Tariff timeline: US imposes 10-12.5% tariffs on 60 economies and 50% tariff on Canada

Will 2026 see tariffs continue to reshape global trade? Automotive Logistics tracks the escalation month by month in this timeline overview, with the latest developments as Trump imposes new tariffs on trading partners.

By the start of 2025, it was clear that tariffs would form the backbone of Donald Trump’s second-term agenda. Since then, there have been so many delays, tariff changes and trade wars and deals that it's been hard to keep track – so we've done it for you.

The timeline below charts the most significant tariff decisions since Trump's inauguration in 2025 – month by month – as they reshaped the rules of global automotive commerce.

Scroll through the slides to view Automotive Logistics' Tariff Timeline

Want more tariff information?

We've got in-depth coverage of all the tariffs affecting automotive logistics and supply chain.

For a comprehensive and continually updated timeline of all tariff and trade changes, read more below.

Nations including the UK, China and EU member states will be subject to these new tariffs, effective immediately.

The new tariffs, imposed under Section 301 of the Trade Act of 1974, have replaced the 10% temporary import surcharge imposed under Section 122 of the same act – with the temporary tariff expiring on the same day this new tariff was introduced due to a 150-day limit on such levies.

Canada faces new 50% tariffs on wide range of US imports

In the first known use of Section 338 of the 1930 Tariff Act, US president Donald Trump has signed three proclamations to impose additional 50% tariffs on certain goods from Canada in response to "Canada’s discriminatory treatment of American products".

According to the White House, this move is designed to "level the playing field for crucial American exports – cars, alcohol, and dairy". The Trump Administration has claimed that Canada's tariffs on US cars compel US automakers to invest in Canadian manufacturing rather than US production and led to a 22% decrease in US motor vehicles imported to Canada from April 2025 to March 2026, compared with the same period a year earlier.

The tariffs apply to $20 billion worth of goods ranging from food and beverages to furniture; they are set to come into effect on 19 August.

US decides not to renew USMCA

Having declined to renew the US-Mexico-Canada Agreement (USMCA) on July 1, the US will now have annual reviews with Canada and America on trade agreements over the next decade, creating more uncertainty for the automotive sector in North America. If at any point the three countries reach a consensus through the annual reviews, the USMCA’s term will be reset for 16 years from that point.

The agreement remains in force and current USMCA trading rules continue to apply. The decision means only that the three governments did not agree to extend the agreement for another 16 years at the first six-year review. Instead, the USMCA now enters an annual review process that could continue until its scheduled expiry in 2036 unless all three countries agree to extend it earlier.

US Treasury issues $49.2 billion in IEEPA tariff refunds

In the month of June, the US Treasury is confirmed to have refunded $49.2 billion in illegal tariffs after the Supreme Court ruled

that the International Emergency Economic Powers Act (IEEPA) "does not authorise the president to impose tariffs to deal with the declared drug trafficking and trade deficit emergencies".

These refunds pushed the June federal budget deficit to $120 billion, compared with the $27 billion surplus reported in June 2025.

The US Treasury reported gross customs duty collections of $23.6 billion for the month, but the $49.2 billion paid in refunds resulted in a net outflow of $25.6 billion for June.

Advertisement

May 2026

Trump threatens to raise tariffs on EU vehicle imports to the US to 25% unless vehicles are produced in the US

On May 1, US president Donald Trump threatened to increase tariffs on EU cars and trucks imported to the US from 15% to 25%, accusing the trade bloc of failing to comply with the EU-US trade deal.

President of the European Commission Ursula von der Leyen responded to Trump’s threat, saying: "A deal is a deal… we're prepared for every scenario.”

Trump had previously struck a deal with the EU last year to reduce tariffs to 15%, while the EU agreed to drop its tariffs on some US goods to zero. However, the EU delayed ratifying the deal when Trump threatened to take over Greenland.

EU diplomats, according to Reuters, have said that EU countries are now pushing to quickly implement the trade deal to avoid the threatened tariffs on vehicles.

European Parliament and Council representatives resumed negotiations on May 6 to lower duties on US imports.

Trump and Xi Jinping meet for talks in China

During meetings in Beijing, US and Chinese officials discussed a framework for reciprocal tariff reductions on “non-sensitive goods” worth up to $30 billion.

The talks reportedly centred predominantly around agricultural and industrial trade, while leaving existing restrictions on technologies sensitive to national security in place; no automotive tariff changes were announced.

Bipartisan lawmakers in the US introduce bill to toughen US ban on Chinese vehicles

Two members of the US House of Representatives introduced a bill on May 11 aimed at toughening the US government’s ban on Chinese automakers entering the US market.

The legislation would ban vehicles designed in China if they had advanced connectivity as well as vehicle software.

April 2026

Advertisement

US Customs and Border Protection launches portal for IEEPA tariff refunds

On April 20, 2026, US Customs and Border Protection (CBP) has developed the Consolidated Administration and Processing of Entries (CAPE) functionality within the Automated Commercial Environment (ACE) portal to streamline the submission and processing of refund requests for duties imposed under the International Emergency Economic Powers Act (IEEPA), which was ruled unlawful by the US Supreme Court in February 2026. More than $160 billion is expected to be refunded to around 330,000 importers. However, refunds are only available to those importers that paid the duties, leaving it up to the importer whether or not to refund consumers who paid higher prices as a result of the tariffs.

White House adjusts Section 232 tariffs on steel, aluminium and copper

On April 2, 2026, the White House issued a proclamation overhauling Section 232 tariffs on steel, aluminum and copper imports by introducing a tiered system of 10-50% tariffs applied to the full value of imported products, rather than just the metal content. The system has been designed to target goods made largely of these metals with higher rates, while offering reduced rates for products using US-sourced metals, preferential rates for imports from the UK and exemptions for some low-metal-content or excluded goods.

Trump administration to proceed with Biden-era ban on Chinese vehicles

US trade representative Jamieson Greer states that the Trump administration has no plans to roll back Biden-era restrictions on Chinese vehicle software and hardware, signalling continuity in US automotive trade policy towards China.

Impact of tariffs on volumes at US ports in 2025 becomes clear

The total number of vehicles handled at the Port of Brunswick dropped by 7.1% year-on-year in 2025, with the Georgia Ports Authority (GPA) saying that automakers pausing shipments and temporarily closing factories in the summer of 2025 had across vehicle ports in the US and abroad.

Likewise, vehicle handling volumes at the Port of Baltimore dropped by 2.8% in 2025, with a spokesperson for the Maryland Port Administration (MPA) saying: "The inconsistent, almost day-to-day changes of [the tariffs] have been hard on our industry. Auto manufacturers have been wondering should they pay the tariffs or change their business models and produce more cars in the US. As a result, our auto volumes were impacted.”

Although US vehicle ports were undoubtedly affected by the imposition of US tariffs on vehicle imports and US Trade Administration port fees in 2025, the Jacksonville Port Authority (Jaxport) said that the impact of the tariffs had only a modest impact on volumes at the Port of Jacksonville.

March 2026

US Trade Representative launches Section 301 forced labour investigations into 60 countries

On March 12, the US Trade Representative (USTR) initiated investigations into 60 of the US' largest trading partners around the world to determine whether these economies effectively enforce a ban on the import of goods produced with forced labour. Canada, Mexico, China, Japan, the UK and the EU are amongst the nations that may face additional tariff measures depending on the outcome of these Section 301 investigations, with the USTR is set to hold hearings in connection with these investigations on April 28.

US Customs and Border Protection developing new process for tariff refunds

On March 6, Brandon Lord, executive director of US Customs and Border Protection’s trade policy and programmes directorate, has said it is working on a new system to simplify the process for IEEPA-related tariff refunds. He said this system should be ready within 45 days and require "minimal submission from importers".

Japan urges US not to apply 15% tariff to Japanese goods

Japan's minister of economy, trade and industry, Ryosei Akazawa, has raised concerns with US commerce secretary Howard Lutnick that the new global tariff structure could disadvantage Japanese exporters, asking that Japan's treatment under the new tariff rules would not become less favourable than what was agreed between the two countries in their 2025 trade deal.

Data shows drop in value of UK car exports to the US in 2025

The value of UK car exports to the US fell by 28.1% in 2025 to £7.5 billion, according to an analysis of trade figures by business advisory and chartered accountancy firm Lubbock Fine.

February 2026

US Supreme Court strikes down Trump's global tariffs

After the ruling on the legality of US president Donald Trump's 'Liberation Day' global tariff was pushed back in January, the US Supreme Court's much-anticipated decision came on February 20, with it finding that the International Emergency Economic Powers Act (IEEPA) "does not authorise the president to impose tariffs to deal with the declared drug trafficking and trade deficit emergencies". The Supreme Court justices were divided 6-3 in favour of the tariffs being unauthorised under the IEEPA. Brett Kavanaugh, associate justice of the Supreme Court of the United States, said he firmly disagreed with the decision but noted that "the decision might not substantially constrain a president’s ability to order tariffs going forward" provided the tariffs are justified by another statute such as the Trade Expansion Act of 1962, the Trade Act of 1974 and the Tariff Act of 1930. He explained that the interim effects of the court’s decision could be "substantial" and the US "may be required to refund billions of dollars to importers who paid the IEEPA tariffs, even though some importers may have already passed on costs to consumers or others".

With the tariffs imposed under the IEEPA immediately struck down, Trump signed a proclamation imposing a new "temporary import surcharge" of 10% – as permitted by Section 122 of the Trade Act of 1974. However, several goods have been exempted from the new import duty "because of the needs of the US economy or in order to ensure the duty more effectively addresses the fundamental international payments problems facing the United States". Amongst these exempt goods are: passenger vehicles; certain light trucks; certain medium- and heavy-duty vehicles; buses; and certain parts of passenger vehicles, light trucks, heavy-duty vehicles and buses.

Trump later claimed on social media that this 10% global tariff would be increased to the maximum rate of 15%, although that increase is yet to be confirmed by official White House documentation, and the tariff took effect at the 10% rate.

Logistics company FedEx has filed a lawsuit against US Customs and Border Protection for a full refund on the illegal IEEPA-related tariffs that it paid.

Trump threatens to block Windsor-Detroit bridge opening

On February 9, Trump claimed he intends to block the opening of the Gordie Howe International Bridge connecting the top two regions for auto production in North America – Detroit, Michigan and Windsor, Ontario. In a post on social media, he falsely claimed Canada owned both sides of the bridge and demanded negotiations take place immediately to ensure the US is "fully compensated". Canadian prime minister Mark Carney later “explained” to Trump during a phone call that the crossing is jointly owned by the country of Canada and the US state of Michigan, describing the call as “a positive interaction” and indicating that the situation will be resolved.

US and Mexico agree to begin USMCA discussions:

US ambassador Jamieson Greer and Mexican secretary of economy Marcelo Ebrard agreed to begin formal discussions on possible structural and strategic reforms to the US-Mexico-Canada agreement (USMCA), with a joint review including all parties to be launched before July 1 this year. According to the US Trade Representative (USTR), they agreed to discuss matters such as stronger rules of origin for key industrial goods, enhanced collaboration on critical minerals and increased external trade policy alignment.

According to reports in Mexico, letters have been sent to the USTR by VW, Nissan, GM and Toyota, supporting the trade pact but warning that its automotive rules of origin are increasing production costs across North America and could end up leading to higher vehicle prices.

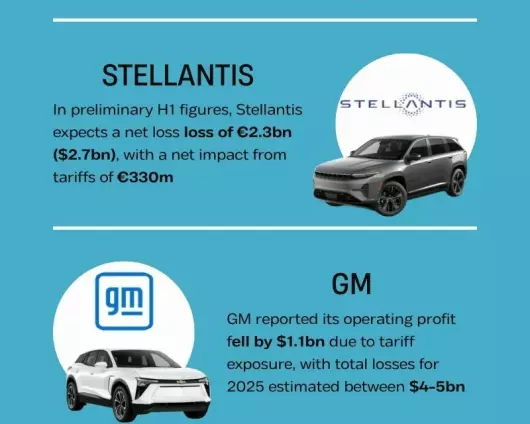

Ford takes $2 billion tariff hit in 2025:

During a February 10 earnings call, Ford president and CEO Jim Farley revealed that Ford generated $6.8 billion of adjusted earnings before interest and taxes (EBIT) for the full year of 2025, noting a net tariff impact of $2 billion.

January 2026

EU puts trade deal with US on pause 'until further notice'

The EU has put its trade deal with the US on pause. The chair of the European parliament’s trade committee Bernd Lange said: “Our negotiating team just decided to suspend work […] on the legal implementation of Turnberry deal. Our sovereignty and territorial integrity are at stake. Business as usual impossible.”

US Supreme Court delays decision on tariff legality:

The US Supreme Court was set to rule on the legality of Trump's tariffs on January 14, but did not issue a ruling. The body - as is typical - has not announced a new date for the decision. If the court rules that the tariffs are illegal, it could mean an influx of companies attempting to claim refunds. Trump said it would be difficult to reverse the tariffs, stating that “it would take many years to figure out what number we are talking about and even, who, when, and where, to pay”. In this case, supply chains that have shifted in anticipation of tariffs or to try to mitigate tariffs may face further upheaval.

New tariffs and trade deals:

Trump announced plans to put additional 25% tariffs on goods from countries that do business with Iran

US tariffs on aluminium imports (now up to 50%) and global supply shortages have sent US aluminium prices to record levels, with direct implications for automotive supply chains, where aluminium is critical for body panels, structural components and EV parts, increasing material costs and logistics expenses

New tariffs have come into effect in Mexico as of January 1, 2026 applying to all countries it does not currently have a Free Trade Agreement (FTA) with, including China, Brazil and India. Passenger cars, auto parts and raw materials are amongst the goods that are subject to these new duties

China and Canada have agreed a trade deal which will allow up to 49,000 Chinese EVs into the Canadian market at the most-favoured-nation (MFN) tariff rate of 6.1%, exempt from the 100% surtax introduced on Chinese-made EVs in October 2024

A “historic” US-Taiwan trade deal has been signed, which will see Taiwanese semiconductor and technology companies invest in manufacturing on US soil in return for a reduction in the tariffs imposed by the US on imports from Taiwan

The US has introduced a new 25% tariff on certain advanced computing chips, with broader tariffs on semiconductors set to be introduced “at a rate of duty that is significant" once the US has concluded negotiations over semiconductors

Trump has also threatened to impose a 100% tariff on all imports from Canada if it “makes a deal with China”; Canadian prime minister Mark Carney has asserted that Canada has no plans for a Free Trade Agreement with China and that its recent agreement that saw tariff exemptions for Chinese EVs does not breach Canada's obligations under the US-Mexico-Canada Agreement (USMCA)

December 2025

US claims automotive tariffs bring in more than $26 billion in the six months from April to October 2025:

The US Customs and Border Protection (CBP) collected $216.7 billion in revenue from all imported goods in 2025

Of this, imports of finished vehicles accounted for $18.33 billion, while imports of automotive parts accounted for $7.61 billion

Other section 232 tariffs brought in $4.83 billion from steel imports, $2.96 billion from aluminium imports and $514m from copper imports

UK and South Korea sign trade agreement:

Deal allows greater export of finished vehicles from UK, lowering the number of parts in a vehicle that must be British or from the EU to quality for zero tariffs from January

Agreement sees rules of origin requirements drop from 55% to 25%

November 2025

Imports to Port of Los Angeles down:

Imports to the US' busiest seaport decrease 11.5% volume year-on-year in November

Imports to all US ports fall 7.8% year-on-year in November

Switzerland and the US reach a trade deal on tariffs:

The US agrees to cap tariffs on Swiss goods at 15%, down from the 30–39% range that was imposed earlier in 2025

While unlikely to majorly affect finished vehicle exports, since the country doesn't have any large production base, it's likely to affect the export of automotive parts to the US. According to Swiss trade data, exports of automotive parts from Switzerland to the US in 2023 amounted to about $7.78m

October 2025

US increases Canada tariff:

Tariff increase of 10% announced on imports from Canada

Tariffs impact VW Group's bottom line:

VW Group reported a 33% decline in operating result for H1 2025 when compared with H1 2024, claiming this was primarily due to high costs from increased US import tariffs; it calculated the impact of these tariffs at €1.3 billion ($1.5 billion)

During Trump's trip to Asia, the US signed technology prosperity deals with both Japan and South Korea; the deals formalise plans for future collaboration in areas such as artificial intelligence, 6G technologies and fusion energy.

Expanded Section 232 tariffs on medium and heavy-duty vehicles and parts:

Carmakers spread the cost of tariffs but prices set to rise:

At ALSC Global, analysts say that costs are being absorbed by OEMs through a range of mitigating strategies as they wait and see how the tariff debacle will play out.

Port congestion, competition pressures loom as Mexico set to increase tariffs on Chinese vehicle imports:

Steel, aluminium and broader material tariffs remain elevated:

The US continues to impose 50% tariffs on many steel and aluminium imports — for example, parts used in automotive body-shop (e.g., chassis components, axles, mounts) now face the 50% rate instead of 25–27.5%.

While vehicle/parts tariff relief for EU origin is conditioned on EU legislation, full implementation timing remains unclear.

With Japan, a deal was reached whereby Japanese automotive exports to the US face a 15% tariff (reduced from an earlier contemplated higher level). Steel and aluminium tariffs remain separate.

September 2025

OEMs react further to deepening impacts of tariffs:

Nissan announced that it will drop the 2026 Ariya electric SUV from its US. lineup. One of the reasons cited is the 15% tariff imposed on Japanese-built EVs under the US–Japan trade framework.

Hyundai is expanding its US output, boosting capacity in Georgia, and has adjusted its operating profit margin targets downward to account for tariff pressures. The company is also accelerating its plans for its hybrid and EV portfolio in North America.

Volvo Cars is accelerating US-based production, committing to produce a new hybrid model in South Carolina by 2030. This is clearly a strategy to reduce exposure to import tariffs.

Continued uncertainty and what’s still in flux:

The Supreme Court decision is now the center of attention. Because the appellate ruling invalidating much of the reciprocal tariff scheme is stayed through mid-October pending appeal, businesses are in a holding pattern. OEMs and suppliers must plan under tariffs that may be reversed (or significantly modified) if the court rules against them.

For parts of the tariff regime not covered by the August ruling, or example, Section 232 tariffs (steel, aluminium) and other trade-remedy or security-based tariffs, there has so far been no court decision invalidating them. They continue to impose elevated costs and uncertainty for automotive OEMs and suppliers.

Countries that negotiated deals (Japan, EU) or that had exemptions and special arrangements now face questions about how stable those deals will be if the legal basis for many tariffs is overturned. Also, automotive companies must assess whether to push for refunds or duty protests for tariffs paid, depending on legal outcome.

Product lineups are being adjusted. EV models or lower-volume vehicles especially are at risk if tariff costs can’t be absorbed. As with Nissan/Ariya, automakers may choose to limit or delay models, shift imports, or reallocate resources to models built domestically or under favourable trade agreements.

Customs, classification, and parts supply chain complexity increase. When parts or assemblies cross borders or involve imported content, correctly classifying them under HTS codes, knowing which piece of the tariff regime applies (IEEPA/Section 232/trade-deal/exemption) can make big cost differences. Demand for trade compliance expertise is up.

August 2025

US extends steel and aluminium tariffs:

The US extends the scope of 50% tariffs on steel and aluminium on August 19, adding 400 additional items to the levy. The expanded scope includes car parts such as chassis components, axles, steel wiring, brackets and mounts, and parts of heavy vehicles.

This means these products, which are not listed under the car parts tariff of 25% to 27.5%, will be taxed at a higher rate of 50%. OEMs will need to review codes carefully to determine which parts will be tariffed at which rate.

The new scope also targets product codes for derivatives and products made from the materials, including the likes of paints and sprays, which are often used in the automotive supply chain, and stamped components.

Truck trailers are also added to the list, further complicating automotive logistics.

US-EU trade deal:

The EU paused planned retaliatory tariffs on US exports (including automobiles), covering €93 billion ($101 billion) in goods. The suspension is expected to last six months, pending the outcome of ongoing trade talks.

The pause is linked to the US-EU framework deal from late July, which aims to de-escalate trade tensions and foster cooperation. Under the deal, the US agreed to cap vehicle and parts tariffs at 15%, down from around 27.5%, while the EU committed to boosting investment in key US sectors such as clean energy, semiconductors and automotive manufacturing.

The EU tabled legislation to cut tariffs on US products, aiming to unlock the US commitment to lower auto tariffs from 27.5% to 15%, retroactive to August 1.

German car lobby groups (VDA, VDIK) publicly urged Washington to move “swiftly” in reducing tariffs on EU car imports in response.

US goods imports see steep drop:

The US Commerce Department indicates the US trade deficit in goods fell roughly 16%, declining from $71.7 billion in May to $60.2 billion in June.

A significant contributor to the decline was a drop in automotive imports, with vehicles, parts and engines falling by $1.3 billion.

Mazda projects a $319 million operating loss for fiscal year 2026 due to US tariffs – assumed at 15% on Japanese imports and 25% on vehicles exported from Mexico.

New tariffs across many countries set to take effect August 7, following a July 31 executive order establishing country-specific 'reciprocal' rates – including a 10% baseline tariff for most nations, higher rates of 15% for trade-deficit countries, and tariffs ranging from 25% to 41% for countries like India, Canada, Brazil, Switzerland and Iraq. The White House has stated these rates are "pretty much set," with limited room for negotiation, and special provisions include a 40% penalty on transshipped goods and exemptions for imports already on route, provided they arrive before October 5.

US Court of Appeals rules 'reciprocal' tariffs illegal, stating that the actions taken by the president to implement the duties were “unbounded in scope, amount and duration”. Tariffs will remain in place until October 14, giving the US administration time to appeal to the Supreme Court before the ruling takes effect. The legal case has been fast-tracked: the Supreme Court has agreed to hear the appeal, with arguments scheduled for early November 2025.

US-China truce:

On August 11, the US and China extended their tariff truce until November 10, holding tariff caps at 30% on Chinese imports and 10% on US imports.

As a result, India plans to diversity its export markets, focusing on regions like the UK, Australia, UAE, South-East Asia and the EU.

New rate does not apply to vehicle imports or designated automotive parts imports, but could still effect other components used in the automotive supply chain, such as castings, forgings, tyres, wire harnesses and metal parts, of which India is a major exporter to the US.

On July 31, Trump announced an agreement reducing auto tariffs on South Korean goods from the threatened 25% to 15%. The deal includes $350 billion investment in US projects such as shipbuilding, chips and batteries.

On August 1, the Asian nation's trade minister said there is no written agreement yet on a trade deal between South Korea and the US.

Final push for deals with Canada, Mexico, India, Brazil and others before August 1.

Deals are made with the likes of Japan and Vietnam. On July 22-23, the US and Japan finalised a bilateral trade agreement that reduces reciprocal tariffs on Japanese vehicles and auto parts from 27.5% (including a 2.5% baseline and an additional 25% auto-specific levy) to a flat 15%. Vietnam, meanwhile, agreed to a 20% tariff on its exports to the US, avoiding the 46% “reciprocal” duty threatened by president Trump on “Liberation Day.”

This impacts both finished auto parts and raw materials, increasing cost pressures on domestic OEMs and tier one-three suppliers.

Automotive sectors reliant on imported flat-rolled steel, castings or extrusions are particularly affected (such as: EV platforms, body-in-white structures, chassis, and control arms).

Rare earth and US-China trade framework:

China and the US make some progress, with Trump claiming a "done deal" on a trade framework which allegedly includes magnets and rare earth minerals supplied by China, but details are not yet confirmed.

As it stands, the US will enforce 55% tariffs on China and 10% for the US. It is understood that the 55% tariffs on China consist of a 10% ‘reciprocal’ base tariff, 20% International Emergency Economic Powers Act or IEEPA tariff, and an existing 25% tariff on imports from China. China has also offered expedited export approvals for civilian uses of rare earth minerals.

California emissions rules:

The US administration blocks the state of California and EPA from enforcing stricter vehicle emissions standards.

The Alliance for Automotive Innovation supports the move, citing regulatory clarity and uniformity.

Potentially affects EV adoption timelines and OEM product planning for low-emission zones.

Orders the administration to suspend them within 10 days.

Raises legal doubts over ongoing negotiations and executive tariff enforcement power.

US-UK finalise trade deal:

The US and the UK reach a trade deal, including reducing US vehicle import tariffs for the UK from the additional 25% levy to a maximum of 10%, with a 100,000-vehicle annual cap. Tariffs on British steel and aluminium imports to the US – which had also been levied at 25% – have also been cut to 0%, according to the UK government.

Part tariff implementation:

As of May 3, the US enforces the 25% tariff on all imported auto parts, originally announced on “Liberation Day”.

Affects a wide range of components including engines, powertrains, electrical modules, HVAC units and safety systems.

Critical for aftermarket, repair and global platform assembly models.

Stacking tariff reform:

Trump amends rules to prevent stacking of multiple tariffs, specifically addressing cases where steel and aluminium tariffs (at 50%) could have compounded vehicle or part tariffs. It is also clarified that only one applicable tariff per item will be applied where overlapping categories exist.

IEEPA tariffs rate clarification:

New guidance confirms the maximum burden is reduced to 27.5%, comprising: 25% vehicle import tariff and 2.5% pre-existing non-USMCA duty.

Initial fears that IEEPA tariffs (for non-USMCA compliance) could stack up to 52.5% are dialled back.

Still a major cost for OEMs with offshore production, especially luxury/import-heavy brands.

Scheme is designed to incentivise local sourcing and protect compliant OEMs from stacking costs. For example, if an OEM assembles vehicles in the US (with vehicles having 85% US content, or USMCA compliant content), they can apply to offset up to3.75% of the tariffs on parts for one year, retroactive to April 3. This offset rate would then drop to 2.5% in the second year, before being removed completely 25% tariff on all imported vehicles.

April 2025, 'Liberation Day'

EU rejects US deal:

Trump rejects the EU's "zero-for-zero" tariff proposal.

Trump threatens 50% tariffs on China in response to Beijing’s threat of a 34% tariff on US imports to China. China’s government says it will “fight to the end” if trade war continues to escalate.

Trump hikes tariffs on Chinese imports up to 104%, and China responds with tariffs on US imports of 84%.

Individual reciprocal tariffs are paused by the US for 90 days. Base global tariffs of 10% are on, while Trump raises tariffs on Chinese imports to 145%. 25% tariffs on steel and aluminium imports, and 25% tariffs on vehicle imports are upheld, as are the planned 25% tariffs on vehicle parts, due to be applied next month.

Trump announces individualised reciprocal tariffs against countries with large US trade deficits, including Germany, China and Japan.

Tariffs of 20–50% set to begin on April 9, but are paused for 90 days after a legal challenge and backlash from allies.

Global tariff baseline implemented:

A 10% universal tariff on all imports to the US takes effect on April 5.

Exceptions include: vehicles, auto parts, and steel/aluminium already subject to separate tariffs are exempt from this new global tariff.

This baseline measure adds pressure to countries without bilateral trade agreements.

"Liberation day" tariffs announced:

Dubbed “Liberation Day” by the administration, president Trump launches a 25% tariff on all vehicle imports to the US, effective immediately. A 25% tariff on imported vehicle parts is also confirmed for implementation on May 3.

The list of parts that will be affected includes engines, powertrains and electrical components.

Temporary exemption granted for USMCA-compliant vehicles, which only pay the tariff on non-compliant content (25%).

March 2025

US imposes major automotive tariffs:

US tariffs enforces 25% tariffs on imports from Canada and Mexico, and 20% on imports from China (March 4).

There is a surge of vessel movements as OEMs scramble to reroute ships bound for the US from Asia and Europe. Meanwhile, OEMs look to diversify manufacturing as quickly as possible.

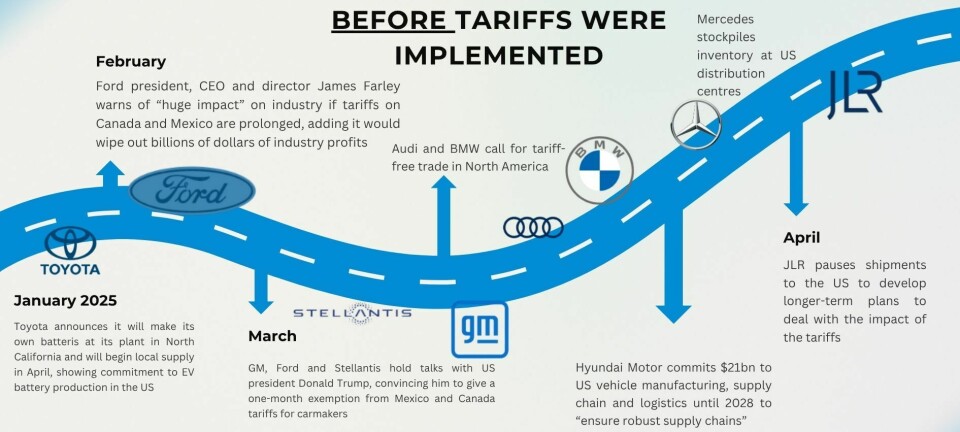

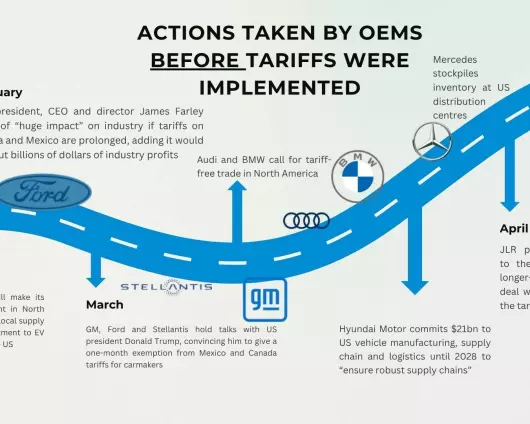

Toyota announces it will make its own batteries at its plant in North Carolina and will begin local supply in April, showing commitment to EV battery production in the US despite Trump’s announcement about pausing IRA funding.

The plant is expected to supply both Toyota and Lexus EVs and may help Toyota mitigate future tariff exposure by localising key value chains.

Threatens Canada with 25% auto part and metal tariffs:

Highlights include: supply chain cost volatility, higher vehicle prices, delays to EV rollout and investment.

US-Panama tensions over canal control:

While tensions between the US and Panama ramp up further over the canal, as the US secretary of state accuses the Panama Canal of being controlled by the Chinese Communist Party.

The canal – critical for East Asia-to-US East Coast vehicle flows – is now caught in geopolitical crossfire, raising alarms in automotive logistics circles.

Auto carriers and parts suppliers reliant on canal access face potential delays or cost surges.

Trump vows global reciprocal tariffs:

Rather than pull back on tariff threats, Trump aims to impose reciprocal tariffs around the world, triggering potential trade wars that could impact automotive logistics networks and dampen investment. He says he will reveal more about his promised tariffs of 25% on vehicles on April 2.

The pause is immediate, affect OEM eligibility for consumer EV tax credits and federal funding for battery production and charging infrastructure.

In the short-term, the move could help balance EV supply and demand, but is likely to reduce investment in EV manufacturing and logistics in the US.

Automakers like Ford, Hyundai, GM and Volkswagen, which had made strategic bets on IRA-backed funding, are now forced to reassess future expansion plans.

In response to President-elect Trump’s announcement of a proposed 25% tariff on all imports to the US – including those from key allies – Mexico’s Ministry of Economy voiced strong concern, calling it a direct threat to the North American automotive supply chain. Canada’s trade minister similarly warned that such a move could trigger a mutually damaging trade war.

Both nations begin preparing diplomatic and economic countermeasures, including WTO consultations, auto industry stakeholder briefings and early coordination with OEMs and cross-border suppliers.

Industry reaction begins quietly:

While public reaction from OEMs is muted in December (pending inauguration), lobbying ramps up behind the scenes. Industry groups like the Alliance for Automotive Innovation and Original Equipment Suppliers Association (OESA) begin preparing legal and policy response frameworks.

Tesla pauses its plans to build a new gigafactory in Mexico until after the US election. The OEM had first announced plans for the gigafactory near Monterrey in Nuevo Leon in March 2023 and it was originally expected to be operating by the first quarter of 2025. In a financial update, the carmaker said uncertainty surrounding the tariffs would make it impractical to invest heavily in the plant, but Mexican government officials have stated that the OEM has received $135m in incentives to build the factory.