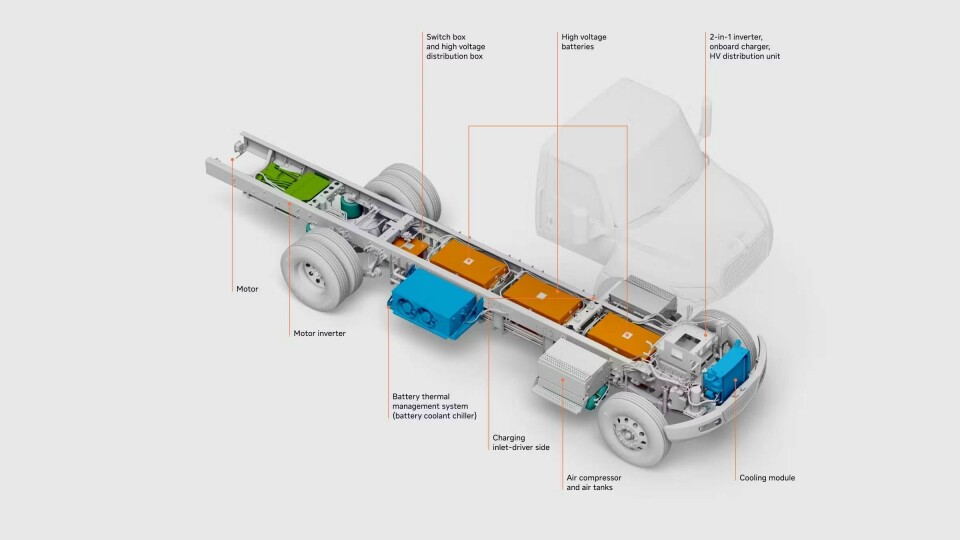

Aside from batteries and charge, another difficulty is the architecture of EVs. The common ‘skateboard’ design of having the battery and powertrain framework on the base of the vehicle can obstruct where trailers traditionally attach to the truck – for an example of this design, see International Motor’s eMV series. This poses difficult situation for OEMs like International, who contend with optimising road haulaway options with heavier and low production vehicles, as described by Tony Stinsa, director of inbound and finished vehicle logistics at International. As such, alternative methods of freight are required but Stinsa also points out that these alternative road methods can be “four to eight times more expensive” and “two to four times” as carbon-intensive compared to traditional ICE driveway operations. Intermodal operations can therefore be beneficial.

However, battery EVs are largely heavier compared to their ICE counterparts, and so legacy car carrier trailers may struggle to efficiently transport EVs at the same scale as ICE models. Charles Franklin, of Glovis America, commented on this problem at earlier this year: “Four out of six auto hauler trailers are incompatible with these vehicles so they’ve got to start planning to change the rail car designs.” However, through increased communication and collaboration, OEMs and their LSPs are increasingly adapting and streamlining processes to ensure the movement of finished EVs remains effective, with Stinsa pointing to the “nimbleness and adaptability” of the sector as being key.

A local boom in batteries

Battery suppliers have also been investing heavily in manufacturing facilities. For example, CATL recently announced plans to invest in a new battery gigafactory, raising a record-breaking $4 billion on the Hong Kong stock exchange to do so. The increase in the number and size of these battery facilities has been instrumental in reducing battery production costs and improving supply, facilitating the scale-up required to meet increased demand. This has also led to several different generations and formats of battery being available for OEMs to use, and has encouraged innovation for next-gen solid state batteries.

The rise in localised production will also have a significant impact on EV logistics going forward. There has been a marked rise in nearshoring over the last few years, with OEMs increasingly creating regional production hubs, partly as a response to the disruption caused by both the Covid-19 pandemic and semiconductor shortages. However, since the US-China trade war earlier this year led to an associated rise in protectionism, interest in creating regional hubs has boomed. While production hubs for ICE vehicles are being built, EV and battery hubs are being prioritised. Ford, for example, has relocated battery production to the US. Meanwhile, Mazda has made plans to source locally produced batteries for two of its Japanese plants to facilitate full domestic assembly for several of its EV model lines. That is something that Audi has already achieved with for its Q7 SUV in Malaysia. Increased local production can make the EV market more resilient by minimising reliance on international inbound flows, meaning OEMs have less risk of disruption to EV production. Localisation also helps lower the overall price of EVs through lower freight costs, facilitating wider adoption of models.

Cleaning the code

Vehicle software is another area to watch within the EV logistics space, which is especially pertinent given that autonomous EVs are on the horizon, including those used in logistics. Speaking at ALSC Mexico last year, Paulo Monteiro, head of logistics for VW Group of America Chattanooga Operations, explained that modern EVs can have at least 100m lines of complex code. The risks associated with such a large amount of coding range from script errors leading to parts failing to more extreme cases of hacking and digital vandalism. Monteiro also pointed out that all the different modules that form an EV must be running the same code and working effectively before the production process ends. Once the vehicles are shipped, it may be too late to change anything (though over-the-air software and firmware updates for EVs are possible). As such, logistics teams need to be involved in production discussions as early as possible so that coding and development can be done with logistics parameters in mind.

Outside of the vehicles themselves, software and digital tools have proven beneficial in EV logistics, especially when dealing with global supply chains. Inform’s transport and yard management software proved “key” to Vinfast’s first shipment of VF8 SUVs to the US from Vietnam, according to Le Thi Thu Thuy, vice-chairwoman of Vingroup and vice-chairwoman of VinFast. Such software can allow for real-time monitoring of EVs in transit, with one benefit being updates on battery health and charge. This is another means of reducing the risks associated with transporting batteries, such as fires, as logistics teams can identify at-risk vehicles and intercept. End-to-end transparency during shipments can also be used to identify bottlenecks and disruptions, facilitating faster response times to issues and helping “achieve faster, more efficient and sustainable vehicle deliveries”.

Software awareness is especially important given the increased automation involved in the manufacturing of EVs, and EVs themselves. For the former, Volkswagen Group China, for example, has taken steps to increase the amount of automation in its Chinese EV plants to boost efficiency and competitiveness, while another arm of the group has been developing autonomous mobile robots that deliver charging apparatus to vehicles. For the latter, DTNA has recently unveiled a new autonomous version of the eCascadia, with it currently being tested in hub-to-hub freight runs. The company hopes for future synergies encouraged by tech advancements, where “charging infrastructure and autonomous freight hubs could be combined to charge and load simultaneously”. Despite the associated concerns, these examples demonstrate the scope of innovation within the EV logistics space. It is on the cusp of becoming “an age of intelligently connected vehicles”, according to VW Group, which could be revolutionary for future logistic flows.