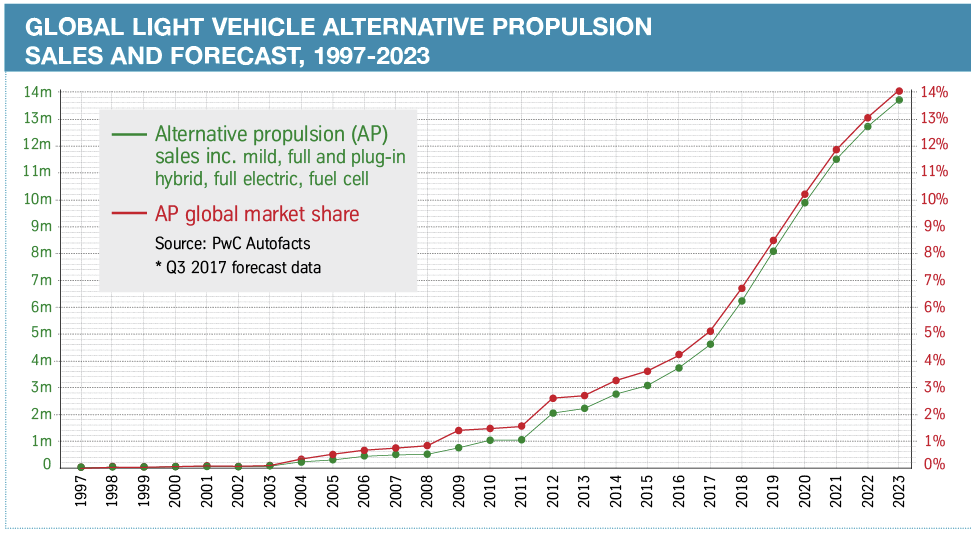

The last two decades have seen the emergence of the alternative propulsion vehicle market from almost nothing. According to PwC Autofacts data, sales in 1997 across all hybrid and electric vehicles numbered about 6,000 vehicles. This year, the number is expected to pass 4.6m. But much faster growth is expected in future and sales could approach 14m units by 2023.

Further regulatory forces – including the phasing out or even outright ban of internal combustion engine vehicles in some markets – could encourage substantial transformation over the next 20 years, all of which will have significant impacts for the automotive supply chain and logistics services. Supply chain managers today are already looking at how production and logistics systems must evolve to support the transition to EV batteries and lithium-ion materials.

In the wake of the ongoing success of relatively new entrants like Tesla, a growing number of incumbents are now vying for a slice of the rising EV market; companies like Volkswagen, Volvo Cars and BMW have already outlined ambitious plans for the commercialisation of electrically powered models, while companies already active in the space, like Renault Nissan, plan to go much further.

By 2030, the consulting firm AlixPartners expects hybrid and battery powered electric vehicles will represent more than 65% of all new vehicles sold. As plug-in hybrid electric vehicles and EVs gain traction, Nick Parker, director at AlixPartners, argues that OEMs will need to evolve traditional powertrain supply chains and procurement methodologies to account for associated engineering requirements, materials and technology for batteries, e-motors and transmissions. Moreover, while he expects logistics and supply chain systems will resemble those typically witnessed in the ‘traditional’ automotive sector, he points out that costs and complexity relating to specific requirements for EV batteries are likely to be driven by several key factors.

In particular, he points out that EV battery packs are typically at least double the weight of a 150-200kg traditional combustion engine and transmission. He further highlights the fact that the lithium-ion chemistry of cells means EV batteries are currently categorised as ‘Class 9’ dangerous goods or hazardous materials for logistics purposes, meaning that they require temperature-controlled handling and storage and must meet stringent customs requirements. Parker also singles out evolving OEM and supplier manufacturing footprints, particularly in relation to cell production and pack assembly, as key considerations.

“With over 80% of lithium-ion battery capacity expected to be in China and the US by 2020, supply chain and logistics requirements for European OEMs and suppliers have the potential to differ significantly where there is insufficient localised supply of battery cells,” he says.

In this light, Parker argues that decisions relating to the localisation of battery cell production, and particularly pack assembly, will be critical in optimising supply chain costs and requirements, especially given the complex requirements for transporting EV batteries long distances.

“AlixPartners expects that electrification, including localised battery pack assembly, has the potential to drive an additional 18,000 jobs in Europe by 2030. Strategic partnerships are likely to play a key role going forward in supporting EV battery supply chains as OEMs and tier ones look to replace the intellectual capital built up over decades of internal combustion engine component development. Out of a total 57 automotive partnerships in the electrification space from 2016, seven include collaboration around batteries,” he says.

Radical changeFlorian Klug, professor of logistics management at Munich University of Applied Sciences, predicts that the growth of EV production will radically change existing supply chains and supplier structures – and argues that the combustion engine-focused car industry could lose a major part of its value creation capabilities to electric drive suppliers.

“Batteries are not only valuable EV modules but also, in view of their weight and volume, the most relevant from a material flow perspective. Car manufacturers will have to rethink existing inbound, in-house and outbound operations – and completely new car modules like batteries, electric motors and transmissions will prompt the evolution of new supply chain networks,” he says.

In Klug’s view, as well as value creation potential for the supply industry, these changes will also lead to a rise in inbound transport volume, increasing the future importance of effective transport management and freight cost control.

Due to the high cost and fragility of EV batteries, producers are understandably demanding in their shipping requirements

Due to the high cost and fragility of EV batteries, producers are understandably demanding in their shipping requirements“Future make-or-buy decisions for batteries are going to influence future supply chain structures. Traditional in-house modules like engines and transmissions could be outsourced in the future, which will fundamentally transform the value chain in car manufacturing,” he says.

However, while more outsourcing could lead to more significant logistics services, the overall structure of an EV is likely to decrease overall volume and variation in the supply chain, according to Sven Dharmani, principal for performance improvement and global supply chain leader for the automotive sector at EY. He points out that EV powertrains consist of “a fraction of the number of parts compared to ICE powertrains”, suggesting that the number of suppliers, as well as the related logistics routes and necessary transport, will be significantly streamlined.

“However, this won’t occur until full EV adoption for each OEM. In the interim, the transition will make logistics more complex and challenging,” he says.

Dharmani also predicts EV battery production will be much more localised compared to current powertrain supply chains, where companies like Ford, BMW, Mercedes-Benz and Volkswagen Group centralise engine production and export volume to overseas plants. “The transportation of batteries over the water is more challenging, so we expect more in-region production and consumption. Europe, Asia and North America are seeing large investments in production capacity for lithium batteries, so I believe there will be local demand driving consumptions from the battery mega-factories,” he adds.

Charging the wavesOne ‘over the water’ company with direct experience of the potential differences between traditional component supply chains and EV battery logistics systems is ro-ro shipping and logistics provider WWL, which recently took on a ro-ro transport contract for a Japanese battery manufacturer supplying an electric vehicle plant in California (neither of which the company will name). As well as shipping finished vehicles for carmakers, Kibo Bodøgaard, head of breakbulk for WWL, says it also handles a large amount of “more delicate” high-tech cargo in the machinery and machine tool space.

“These producers are very demanding customers in terms of handling and quality procedures, and have zero tolerance for damages,” he says. “They also demand a stable frequency and velocity.”

According to Alex Conjour, head of port and cargo operations at WWL, participants in the electric vehicle supply chain are currently investing in new facility capabilities, such as charging stations, and enhancing both their technical competence and their procedures to ensure a seamless flow through their networks.

(Click to enlarge)

(Click to enlarge)“Supply chain participants are increasingly engaged in the transport of computers on wheels, whose technology is evolving at a rapid pace. Suppliers and finished vehicle manufacturers must synchronise the frequency of their collaboration and information sharing within this space to avoid the wrong kind of ‘disruption’,” he says.

Electrifying Europe and ChinaCarmakers like BMW and Mercedes-Benz are also increasingly aware of the current and potential impact of EV production on supply chains. This summer, BMW announced it would offer 25 electric models by 2025, including a dozen fully electric versions. It has also announced it would build a new electric Mini model in the UK, but with the electric components built in Dingolfing, Germany, where it currently builds components for electric models also assembled in Leipzig.

Mercedes-Benz also has aggressive EV ambitions. According to a spokesperson for the company, Daimler is investing significantly in the worldwide expansion of a network of local production hubs for batteries to help it fulfil its goal of ensuring that EVs make up 15-25% of global Mercedes-Benz sales by 2025. This autumn it announced a $1 billion investment in the US mostly to build an electric SUV and a battery plant at its Alabama facility. The carmaker is already building a €500m ($588m) battery factory in Kamenz, in eastern Germany. The carmaker has also confirmed that it and its Chinese partner BAIC intend to invest a total of 5 billion yuan ($772m) in the production of battery-electric vehicles under the Mercedes-Benz brand, as well as in local battery production in Beijing.

“The Untertürkheim site is being further developed as a high-tech location for electric components. This includes, for example, a new battery production facility at the site and the assembly of electric drive modules for front and rear axles. This makes the location a centre of excellence for the integration of the entire electric powertrain into production,” the spokesperson tells Automotive Logistics.

“This global production hub strategy ensures the direct supply of our plants in the production network with lithium-ion batteries and electric components and enables a flexible network. With regard to the transport of lithium-ion batteries, we are currently focusing on overland and maritime transport,” he adds.

Based on the weight of batteries and future vehicles, the spokesperson also reveals that railway concepts are a valid alternative. In recognition of the safety regulations for transporting lithium-ion batteries, Daimler is also running training courses for all employees involved – from R&D through production to purchasing and logistics.

“We are taking care that our logistics partners and service providers in the supply chain will be trained as well with our new products,” says the spokesperson.

Unblocking bottlenecksLooking ahead, Alixpartner’s Parker argues that the key challenges facing OEMs and suppliers in optimising the end-to-end EV battery supply chain relate to access to raw materials and the complexity of investment decisions, as well as to the recycling of EV batteries and component materials. In terms of raw materials, he believes potential challenges arise in ensuring access to critical and rare materials such as lithium and cobalt, required for cathode production, where Asia, in particular China, is prominent in supply, ownership and control.

He also reveals that Japan, China and South Korea accounted for over 65% of cathode material production in 2015, with 39% coming from China alone. While South America and Africa currently dominate lithium and cobalt resources and reserves, he confirms that China has also made a number of strategic investments in mining operations and mining companies over the past two years.

“For OEMs and suppliers outside of these geographies, ensuring security over supply chains as EV volumes ramp up, through strategic partnerships or otherwise, will be key. Furthermore, establishing EV battery recycling supply chains to enable recovery of raw materials will play a key role in supporting supply of materials,” he says.

Elsewhere, professor Florian Klug predicts that logistics costs, especially for heavy and bulky batteries, will significantly influence the location and total network structure of future EV manufacturing. In particular, he believes that the tremendous growth of the Chinese automobile market, with the highest level of vehicle production and sales in the world, will privilege China as a centre of EV manufacturing.

“This will focus future supply chains on Asian markets, and in the US with Tesla. China has built a complete value chain with a high percentage of locally produced components being incorporated into foreign cars produced in China,” he says.

Daimler's €500m battery factory in Kamenz, Germany, is part of a global investment in battery plants that will include the US and China

Daimler's €500m battery factory in Kamenz, Germany, is part of a global investment in battery plants that will include the US and ChinaIn Klug’s view, a number of different scenarios are also likely to emerge in the evolution of EV supply chains. Such scenarios include the vertical integration of battery producers and carmakers into a single company and the acquisition of battery producers by car manufacturers, as well as the expansion of battery producers into car production and the cooperation of EV manufacturers with local and foreign battery suppliers.

“The transport of bulky and heavy modules like batteries with high value favours proximate supply. There are also security reasons why at least the final assembly of batteries should take place adjacent to the vehicle manufacturer,” says Klug.

In the future, EY’s Dharmani believes, the main EV supply chain bottlenecks will relate to manufacturing capability and location, as well as their impact on logistics. He also highlights the fact that battery technology is rapidly evolving, meaning that existing battery technology and manufacturing methods may be superseded by more advanced versions.

[related_topics align="right" border="yes"]“As a result, the logistics networks will be constantly evolving based on where the up-to-date technology and manufacturing capability is established,” he says. “Mining, extraction, refining and synthetic substitutes will be important in reducing these bottlenecks and Li-ion may face competition from other types of batteries and power storage.”

For Dharmani, the best way to address these changes and challenges is to develop flexible, agile and responsive logistics networks – with cross-industry network optimisation and balancing also likely to assume increased importance.

“I think the key will be to install manufacturing capability that is flexible and easier to adapt with evolving battery technology, even though the upfront cost may be higher,” he comments.

“This is different to what the industry has done and experienced in the past,” he concludes.

One company already involved in specialist electric vehicle battery logistics is Swiss outfit Kuehne + Nagel (KN), which boasts a growing list of clients in the segment, including Asian battery cell manufacturers and European carmakers. For one customer, the company handles physical material flows from a manufacturing plant in South Korea to a battery assembly station in Austria. For another, it receives batteries destined for EVs in a battery logistics warehouse in Germany for sequencing operations for a nearby car assembly line.

One company already involved in specialist electric vehicle battery logistics is Swiss outfit Kuehne + Nagel (KN), which boasts a growing list of clients in the segment, including Asian battery cell manufacturers and European carmakers. For one customer, the company handles physical material flows from a manufacturing plant in South Korea to a battery assembly station in Austria. For another, it receives batteries destined for EVs in a battery logistics warehouse in Germany for sequencing operations for a nearby car assembly line.

In total, the company currently dedicates around 3,000 sq.m of space to testing, charging and reverse logistics activities, with sizeable growth in the pipeline. According to Achim Glass (pictured), senior vice-president and head of the company’s global automotive vertical, the rapid increase in the uptake of lithium-ion-powered vehicles opens up opportunities for logistics companies.

“With falling battery costs and drive range increases, the car showroom prices of EVs will continue to fall. Government regulations to meet CO2 emissions are [also] forcing all OEMs to change drivetrain technology,” he says.

About a year ago, KN set up a project group to identify detailed customer requirements and the expected implications for their supply chains. The goal was to work on a product to tackle the supply chain challenges, which KN launched in September.

Generally speaking, KN has observed several differences between the storage and transport types and logistics systems used for EV components compared to ‘standard’ vehicle parts. The first is based on the fact that EVs tend to have a larger proportion of expensive or valuable components, including electronics that often have shorter lifecycles. This difference results in much less stock for aftermarket repairs, says Glass, largely because products kept in the warehouse for too long quickly become outdated. He also points out that EV and battery materials must be shipped and stored with more care because of their sensitivity to variables like temperature, as well as the risk of electric shock.

“The biggest difference, however, is the lithium battery replacing the traditional combustion engine. Lithium cells and batteries are hazardous materials, which can put life at risk when not packed, shipped and stored according to international dangerous goods regulations. If a lithium battery is on fire, it cannot be extinguished” he says.“From deploying the correct packaging and correct labelling to avoiding shock and meeting temperature requirements during transport and observing very special storage regulations, the list of special requirements for a lithium-battery supply chain is long.”

On a related point, Glass believes that the hazardous nature of EV batteries represents the single largest bottleneck for EV-related logistics systems, particularly the requirement to adhere to dangerous goods regulations at all times. Such responsibility represents a significant challenge, he says, since regulations vary not only between transport modes but also between countries. Moreover, he points out that quantity or weight restrictions often apply to the transport of relatively heavy goods like batteries. For example, a single piece of air freight cargo generally must not exceed 30kg, meaning it is impossible to transport a vehicle battery by air freight.

“The bottleneck can be overcome by having the entire supply chain fully certified so that all involved stakeholders – for example the ground cargo handling agent at [the point of] origin, as well as the airline and the trucking company at the destination – are all compliant with the respective dangerous goods regulations. This is obviously very challenging, but it can be done,” he says.

Evolution not revolutionAlthough the initial focus of most logistics providers has been on transporting vast quantities of lithium-ion cells from manufacturers to carmaker battery assembly lines, Glass predicts that in just a few years from now, the logistics market will be confronted with huge numbers of batteries coming back from the aftermarket. While recognising that lithium cells and batteries are already dangerous to store and transport, Glass also stresses that the nature of a used lithium battery is even more dangerous. As a result, he argues, the entire logistics aftermarket must be revisited to meet this specific requirement – in particular, how best to organise the logistics process for replacing a used battery with a new battery at a dealership. Ultimately though, Glass believes the boom in EVs is likely to prompt evolution rather than revolution in automotive logistics systems.

“While today only a few companies are tackling the associated logistics challenges, in future more players will jump on that running train in order not to lose out on this market potential,” he adds.